- United States

- /

- Metals and Mining

- /

- NYSE:FCX

Freeport-McMoRan (FCX) Reports Q2 Sales Surge To US$7,582 Million

Reviewed by Simply Wall St

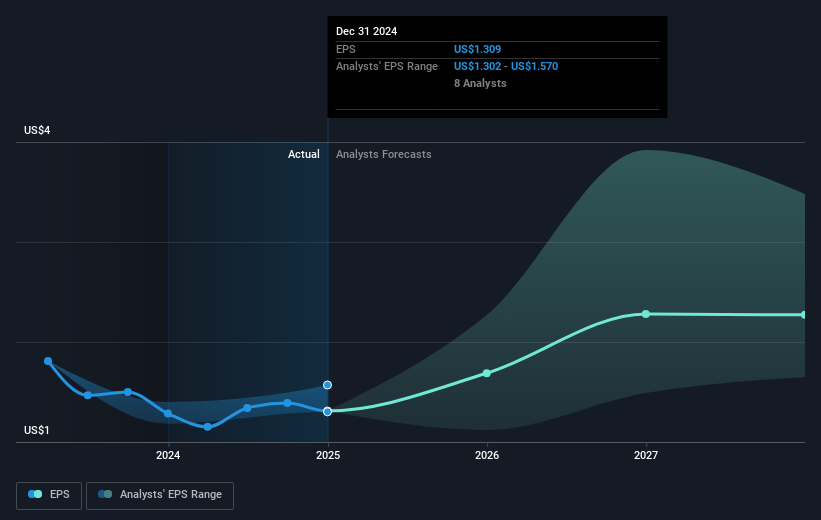

Freeport-McMoRan (FCX) recently reported a substantial increase in its second-quarter sales to USD 7,582 million and net income growing to USD 772 million, fueling positive investor sentiment. This was further supported by the company's strategic buyback initiative, repurchasing 1.5 million shares during the quarter, indicating confidence in its valuation. Despite a broader market trend, characterized by modest gains led by strong tech earnings, Freeport-McMoRan's price move of 7.5% stands out, reflecting a meaningful response to robust earnings growth and proactive shareholder returns, aligning with the current optimistic market conditions.

We've identified 1 possible red flag for Freeport-McMoRan that you should be aware of.

Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

The recent boost in Freeport-McMoRan's sales and net income aligns closely with the company's proactive measures, such as its share buyback initiative, and signals positive momentum. Over a five-year span, the company's total return, including dividends, was 198.28%, suggesting robust long-term performance amid fluctuating markets. However, in the past year, Freeport-McMoRan's share performance lagged behind both the US Metals and Mining industry and the broader US market, which is important contextual information for current investors.

The introduction of the Indonesian smelter and U.S. initiatives could potentially bolster integration, reduce costs, and increase margins, directly impacting revenue and earnings positively. With these developments, analysts forecast Freeport-McMoRan's revenue to grow at 6.5% annually over the next three years, increasing future earnings substantially. The recent price move to US$39.14 offers a discount relative to the consensus price target of US$50.90, suggesting potential room for share price growth if the company's strategy unfolds as planned. Nonetheless, the performance relative to this target will heavily depend on the stability of market conditions and the execution of ongoing expansion projects.

Jump into the full analysis health report here for a deeper understanding of Freeport-McMoRan.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FCX

Freeport-McMoRan

Engages in the mining of mineral properties in North America, South America, and Indonesia.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion