- United States

- /

- Insurance

- /

- NYSE:WRB

W. R. Berkley (WRB): Valuation Check After New Regular and Special Cash Dividends

Reviewed by Simply Wall St

W. R. Berkley (WRB) just paired its regular quarterly payout with a meaningful special dividend, sending a clear signal about balance sheet strength and management confidence in cash generation for long term shareholders.

See our latest analysis for W. R. Berkley.

Those regular and special dividends land against a backdrop where the latest share price of $69.1 sits below recent highs. Yet W. R. Berkley still posts a solid year to date share price return and an impressive multi year total shareholder return that suggests momentum in the longer term story is intact.

If this kind of shareholder friendly capital return has caught your eye, it could be worth exploring other insurance and financial names with aligned incentives using fast growing stocks with high insider ownership.

With WRB trading below recent highs but still boasting robust multi year returns and a large intrinsic value gap, investors face a key question: is the stock quietly undervalued, or are markets already pricing in its future growth?

Most Popular Narrative: 6.9% Undervalued

With W. R. Berkley’s fair value estimate sitting modestly above the recent $69.10 close, the dominant narrative frames today's price as leaving some upside on the table.

Prudent capital management, shown by a growing investment portfolio benefitting from higher new money yields and conservative reserving, is increasing investment income and book value per share, laying a foundation for higher long-term earnings and the potential for resumed share buybacks.

Curious how modest top line expectations, rising margins and a richer future earnings multiple can still point to upside from here? The full narrative reveals the specific earnings path, profitability shift and valuation reset that underpin this fair value call, and how sensitive it is to even small changes in those assumptions.

Result: Fair Value of $74.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could be challenged if softening property and casualty pricing or rising loss trends erode underwriting margins more quickly than expected.

Find out about the key risks to this W. R. Berkley narrative.

Another Angle on Valuation

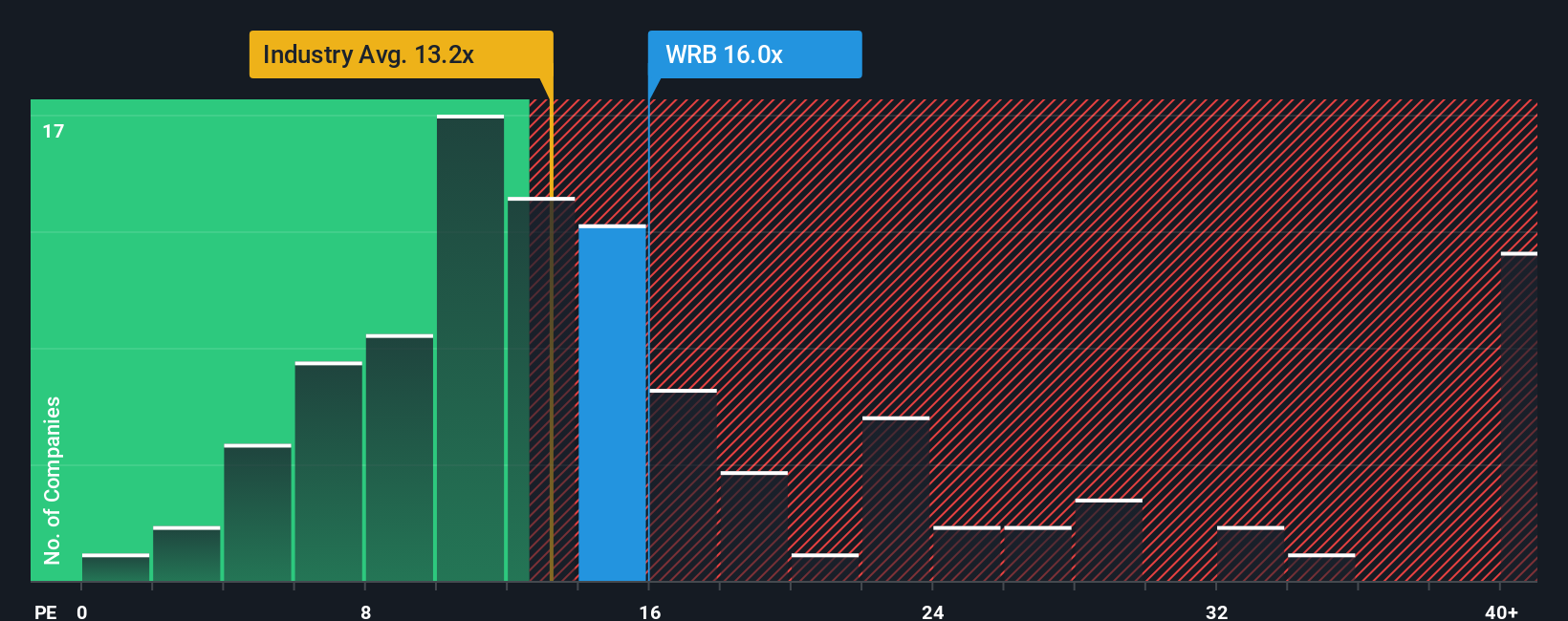

On earnings based measures, W. R. Berkley looks less cheap than the narrative suggests. Its 13.8x price to earnings ratio sits above the US insurance industry at 13.6x, the peer average at 13.3x, and even our 12.8x fair ratio. This points to some valuation risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own W. R. Berkley Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just minutes: Do it your way.

A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for your next smart opportunity?

Do not stop with one insurance leader; use the Simply Wall Street Screener to uncover more targeted ideas that match your strategy before the market moves.

- Capitalize on mispriced potential by targeting companies that look cheap on cash flow fundamentals through these 908 undervalued stocks based on cash flows.

- Ride structural growth in machine learning and automation by zeroing in on innovators shaping the future with these 26 AI penny stocks.

- Lock in reliable income streams by focusing on businesses offering consistent payouts via these 13 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if W. R. Berkley might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WRB

W. R. Berkley

An insurance holding company, operates as a commercial line writer worldwide.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)