- United States

- /

- Insurance

- /

- NYSE:HIG

Hartford Insurance Group (NYSE:HIG) Announces Dividend Payouts for Common and Preferred Stocks

Reviewed by Simply Wall St

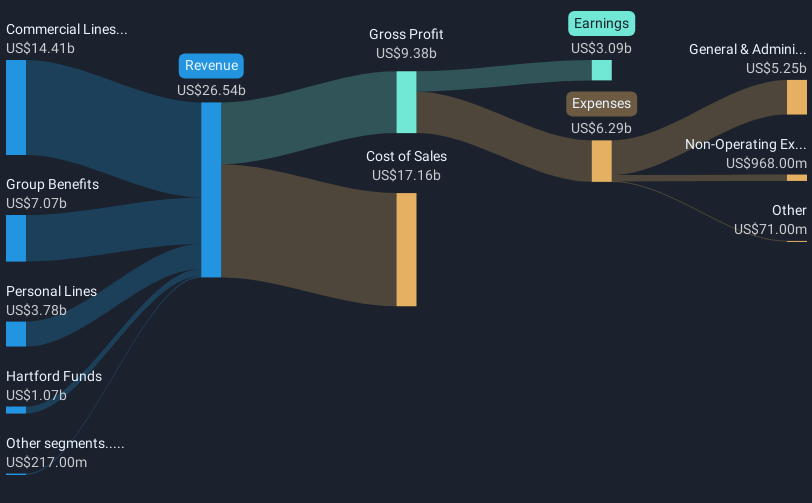

Hartford Insurance Group (NYSE:HIG) announced dividends across common and preferred shares, highlighting its commitment to shareholder value. This, combined with a share price increase of 15% last quarter, shows strong shareholder response. Despite reporting a decline in Q1 net income, Hartford's robust dividend affirmations and significant share buybacks bear weight. On the broader market front, where stocks rose slightly outpacing recent slumps, Hartford's moves countered the general dip. While market rebounds influenced indices, the Hartford’s events underscored its strategic shifts amid Executive and Organizational changes, enhancing its market positioning within a partially tumultuous period.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

The recent dividend announcements and share buybacks from Hartford Insurance Group could bolster shareholder confidence, reinforcing the company's narrative of enhancing technological efficiencies and disciplined underwriting. This aligns with Hartford's broader strategy of adopting AI and cloud technologies to improve operational efficiencies and customer experiences. Such moves might have a positive influence on revenue and earnings forecasts, as the company targets growth in the Excess and Surplus markets while refining its combined ratios.

Hartford Insurance Group's shares have seen a compelling long-term appreciation, with a total return of 270.11% over the past five years. This impressive growth underscores the company's successful adaptations and investment in technology. In the last year, Hartford outpaced the US Insurance industry, which returned 17.1%, reflecting its advantageous market positioning and operational strategies.

Despite short-term share price movements and a slight discount to the analyst consensus price target of US$134.72, the company's current price of US$126.58 suggests that it is relatively in line with market valuations. The price target implies a modest upside, and it will be crucial to monitor how Hartford's revenue and earnings materialize in light of its digital investments and expansion efforts. These factors could very well determine if the market reassesses its perceived fair value, considering anticipated revenue growth and potential macroeconomic challenges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Hartford Insurance Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hartford Insurance Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HIG

Hartford Insurance Group

Provides insurance and financial services to individual and business customers in the United States, the United Kingdom, and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives