Advertisement

- United States

- /

- Insurance

- /

- NasdaqGS:ROOT

Root, Inc. (NASDAQ:ROOT) Reported Earnings Last Week And Analysts Are Already Upgrading Their Estimates

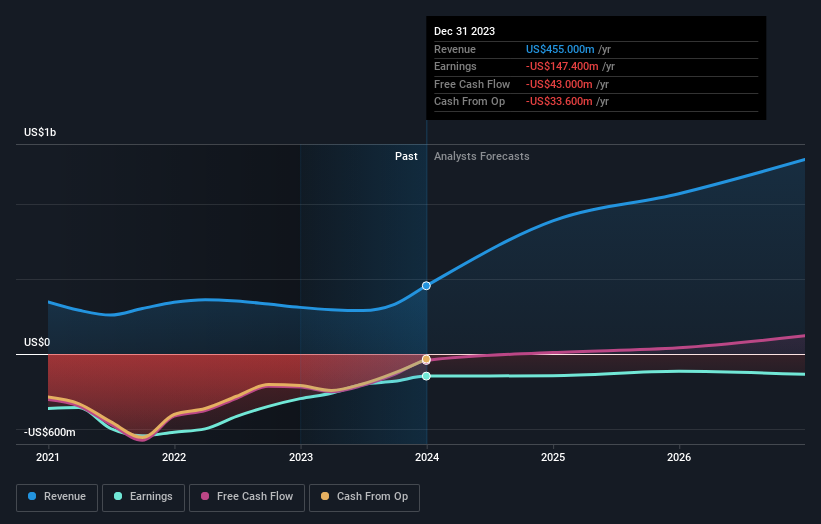

Root, Inc. (NASDAQ:ROOT) just released its full-year report and things are looking bullish. Revenues were better than expected, with US$455m in revenue some 20% ahead of forecasts. The company still lost US$10.24 per share, although the losses were marginally smaller than the analysts expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Root

Taking into account the latest results, the current consensus from Root's eight analysts is for revenues of US$887.8m in 2024. This would reflect a major 95% increase on its revenue over the past 12 months. The loss per share is expected to ameliorate slightly, reducing to US$9.64. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$622.0m and losses of US$10.48 per share in 2024. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

It will come as no surprise to learn thatthe analysts have increased their price target for Root 6.9% to US$11.63on the back of these upgrades. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Root at US$15.00 per share, while the most bearish prices it at US$10.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting Root's growth to accelerate, with the forecast 95% annualised growth to the end of 2024 ranking favourably alongside historical growth of 7.5% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 5.8% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Root to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on Root. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Root analysts - going out to 2026, and you can see them free on our platform here.

It is also worth noting that we have found 4 warning signs for Root (1 is a bit unpleasant!) that you need to take into consideration.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ROOT

Root

Provides insurance products and services in the United States.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

134 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on AbbVie ·

AbbVie Inc. (ABBV): The Post-Humira "Ascent" Phase and the Immunology Juggernaut

Fair Value:US$253.2313.2% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Duolingo ·

Duolingo Inc. (DUOL): The "User-First" Reset and the 100 Million DAU Blueprint

Fair Value:US$295.666.7% undervalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Hansol Chemical ·

Hansol Chemical (014680): The HBM Materials Surge and the Silicon Anode Pivot

Fair Value:₩373.93k26.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1308 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0