There’s a lot going on right now. As yet another war spreads across the Middle East, AI (itself a potential bubble) is upending the software industry. At times like this, it’s a good idea to take a step back to gain some perspective.

We are also at Year 1 of the next 25 years into the century. So, what better time to take a super long view, and think about what the next 25 years could mean for investors.

What Happened In Markets This Week

Here’s a quick summary of what’s been going on:

🏦 Oil Shock Complicates Rate-Cut Plans for Central Banks ( Morningstar / Dow Jones )

- What happened : Rising oil prices linked to the Iran conflict have renewed inflation concerns across Asia, complicating central banks’ plans to support slowing growth with rate cuts. Economists expect governments to rely on fiscal measures like fuel subsidies and tax adjustments while currencies across several Asian economies weaken.

- European government bonds suffered their worst week in a year as rising energy prices and geopolitical tensions erased expectations for rate cuts. A week ago lower rates were taken as a given, but yields now point to a possible hike from the ECB this year.

- How it impacts investors: A renewed inflation shock could delay interest rate cuts globally, reinforcing a “higher for longer” environment for borrowing costs. This may pressure growth-sensitive assets while supporting commodities and inflation hedges.

- Next steps: Check to see if your portfolio is exposed to companies impacted by higher interest rates.

🤖 AI Revenue Race Tightens as OpenAI and Anthropic Scale Enterprise Adoption ( Techloy )

- What happened: OpenAI reached $25 billion in annualized revenue by the end of February 2026, up from $21.4 billion at the end of 2025. Anthropic’s annualized revenue surged from $9 billion at the end of 2025 to over $19 billion, with enterprise clients contributing about 80% of its revenue and Claude Code alone generating roughly $2.5 billion.

- How it impacts investors: Rapid revenue growth across leading AI firms signals accelerating enterprise adoption and a deepening competition for AI infrastructure. This spending race continues to benefit cloud providers and chipmakers that supply the compute powering AI systems.

- Next steps: Explore companies benefiting from the AI infrastructure boom with the U.S. Data Center (AI Picks and Shovels) Stocks screener.

🚗 BYD’s Rapid European Expansion Puts Pressure on EV Rivals ( Electric Vehicles )

- What happened: BYD’s vehicle registrations in Germany rose from 185 to 3,053 year-over-year, surpassing Tesla’s 2,276 units in the market. The company also reported 2,154 UK registrations in February and became Spain’s top-selling new energy vehicle brand with 3,003 units and a 15.4% market share, while starting trial production at its Hungary factory.

- How it impacts investors: BYD’s accelerating expansion in Europe highlights growing competition for established EV makers, particularly as lower-priced models and hybrids pressure pricing across the sector. Investors may see increasing margin and market share pressure on European automakers and other EV players if BYD’s growth continues.

- Next steps: Have a look at BYD's company report to explore its fundamentals, valuation, and growth outlook.

🏦 Poland Considers Selling Gold Reserves to Finance Defense Spending ( Bloomberg )

- What happened: Poland’s central bank governor proposed selling part of the country’s roughly 550-ton gold reserve to help finance a $13 billion defense spending plan. The proposal would involve selling gold and later repurchasing it, though legal constraints may limit the central bank’s ability to directly fund government spending.

- How it impacts investors: If central banks begin monetizing gold reserves to fund fiscal spending, it could introduce new dynamics into gold supply and demand expectations. This may increase volatility in the precious metals market.

- Next steps: If you believe the long-term outlook for precious metals is bright, volatility could create opportunities. The Global Precious Metals screener includes all of the producers.

🔧 Broadcom Signals $100B AI Chip Opportunity as Custom Silicon Gains Momentum ( Yahoo Finance )

- What happened: Broadcom said it expects the market for its AI chips to exceed $100 billion next year, driven by strong demand from major clients including Meta Platforms and Anthropic. The company’s shares rose more than 5% after the forecast, with CEO Hock Tan saying Broadcom is well positioned despite memory shortages and limited capacity at TSMC.

- How it impacts investors: Rising demand for custom AI processors suggests hyperscalers are diversifying their chip supply beyond Nvidia’s GPUs. This shift could intensify competition in the data-center chip market and reshape long-term market share across AI semiconductor companies.

- Next steps: Explore Broadcom’s growth outlook and valuation .

🔮 What will shape the next 25 years for markets and investors?

The first 25 years of this century were shaped by a few notable themes:

- 🇨🇳 China’s economy grew fifteenfold ! This resulted in soaring demand for commodities, particularly during the early part of the century. It also kept a lid on global inflation as the world was flooded with cheap go o ds.

- 📱 Tech companies grew to dominate the market , as ecommerce, smart phones and cloud computing emerged.

- 💰 Soaring debt and near zero interest rates. First it was households that embraced debt (until the GFC) and then as central banks embraced quantitative easing, governments piled on the debt. Super low rates fueled an avalanche of investment in emerging technologies.

During this period, the S&P 500’s average return was 7.6%, which was notably lower than the 16.9% average return from 1975 to 1999. But that doesn’t tell the full story. The last 25 years included a “lost decade,” followed by above average returns from 2010 to 2025.

Looking toward 2050, there are a few prominent secular trends that are likely to shape economies and markets.

We are going to highlight five of them, four of which can be classified as transitions, and one that is more of a headwind than anything else.

🤖 Transition 1: AI to Automation

Recently released models and tools from OpenAI, Anthropic and Google have shown AI models are still improving at a rapid pace. And OpenClaw became perhaps the first viral agentic app built on top of the AI infrastructure layer. While models and apps are improving, inference costs are falling rapidly .

LLMs are still far from perfect, but they are a lot more reliable than they were a year ago. The automation and/or augmentation of a big chunk of knowledge work now seems inevitable.

Automation in the form of robotaxis, humanoid robots and autonomous delivery drones will take longer to scale, and require considerable capital. Automation in factories isn’t new, but there’s a lot more that can be automated.

💡 Check the Robotics and Automation Stocks screener for ideas in this space.

Productivity gains need to be offset against the impact of job losses, which makes forecasting just about impossible. For what it’s worth, here are a few estimates:

- PWC’s base case projects AI adding 7.7% to global GDP by 2035 . However, their projections range from 0.8% to 14.7%.

- Penn Wharton's Budget Model projects generative AI will raise US GDP and productivity by 1.5% by 2035, nearly 3% by 2055, and 3.7% by 2075 . They believe the biggest productivity gain will occur around 2032.

The hyperscalers (a.k.a. big tech) are making massive investments now, in the belief that revenue and profits will come later. Whether the returns come soon enough to justify the investments remains to be seen. BlackRock, for one, is somewhat skeptical .

💡 Regardless of the eventual impact on GDP, and the returns generated by the hyperscalers, there are certain to be some big winners:

- The infrastructure is being built, which is good for the companies doing the building, and the companies supplying the hardware.

- That infrastructure will allow a new generation of companies to build apps, devices, robots and drones.

⚡ Transition 2: Electrifying the Global Economy

In June last year we wrote about the ‘Turbulent Transition To Greener Energy’ , The TL;DR was that the odds of reaching net zero by 2050 weren't looking good.

The main problem is that it will cost as much as $5 trillion per year to do so.

Net zero by 2050 might be wishful thinking, but simple economics could still get the world quite a long way down the path:

- The cost and efficiency of battery storage is improving. The cost of solar panels has already plummeted.

- Massive investments are being made to try to get fusion reactors and SMRs (small modular reactors) to a viable stage.

- Fossil fuel reserves are finite, and the cost of extracting them increases as the remaining reserves become harder to reach. Peak oil demand is a concept that keeps being pushed further into the future ( currently estimated around 2035 ). At some point, the potential returns on new investments won’t look very attractive, leading to lower production and higher prices. When that happens, the alternatives become more attractive based on price alone.

An autonomous future powered by AI can’t occur without a lot of electricity. Regardless of whether it comes from renewables, fossil fuel or nuclear power, power grids across the globe need to be scaled up.

We can’t be certain of the world’s energy mix 15 to 25 years from now. But there are a few companies that supply equipment that’s essential whatever the mix looks like.

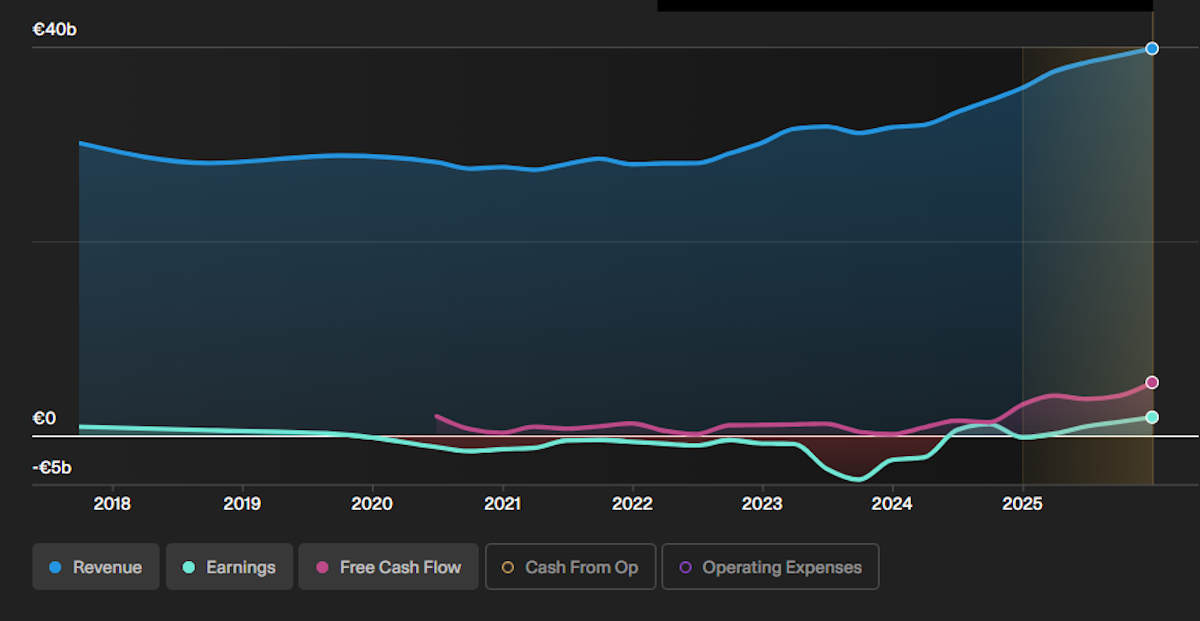

These are the companies that supply and build the technologies and infrastructure required to deliver high-density power at scale. Siemens Energy ( XTRA:ENR ) below is one example, and you’ll find others in the Power Grid Technology Stocks screener.

👴 Transition 3: The Two Sides of Demographics

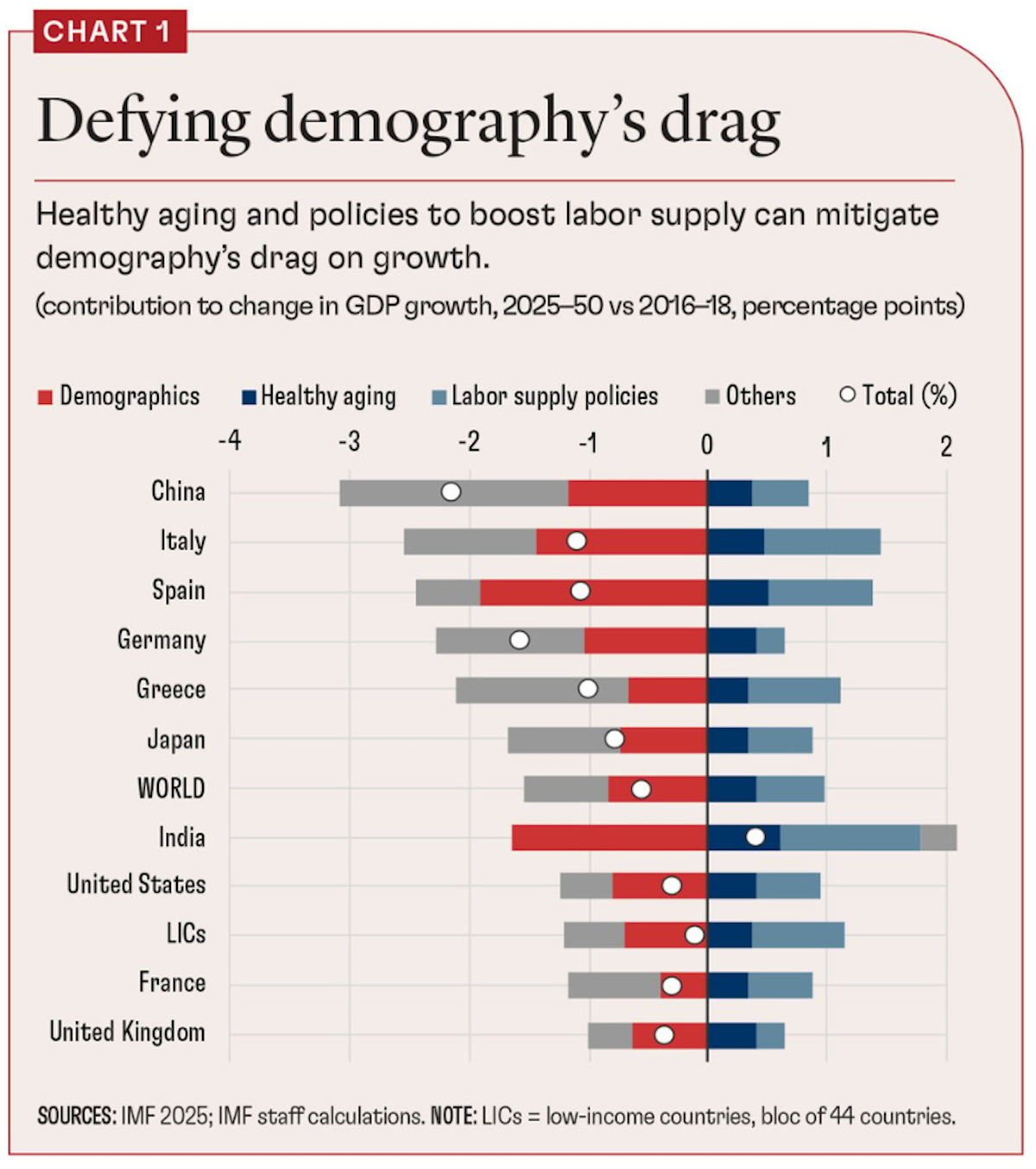

Evolving demographics could be viewed as a headwind, but there are really two sides to this story. The West, Japan, and China are already dealing with aging populations. On the other hand, several countries in Asia (notably India) and Africa have young and growing populations.

Fertility rates in South Korea (0.7), China (0.99), and the US (1.6) are well below the replacement rate of 2.1. This leads to a shrinking labor force and rising dependency ratios, placing immense pressure on social safety nets. China, in particular, faces a projected 2.7 percentage point growth slowdown due to its rapidly aging population.

Aging populations are a potential tailwind for automation and for healthcare. The IMF has identified ‘healthy aging’ as one way to offset the impact of aging populations.

💡 We previously covered how longer lifespans can reshape markets.

On the other side is the Demographic Dividend. By 2050, one in four people on Earth will be African . India and Southeast Asia are entering a "peak working-age window," creating a self-reinforcing cycle of consumer demand.

Goldman Sachs estimates India’s average annual earnings growth at 12.6% over the next decade , nearly double the forecast for the S&P 500. The global middle class will continue to rise, but its center of gravity is shifting toward the "E7" economies.

🌐 Transition 4: Deglobalization

Globalization has been a secular trend for most of the last 50 years, but the tide has turned. Analysts at RBC expect the shift from a US-led, rules-based global order to a power-based, multipolar order t o be one of the defining themes of the next 25 years .

Some are using the term "reglobalization" to describe the rewiring of trade routes and supply chains based on security and resilience rather than just-in-time cost efficiency.

China’s manufacturing sector has acted as a disinflationary tailwind for the last 25 years. Unwinding that paradigm is therefore likely to be inflationary.

These new alliances, and the demographic shifts mentioned above are also important for investors, as economists expect the world’s largest economies in 2050 to include China, India, Indonesia and Brazil .

One of the positive consequences of deglobalization is that leaders are being forced to make more domestic investments. These are needed to ensure energy and food security, and self-sufficiency.

This is yet another reason that infrastructure investment is seen as an imperative for every country. With all the focus on technology, listed infrastructure has become attractive on a ‘relative valuation’ basis.

📊 The Headwind: Reckoning with Debt

The final, sobering force is the return of fiscal dominance . Global debt, including government, private sector, and consumer borrowing, reached a staggering $348 trillion in 2025 . In the US, public debt is on track to surpass 120% of GDP by 2036.

For the first time in decades, government interest payments in many OECD nations now exceed defense spending. This "fiscal bind" means the era of near-zero interest rates is probably over.

As long as this headwind remains, bonds might not be the stabilizing force they have been in the past. Real assets like gold, commodities and real estate might be more viable alternatives too.

The other potential consequence is that growing industries and companies will be competing for capital, making it more expensive. Companies without a proven business model or cash flows will struggle if, or when, liquidity dries up.

💡 The Insight: Your portfolio may need to evolve too

The transitions we mentioned above could get quite messy at times. No doubt there will be winners and losers.

Economists expect returns over the next 10 years to be a lot more modest than the 15 odd percent of the last 10 years.

Goldman Sachs expects 6.5% from US large caps. JP Morgan is making similar forecasts for returns to 2035 : 7% for global equities, 6.7% for US large caps, and 6.4% for a 60/40 stock and bond portfolio.

Whether those projections turn out to be correct or not, it’s likely that the returns for individual companies will vary a lot. Some will be disrupted and some will do the disrupting.

Passive investing has worked very well over the last 15 years. The concentration of ‘Mag 7’ stocks in indexes like the S&P 500 worked in investors’ favor. As the global economy evolves, that concentration could become a drag on returns. Which is all the more reason to focus on finding individual listed companies with bright futures.

Key Events Next Week

There’s plenty of inflation data out this week, although central bankers might be watching the oil price more closely.

Tuesday

- 🇯🇵 Japan GDP YoY (2nd/Revised Estimate)

- 📈 Forecast 0.2%, Previous -2.3%

- ➡️ Why it matters: Any upward revision supports BoJ rate hike expectations.

Wednesday

-

🇩🇪 Germany CPI Final YoY

- 📉 Forecast 1.9%, Previous 2.1%

- ➡️ Why it matters: A confirmed print below the ECB's 2% target gives policymakers room to cut further, but could also be overshadowed by the spike in energy prices.

-

🇺🇸 US CPI YoY

- 📉 Forecast 2.4%, Previous 2.4%

- ➡️ Why it matters: A surprise to the upside could stall Fed rate cut expectations amid tariff fears.

Thursday

- 🇺🇸 US Trade Balance

- 📉 Forecast -$65 B, Previous -$70.3

- ➡️ Why it matters : Will provide further insight on the impact of tariffs after the recent widening of the deficit.

Friday

-

🇬🇧 UK Monthly GDP MoM

- 📈 Forecast 0.1%, Previous 0.1%

- ➡️ Why it matters: A miss would intensify calls for faster BoE rate cuts, which will need to be weighed against rising energy prices.

-

🇺🇸 US Core PCE Price Index YoY (The Fed's preferred inflation gauge )

- 📉 Forecast 3%, Previous 3%

- ➡️ Why it matters: Another key data point ahead of the Fed’s next meeting.

Most of the large caps have reported, but lots of smaller companies including retailers and software companies will be reporting over the next few weeks:

- Oracle ( ORCL)

- HP ( HP )

- HP Enterprise ( HPE )

- Adobe ( ADBE)

- Dollar General ( DG )

- Ulta Beauty ( ULTA )

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.