- United States

- /

- Household Products

- /

- NYSE:ODC

Further Upside For Oil-Dri Corporation of America (NYSE:ODC) Shares Could Introduce Price Risks After 27% Bounce

Oil-Dri Corporation of America (NYSE:ODC) shareholders have had their patience rewarded with a 27% share price jump in the last month. Looking further back, the 24% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

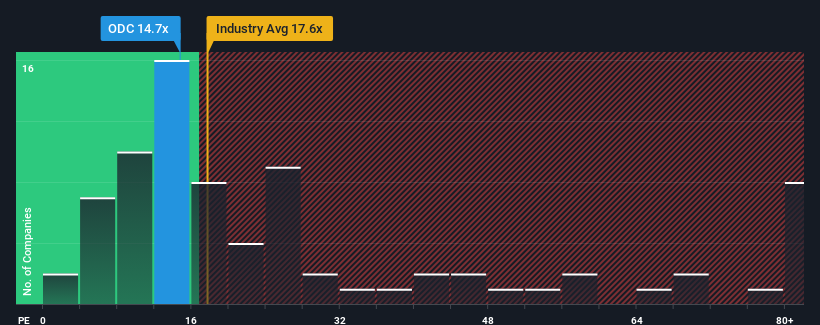

In spite of the firm bounce in price, Oil-Dri Corporation of America's price-to-earnings (or "P/E") ratio of 14.7x might still make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 20x and even P/E's above 35x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Oil-Dri Corporation of America has been doing a good job lately as it's been growing earnings at a solid pace. It might be that many expect the respectable earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Oil-Dri Corporation of America

How Is Oil-Dri Corporation of America's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as Oil-Dri Corporation of America's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 28% last year. Pleasingly, EPS has also lifted 421% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 15% shows it's noticeably more attractive on an annualised basis.

With this information, we find it odd that Oil-Dri Corporation of America is trading at a P/E lower than the market. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Bottom Line On Oil-Dri Corporation of America's P/E

Oil-Dri Corporation of America's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Oil-Dri Corporation of America revealed its three-year earnings trends aren't contributing to its P/E anywhere near as much as we would have predicted, given they look better than current market expectations. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

Having said that, be aware Oil-Dri Corporation of America is showing 1 warning sign in our investment analysis, you should know about.

You might be able to find a better investment than Oil-Dri Corporation of America. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ODC

Oil-Dri Corporation of America

Develops, manufactures, and markets sorbent products in the United States and internationally.

Outstanding track record with excellent balance sheet and pays a dividend.