Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:WMG

January 2025's US Stock Selections That May Be Priced Below Fair Value

Simply Wall St

Reviewed by Simply Wall St

As of January 2025, the U.S. stock market is experiencing volatility, with significant declines in major indices like the Nasdaq Composite and S&P 500 due to concerns over China's advancements in artificial intelligence. This environment of uncertainty presents potential opportunities for investors to identify stocks that may be priced below their fair value, suggesting a focus on fundamentals such as strong earnings potential and resilience amid technological shifts could be key factors in evaluating these opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Argan (NYSE:AGX) | $137.36 | $273.30 | 49.7% |

| First National (NasdaqCM:FXNC) | $24.77 | $48.65 | 49.1% |

| Berkshire Hills Bancorp (NYSE:BHLB) | $28.65 | $56.59 | 49.4% |

| German American Bancorp (NasdaqGS:GABC) | $39.94 | $78.06 | 48.8% |

| Heartland Financial USA (NasdaqGS:HTLF) | $66.43 | $129.40 | 48.7% |

| Western Alliance Bancorporation (NYSE:WAL) | $94.00 | $184.90 | 49.2% |

| Privia Health Group (NasdaqGS:PRVA) | $22.87 | $44.59 | 48.7% |

| Ubiquiti (NYSE:UI) | $392.09 | $770.21 | 49.1% |

| Tenable Holdings (NasdaqGS:TENB) | $44.19 | $86.65 | 49% |

| RXO (NYSE:RXO) | $26.81 | $52.21 | 48.6% |

Let's explore several standout options from the results in the screener.

Intuit (NasdaqGS:INTU)

Overview: Intuit Inc. offers financial management, compliance, and marketing products and services in the United States with a market cap of approximately $167.38 billion.

Operations: The company's revenue segments include Pro-Tax at $596 million, Consumer at $4.43 billion, Credit Karma at $1.83 billion, and Global Business Solutions at $9.73 billion.

Estimated Discount To Fair Value: 33.3%

Intuit is trading at US$606.62, significantly below its estimated fair value of US$909.29, suggesting it may be undervalued based on discounted cash flow analysis. With revenue expected to grow faster than the U.S. market and earnings projected to increase by 17.3% annually, Intuit's financial outlook appears robust. Recent strategic partnerships with Amazon and product innovations like TurboTax's fast refund offerings enhance its growth potential, reinforcing its strong cash flow position amidst evolving market dynamics.

- Our growth report here indicates Intuit may be poised for an improving outlook.

- Take a closer look at Intuit's balance sheet health here in our report.

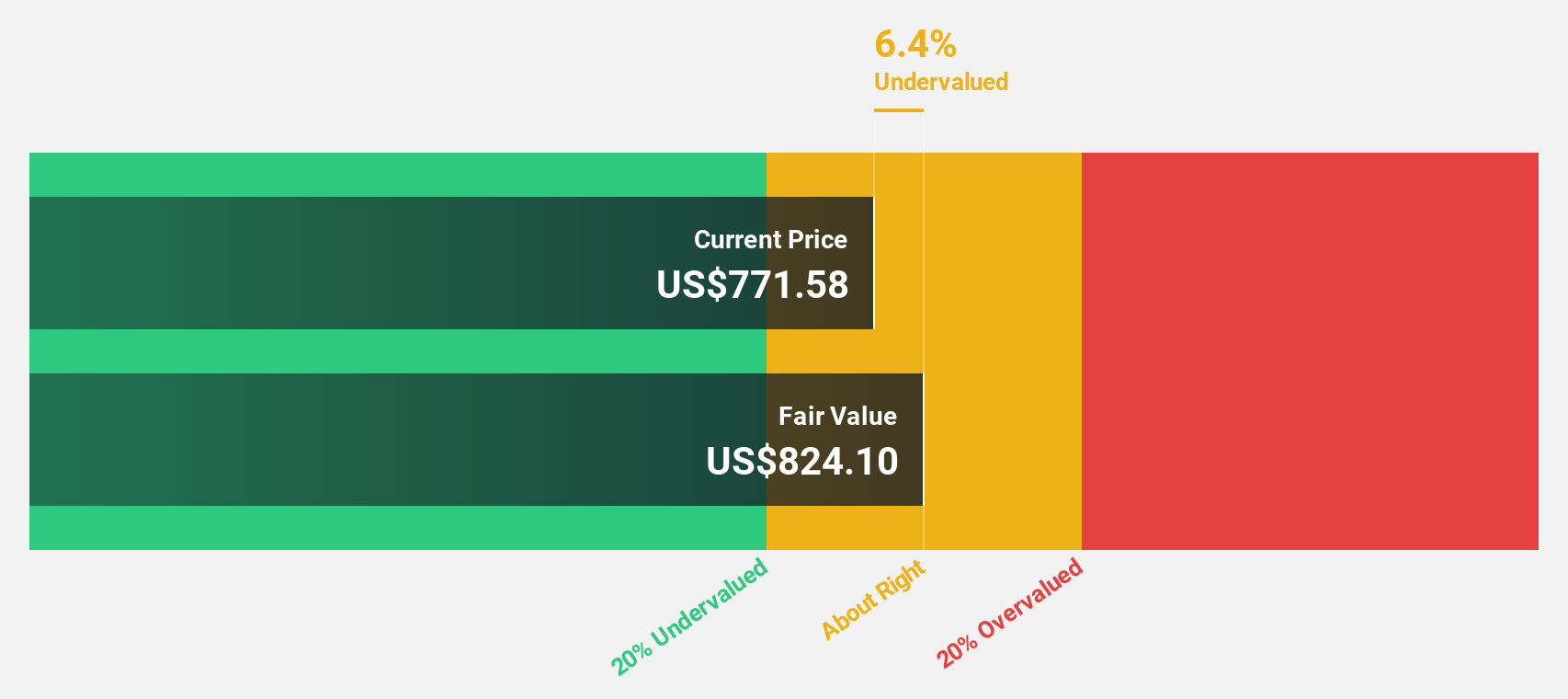

Warner Music Group (NasdaqGS:WMG)

Overview: Warner Music Group Corp. is a music entertainment company operating in the United States, the United Kingdom, Germany, and internationally with a market cap of $15.49 billion.

Operations: The company generates revenue from its Recorded Music segment, contributing $5.22 billion, and its Music Publishing segment, which adds $1.21 billion.

Estimated Discount To Fair Value: 25.6%

Warner Music Group, trading at US$31.2, is priced below its estimated fair value of US$41.94, reflecting potential undervaluation based on cash flows. Despite slower revenue growth compared to the U.S. market, earnings are forecast to rise significantly at 20.3% annually. Recent strategic moves include a $100 million share repurchase program and expansion into India’s music market through acquisitions, which could bolster its financial position despite high debt levels relative to operating cash flow.

- The growth report we've compiled suggests that Warner Music Group's future prospects could be on the up.

- Dive into the specifics of Warner Music Group here with our thorough financial health report.

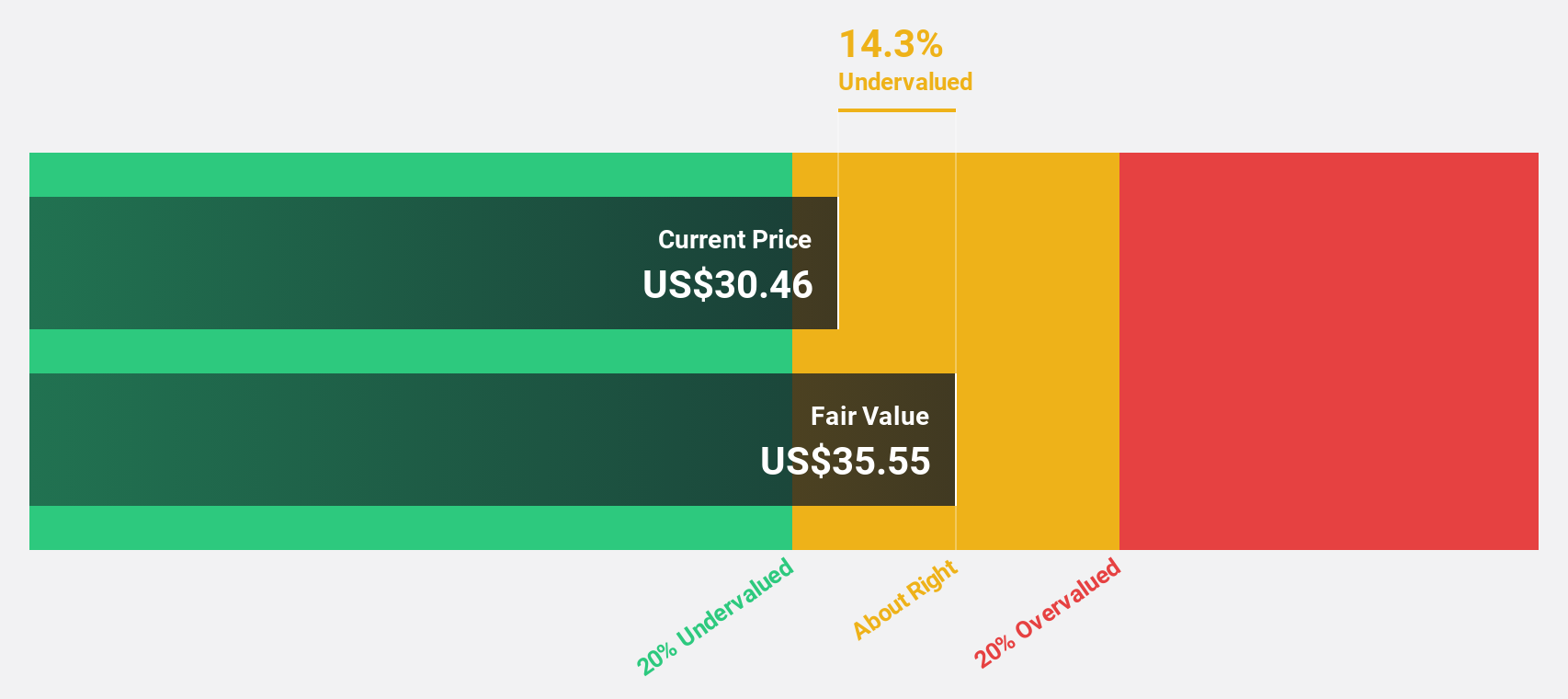

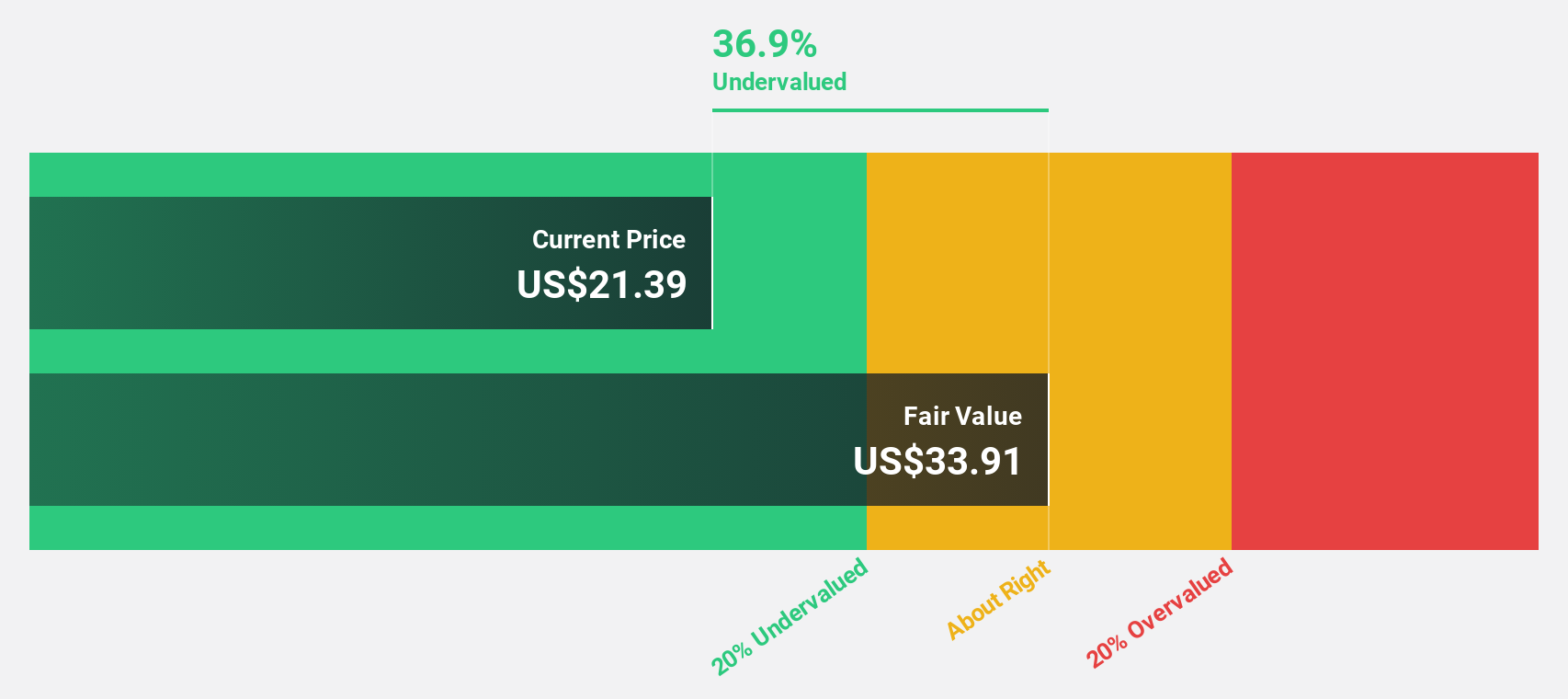

Kenvue (NYSE:KVUE)

Overview: Kenvue Inc. is a global consumer health company with a market cap of approximately $39.84 billion.

Operations: Kenvue Inc. generates revenue through its three main segments: Self Care ($6.50 billion), Essential Health ($4.73 billion), and Skin Health and Beauty ($4.23 billion).

Estimated Discount To Fair Value: 40.4%

Kenvue, trading at US$21.44, is significantly undervalued compared to its fair value estimate of US$35.98. While revenue growth lags behind the U.S. market at a forecasted 3.3% annually, earnings are expected to grow substantially by 20.6% per year, outpacing the market average. Despite high debt and declining profit margins from last year, recent dividend affirmations and strategic expansions like the Guelph facility underscore its commitment to long-term growth and financial resilience.

- In light of our recent growth report, it seems possible that Kenvue's financial performance will exceed current levels.

- Delve into the full analysis health report here for a deeper understanding of Kenvue.

Key Takeaways

- Click this link to deep-dive into the 172 companies within our Undervalued US Stocks Based On Cash Flows screener.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Warner Music Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WMG

Warner Music Group

Operates as a music entertainment company in the United States, the United Kingdom, Germany, and internationally.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor