Advertisement

- United States

- /

- Personal Products

- /

- NasdaqGM:NAII

Here's Why Natural Alternatives International (NASDAQ:NAII) Can Manage Its Debt Responsibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Natural Alternatives International, Inc. (NASDAQ:NAII) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Natural Alternatives International

What Is Natural Alternatives International's Net Debt?

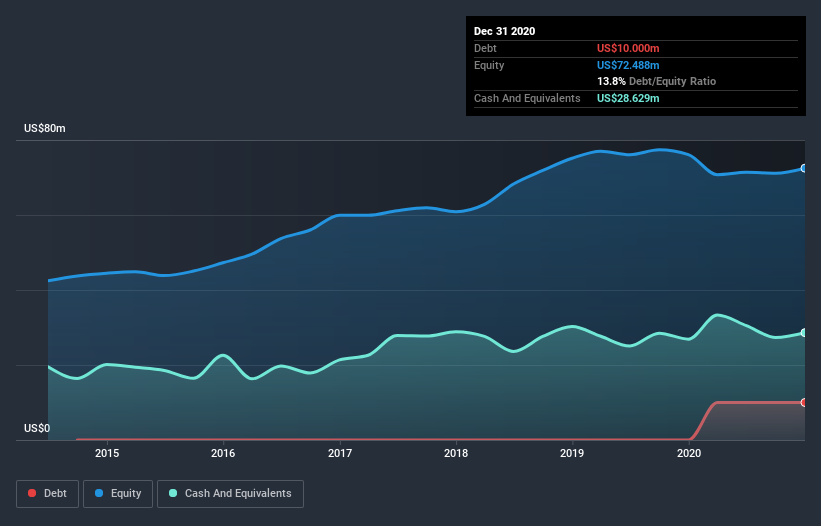

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Natural Alternatives International had US$10.0m of debt, an increase on none, over one year. However, it does have US$28.6m in cash offsetting this, leading to net cash of US$18.6m.

A Look At Natural Alternatives International's Liabilities

The latest balance sheet data shows that Natural Alternatives International had liabilities of US$32.7m due within a year, and liabilities of US$20.3m falling due after that. Offsetting these obligations, it had cash of US$28.6m as well as receivables valued at US$17.3m due within 12 months. So its liabilities total US$7.14m more than the combination of its cash and short-term receivables.

Given Natural Alternatives International has a market capitalization of US$100.2m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Natural Alternatives International also has more cash than debt, so we're pretty confident it can manage its debt safely.

Another good sign is that Natural Alternatives International has been able to increase its EBIT by 23% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Natural Alternatives International will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Natural Alternatives International has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Considering the last three years, Natural Alternatives International actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Natural Alternatives International has US$18.6m in net cash. And we liked the look of last year's 23% year-on-year EBIT growth. So we don't have any problem with Natural Alternatives International's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 4 warning signs with Natural Alternatives International (at least 1 which doesn't sit too well with us) , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Natural Alternatives International, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Natural Alternatives International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:NAII

Natural Alternatives International

Engages in formulating, manufacturing, and marketing nutritional supplements in the United States and internationally.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor