Advertisement

- United States

- /

- Beverage

- /

- NYSE:KOF

Is It Too Late to Consider Coca-Cola FEMSA After Its Strong Multi Year Share Price Run?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Coca-Cola FEMSA. de is still worth considering after its recent run up, or if the easy money has already been made, you are in the right place because we are going to dig into what the current share price really implies.

- The stock has climbed about 1.1% over the last week, 2.8% over the past month, and 14.3% year to date, building on longer term gains of 12.0% over 1 year, 45.7% over 3 years, and 135.5% over 5 years.

- Behind those moves, the market has been reacting to Coca-Cola FEMSA. de's ongoing expansion in its core Latin American markets and continued investment in digital distribution and route to market efficiency. Many investors view these as strong competitive advantages. At the same time, macro uncertainty and shifting consumer trends in beverages are keeping a close spotlight on what constitutes a fair price for that growth.

- On our numbers, Coca-Cola FEMSA. de scores a solid 5 out of 6 on our valuation checks, suggesting it screens as undervalued on most of them. Next we will walk through those different valuation approaches before finishing with a more holistic way to think about what the stock might be worth.

Approach 1: Coca-Cola FEMSA. de Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today.

For Coca-Cola FEMSA. de, the latest twelve month free cash flow stands at about MX$7.5 billion. Analysts provide detailed forecasts for the next few years, which are then extended by Simply Wall St to build a longer term view. Under this 2 Stage Free Cash Flow to Equity model, free cash flow is projected to rise to roughly MX$49.8 billion by 2035 as the business scales and margins improve.

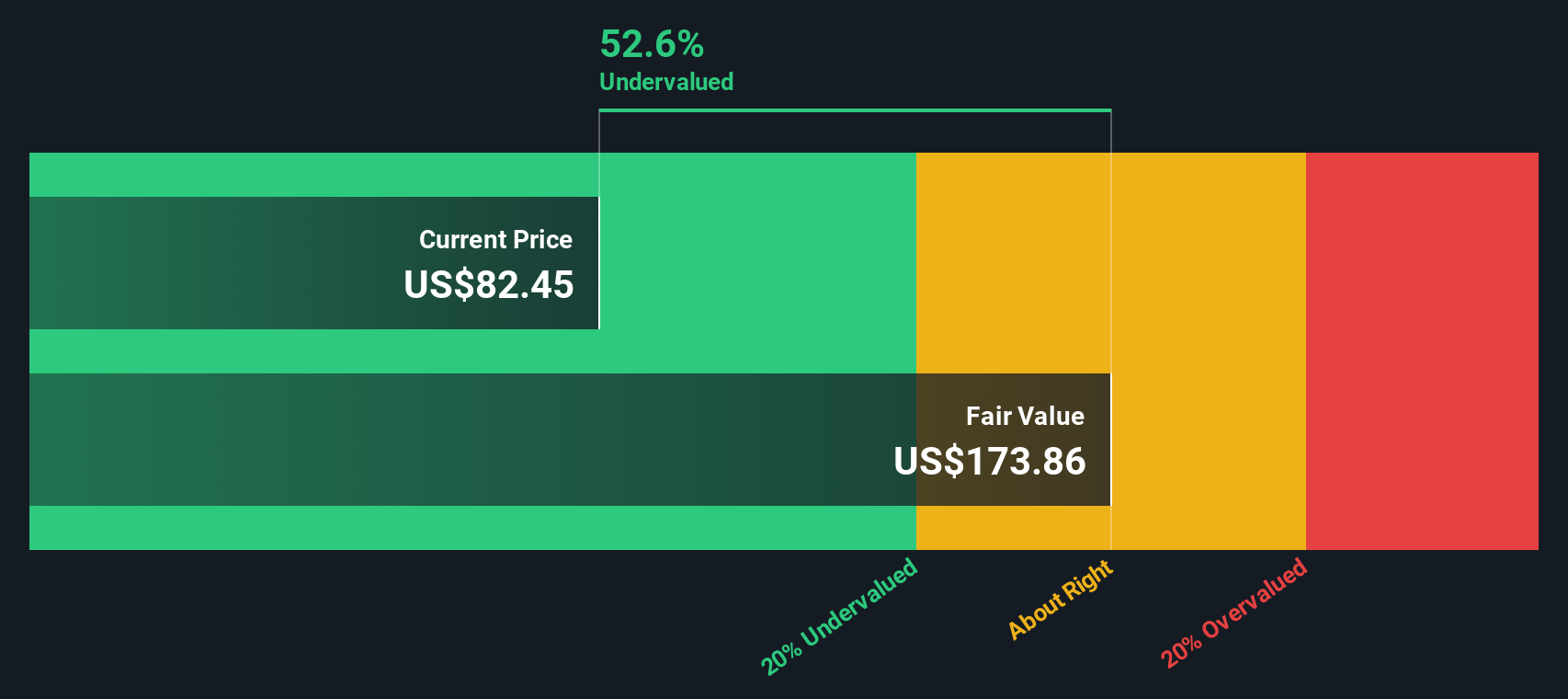

When all those future cash flows are discounted back, the model points to an intrinsic value of about $161.94 per share. Compared with the current market price, this implies the stock is trading at a 45.1% discount to its estimated fair value, which indicates a substantial margin of safety for long term investors.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Coca-Cola FEMSA. de is undervalued by 45.1%. Track this in your watchlist or portfolio, or discover 927 more undervalued stocks based on cash flows.

Approach 2: Coca-Cola FEMSA. de Price vs Earnings

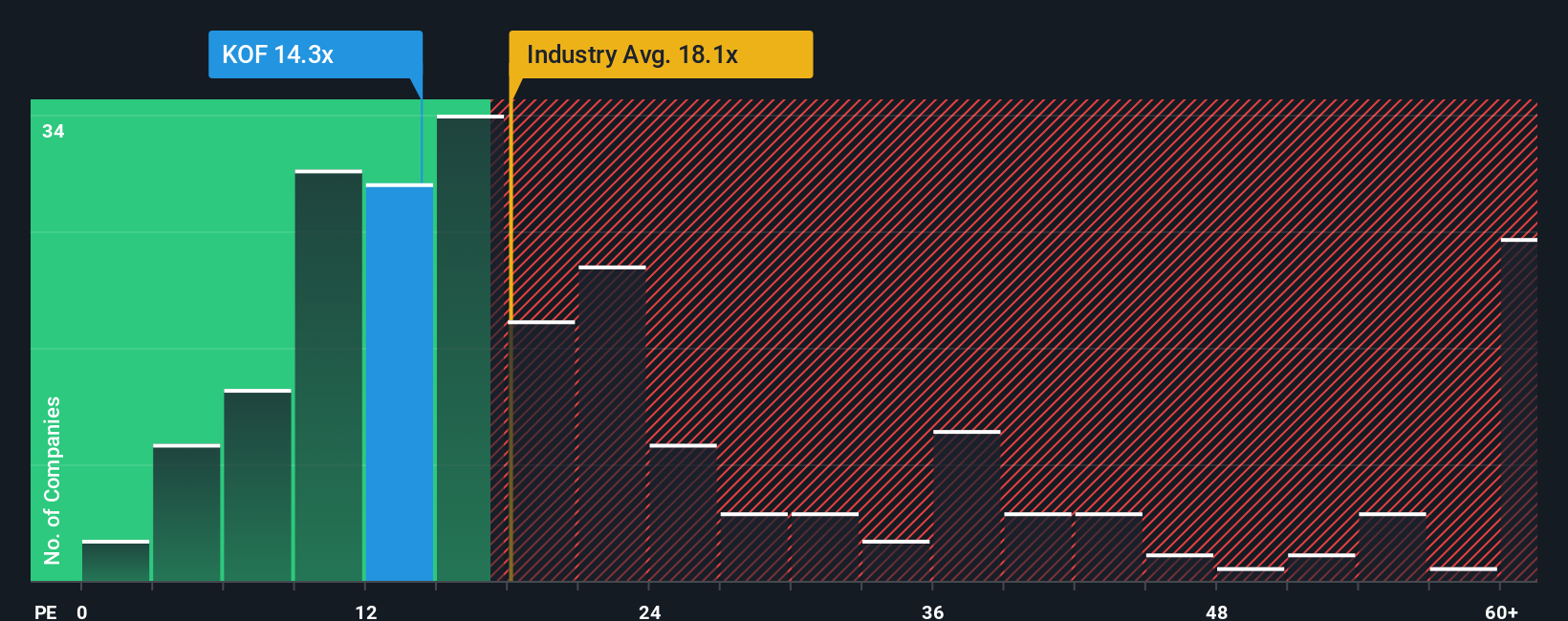

For a consistently profitable business like Coca-Cola FEMSA. de, the price to earnings ratio is a useful way to gauge value because it directly relates what investors are paying to the companys current earning power. In general, higher growth and lower risk justify a higher PE multiple, while slower growth or greater uncertainty usually call for a lower, more conservative multiple.

Coca-Cola FEMSA. de currently trades on about 14.45x earnings, which sits below both the Beverage industry average of roughly 17.85x and the broader peer group at around 33.53x. Simply Wall St also calculates a Fair Ratio of 18.45x, a proprietary estimate of what a reasonable PE should be once factors such as earnings growth, profit margins, industry dynamics, company size, and key risks are taken into account. This makes the Fair Ratio a more tailored benchmark than simple peer or industry comparisons, which can be skewed by very different business profiles.

Comparing the current 14.45x PE to the 18.45x Fair Ratio suggests the market is pricing Coca-Cola FEMSA. de at a discount relative to what its fundamentals might justify.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Coca-Cola FEMSA. de Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of a company with the numbers behind it by telling a story about its future revenue, earnings, and margins, then translating that into a financial forecast and a fair value estimate. Narratives on Simply Wall St, accessible on the Community page used by millions of investors, make this process easy by guiding you from the companys story to projected cash flows and finally to a fair value you can compare directly with todays share price to decide whether it might be a buy, hold, or sell. Because Narratives are updated dynamically when new information, such as earnings results or tax changes, is released, your valuation view stays current rather than static. For example, one Coca-Cola FEMSA. de Narrative might reflect a more optimistic perspective with a fair value around $200, while another more cautious investor could anchor their story closer to $93. Yet both are using the same framework to express different, clearly structured views on what the stock is really worth.

Do you think there's more to the story for Coca-Cola FEMSA. de? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KOF

Coca-Cola FEMSA. de

A franchise bottler, produces, markets, sells, and distributes Coca-Cola trademark beverages in Mexico, Guatemala, Nicaragua, Costa Rica, Panama, Colombia, Brazil, Argentina, and Uruguay.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

13 followersusers have followed this narrative

5 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.563.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

947 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative