Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:MPC

Newsflash: Marathon Petroleum Corporation (NYSE:MPC) Analysts Have Been Trimming Their Revenue Forecasts

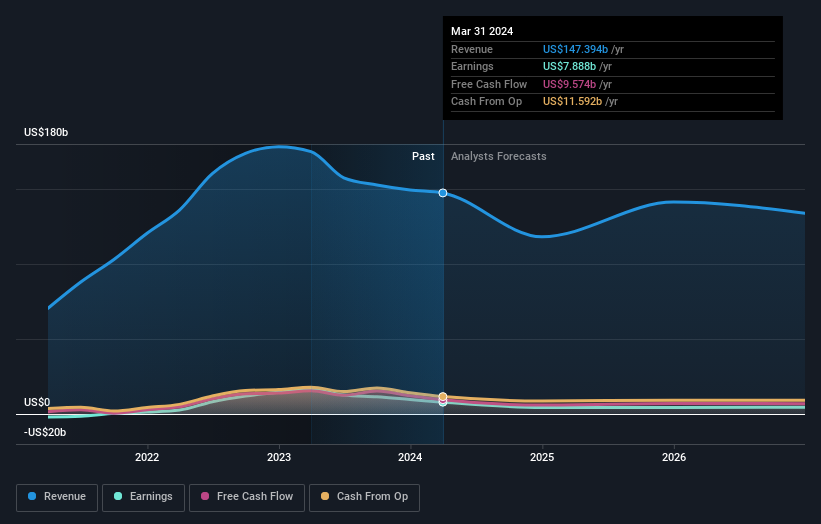

One thing we could say about the analysts on Marathon Petroleum Corporation (NYSE:MPC) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Revenue estimates were cut sharply as analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

Following the latest downgrade, the current consensus, from the 14 analysts covering Marathon Petroleum, is for revenues of US$118b in 2024, which would reflect a chunky 20% reduction in Marathon Petroleum's sales over the past 12 months. Statutory earnings per share are anticipated to crater 41% to US$13.24 in the same period. Prior to this update, the analysts had been forecasting revenues of US$140b and earnings per share (EPS) of US$13.21 in 2024. So there's been a clear change in analyst sentiment in the recent update, with the analysts making a measurable cut to revenues and reconfirming their earnings per share estimates.

View our latest analysis for Marathon Petroleum

The average price target was steady at US$193 even though revenue estimates declined; likely suggesting the analysts place a higher value on earnings.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 36% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 13% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 1.9% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Marathon Petroleum is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the stark change in sentiment, we'd understand if investors became more cautious on Marathon Petroleum after today.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with Marathon Petroleum's business, like its declining profit margins. For more information, you can click here to discover this and the 2 other risks we've identified.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MPC

Marathon Petroleum

Operates as an integrated downstream energy company in the United States.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor