- United States

- /

- Oil and Gas

- /

- NYSE:LPG

Exploring Cricut And Two Other Promising Small Caps In The US Market

Reviewed by Simply Wall St

Over the last 7 days, the United States market has dropped 1.2%, yet it remains up by an impressive 23% over the past year, with earnings forecasted to grow by 15% annually. In this dynamic environment, identifying promising small-cap stocks like Cricut and others can offer unique opportunities for investors seeking growth potential amidst broader market trends.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Eagle Financial Services | 170.75% | 12.30% | 1.92% | ★★★★★★ |

| Omega Flex | NA | 0.39% | 2.57% | ★★★★★★ |

| Franklin Financial Services | 173.21% | 5.55% | -1.86% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Morris State Bancshares | 10.20% | -0.28% | 6.97% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.65% | 11.17% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 7.11% | -35.88% | ★★★★★☆ |

| Pure Cycle | 5.15% | -2.61% | -6.23% | ★★★★★☆ |

| FRMO | 0.13% | 19.43% | 29.70% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

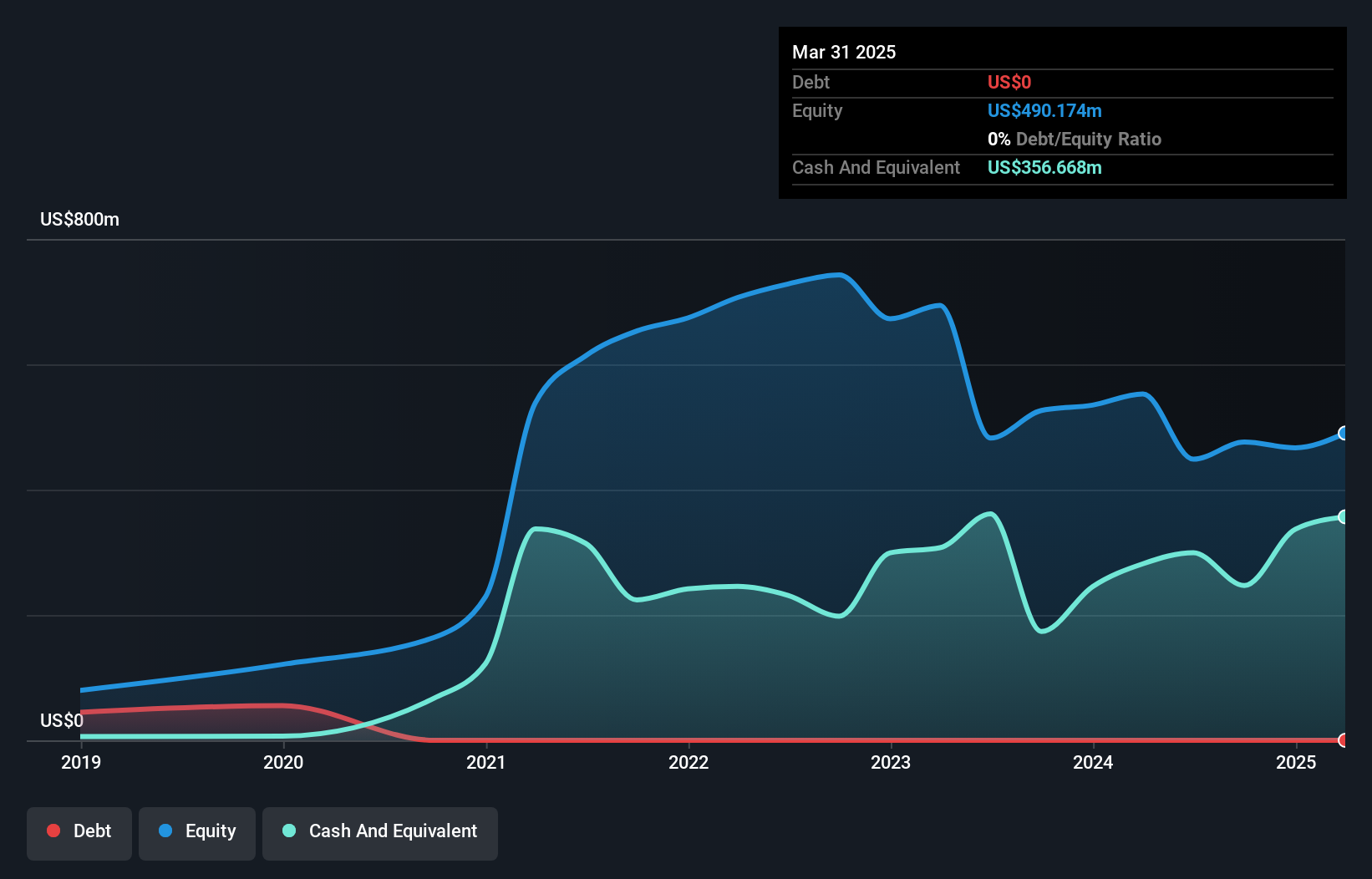

Cricut (NasdaqGS:CRCT)

Simply Wall St Value Rating: ★★★★★★

Overview: Cricut, Inc. is involved in designing, marketing, and distributing a creativity platform that empowers users to create professional-looking handmade goods, with a market capitalization of approximately $1.23 billion.

Operations: Cricut generates revenue primarily through the sale of connected machines and related accessories, as well as subscriptions for its design software. The company has reported fluctuations in its net profit margin over recent periods, reflecting changes in operational efficiencies and market conditions.

Cricut stands out for its financial resilience, operating debt-free with a significant reduction from a 47.6% debt-to-equity ratio five years ago. Despite earnings declining by 22.2% annually over the past five years, recent growth of 16.8% surpasses industry averages, showcasing potential recovery momentum. The company repurchased shares worth $19.2 million in the latest buyback initiative and trades at an attractive valuation, estimated to be 57.1% below fair value estimates. With strong free cash flow and high-quality earnings, Cricut's strategic moves like dividends and buybacks suggest confidence in its financial health and future prospects.

- Click to explore a detailed breakdown of our findings in Cricut's health report.

Understand Cricut's track record by examining our Past report.

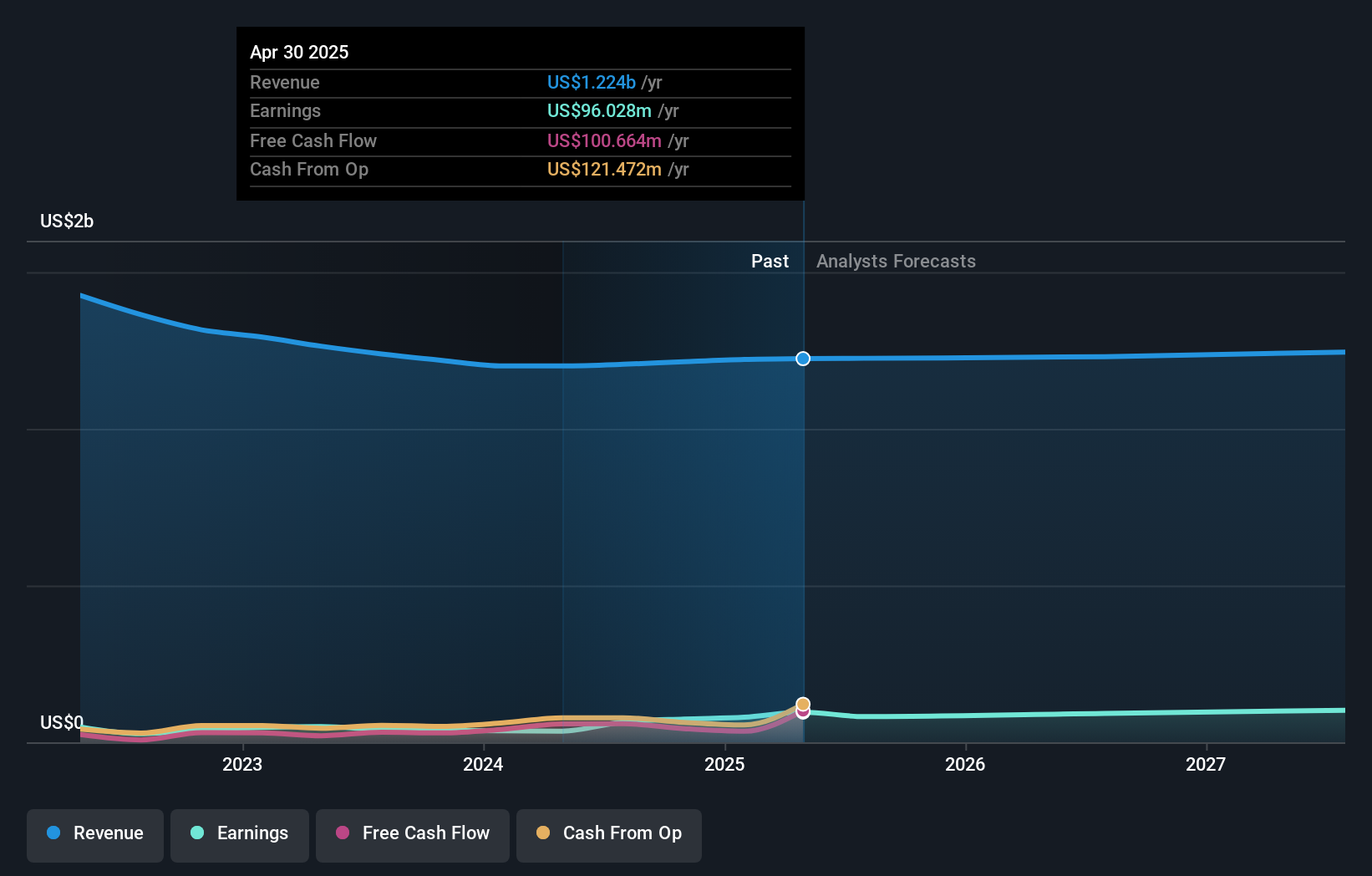

IDT (NYSE:IDT)

Simply Wall St Value Rating: ★★★★★★

Overview: IDT Corporation offers a range of communications and payment services across the United States, the United Kingdom, and other international markets, with a market capitalization of approximately $1.19 billion.

Operations: IDT generates revenue primarily from its Traditional Communications segment, which accounts for $889.39 million, followed by Fintech at $131.23 million and National Retail Solutions (NRS) at $109.51 million. The Net2phone segment contributes $84.02 million to the overall revenue stream, highlighting a diverse income model across various service offerings.

IDT Corporation, a dynamic player in the telecom sector, is catching attention with its robust financial health and strategic moves. The company reported impressive earnings growth of 99.3% over the past year, outpacing the industry average by a significant margin. Trading at 33.3% below its estimated fair value suggests potential upside for investors. IDT's debt-free status enhances its appeal, indicating strong fiscal management and stability. Recent buybacks of 37,714 shares for US$1.34 million reflect confidence in long-term prospects while maintaining high-quality earnings through non-cash contributions further solidifies its market position.

- Dive into the specifics of IDT here with our thorough health report.

Assess IDT's past performance with our detailed historical performance reports.

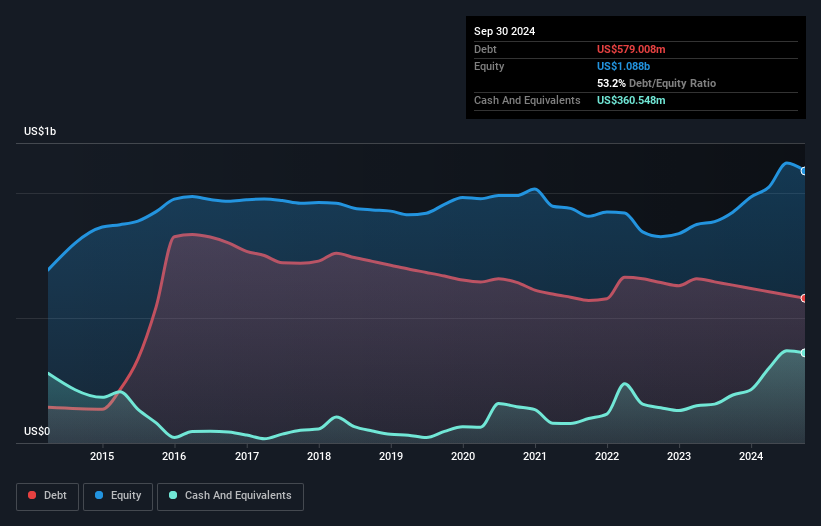

DorianG (NYSE:LPG)

Simply Wall St Value Rating: ★★★★★☆

Overview: Dorian LPG Ltd., along with its subsidiaries, operates in the global transportation of liquefied petroleum gas using its fleet of LPG tankers and has a market capitalization of approximately $1.15 billion.

Operations: DorianG generates revenue primarily from the international transportation of liquefied petroleum gas, totaling approximately $498.83 million. The company has a market capitalization of around $1.15 billion.

DorianG, a smaller player in the LPG shipping industry, is navigating a challenging landscape with strategic moves like expanding U.S. LPG terminals and adding ammonia-capable vessels. Despite these efforts to boost capacity and operational efficiency, the company faces hurdles such as potential weather disruptions and reliance on the Panama Canal. Financially, DorianG's net debt to equity ratio stands at 20.1%, indicating a satisfactory debt level while maintaining high-quality earnings with EBIT covering interest payments tenfold. However, projected revenue declines of 15.6% annually over three years suggest caution; analysts' price targets range from US$29 to US$42 per share.

Turning Ideas Into Actions

- Gain an insight into the universe of 248 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LPG

DorianG

Engages in the transportation of liquefied petroleum gas through its LPG tankers worldwide.

Very undervalued with excellent balance sheet and pays a dividend.