- United States

- /

- Oil and Gas

- /

- NYSE:COP

Shareholders Will Probably Hold Off On Increasing ConocoPhillips' (NYSE:COP) CEO Compensation For The Time Being

Key Insights

- ConocoPhillips to hold its Annual General Meeting on 14th of May

- Salary of US$1.74m is part of CEO Ryan Lance's total remuneration

- The overall pay is 43% above the industry average

- ConocoPhillips' EPS grew by 699% over the past three years while total shareholder return over the past three years was 149%

CEO Ryan Lance has done a decent job of delivering relatively good performance at ConocoPhillips (NYSE:COP) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 14th of May. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for ConocoPhillips

How Does Total Compensation For Ryan Lance Compare With Other Companies In The Industry?

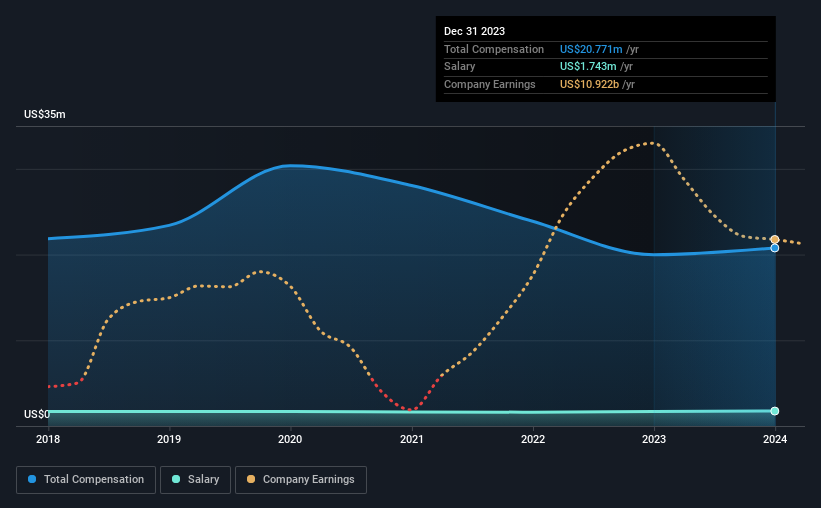

According to our data, ConocoPhillips has a market capitalization of US$144b, and paid its CEO total annual compensation worth US$21m over the year to December 2023. That's a fairly small increase of 4.0% over the previous year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$1.7m.

On comparing similar companies in the American Oil and Gas industry with market capitalizations above US$8.0b, we found that the median total CEO compensation was US$15m. Hence, we can conclude that Ryan Lance is remunerated higher than the industry median. Furthermore, Ryan Lance directly owns US$13m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.7m | US$1.7m | 8% |

| Other | US$19m | US$18m | 92% |

| Total Compensation | US$21m | US$20m | 100% |

Speaking on an industry level, nearly 14% of total compensation represents salary, while the remainder of 86% is other remuneration. ConocoPhillips sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at ConocoPhillips' Growth Numbers

ConocoPhillips's earnings per share (EPS) grew 699% per year over the last three years. In the last year, its revenue is down 27%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's always a tough situation when revenues are not growing, but ultimately profits are more important. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has ConocoPhillips Been A Good Investment?

Most shareholders would probably be pleased with ConocoPhillips for providing a total return of 149% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 2 warning signs for ConocoPhillips that investors should look into moving forward.

Important note: ConocoPhillips is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade ConocoPhillips, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:COP

ConocoPhillips

Explores for, produces, transports, and markets crude oil, bitumen, natural gas, liquefied natural gas (LNG), and natural gas liquids.

Undervalued with excellent balance sheet and pays a dividend.