Advertisement

- United States

- /

- Oil and Gas

- /

- NasdaqGS:CLMT

Should Calumet’s (CLMT) Analyst Downgrade and Weak Earnings Prompt a Reassessment by Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Zacks Research downgraded Calumet (NASDAQ:CLMT) to a strong sell, following quarterly earnings that came in below analysts’ consensus estimates.

- This shift in analyst sentiment highlights growing uncertainty around the company’s near-term performance and reflects heightened caution regarding its earnings potential.

- We’ll assess how this analyst downgrade and weaker earnings performance affect Calumet’s investment narrative and outlook for margin resilience.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

Calumet Investment Narrative Recap

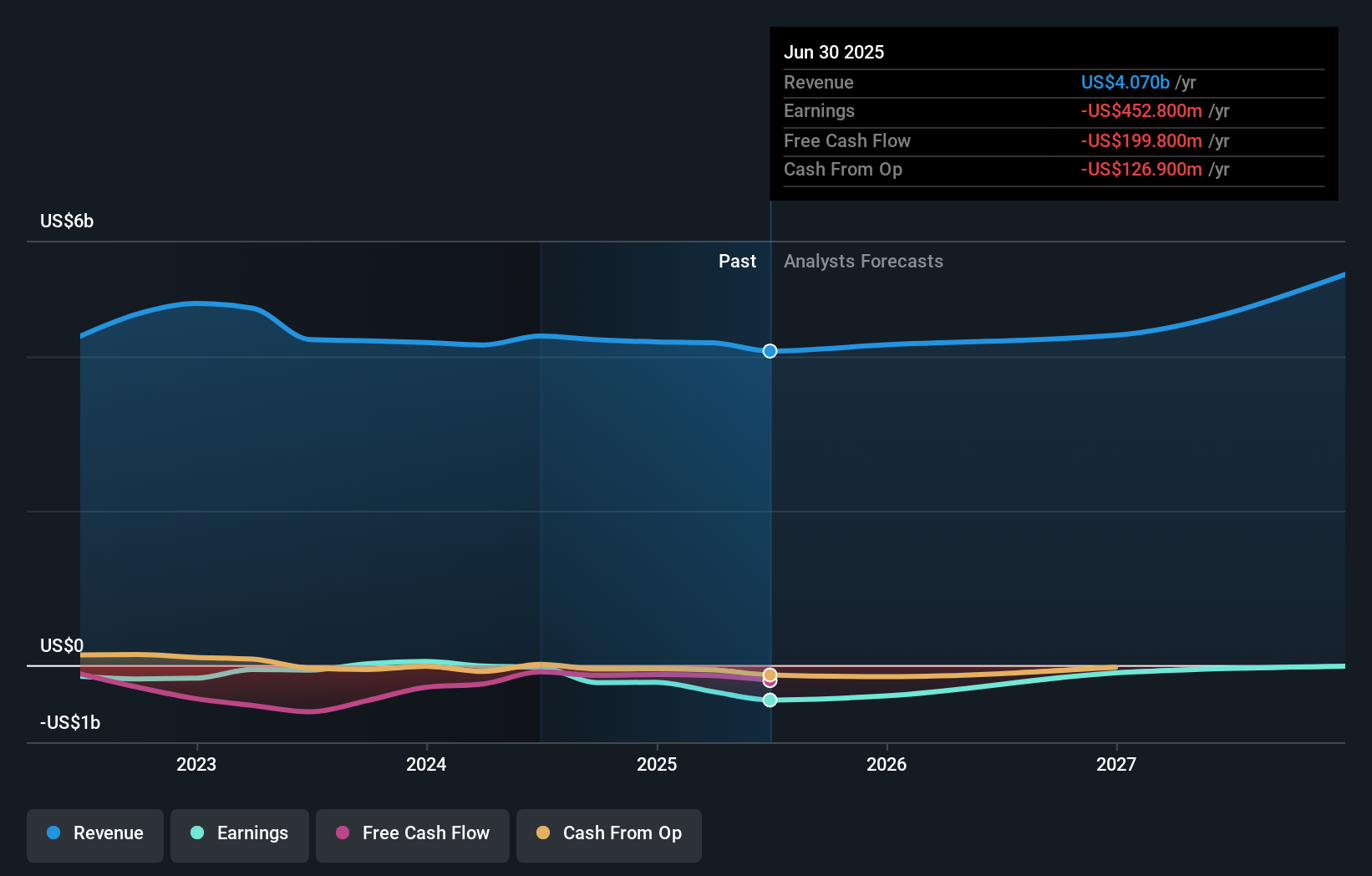

To be a shareholder in Calumet, you generally need to believe in a rebound in renewables profitability, resilient margins for specialty products, and successful debt reduction, anchored by execution of major projects like MaxSAF 150. Zacks Research’s downgrade to strong sell, coming after weaker-than-expected earnings, raises concerns about Calumet’s ability to deliver near-term margin improvements and amplifies the biggest risk: pressure on margins if regulatory support for renewables falters. While this shift is serious, the core long-term catalysts, like the MaxSAF 150 project, still underpin the investment case unless earnings weakness persists or intensifies. One recent announcement with strong relevance is the Q2 2025 earnings release, where Calumet reported a net loss of US$147.9 million despite ongoing cost-reduction efforts. This earnings shortfall is a key factor in the shift in analyst sentiment and highlights operational and regulatory headwinds that may directly impact Calumet’s progress on high-profile initiatives such as expanding renewable fuel capacity. However, investors should be aware that for all the focus on future growth, mounting debt and cash flow constraints remain a critical source of risk if...

Read the full narrative on Calumet (it's free!)

Calumet's narrative projects $5.1 billion revenue and $40.3 million earnings by 2028. This requires 8.0% yearly revenue growth and a $493.1 million increase in earnings from -$452.8 million.

Uncover how Calumet's forecasts yield a $19.05 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Calumet range widely from US$19.05 to US$52.30, based on three distinct member analyses. Persistent margin risk tied to evolving regulatory support is a factor that may influence these diverse outlooks, making it important to consider multiple viewpoints before forming your own.

Explore 3 other fair value estimates on Calumet - why the stock might be worth just $19.05!

Build Your Own Calumet Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Calumet research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Calumet research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Calumet's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CLMT

Calumet

Manufactures, formulates, and markets a diversified slate of specialty branded products and renewable fuels to various consumer-facing and industrial markets in North America and internationally.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor