- United States

- /

- Capital Markets

- /

- NYSEAM:CET

US Market's Top 3 Undiscovered Gems With Strong Potential

Reviewed by Simply Wall St

The United States market has shown robust performance, climbing 2.9% in the last 7 days and rising by 11% over the past year, with earnings projected to grow by 14% annually. In such a dynamic environment, identifying stocks with strong potential often involves looking for companies that are not only underappreciated but also positioned to benefit from sustained growth trends.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 9.72% | 4.93% | 6.51% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Oakworth Capital | 31.49% | 14.78% | 4.46% | ★★★★★★ |

| Cashmere Valley Bank | 15.62% | 5.80% | 3.51% | ★★★★★★ |

| Omega Flex | NA | -0.52% | 0.74% | ★★★★★★ |

| Teekay | NA | -0.89% | 62.53% | ★★★★★★ |

| Anbio Biotechnology | NA | 8.43% | 184.88% | ★★★★★★ |

| Pure Cycle | 5.15% | -2.61% | -6.23% | ★★★★★☆ |

| First IC | 38.58% | 9.04% | 14.76% | ★★★★☆☆ |

| Reitar Logtech Holdings | 31.39% | 231.46% | 41.38% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

Value Line (NasdaqCM:VALU)

Simply Wall St Value Rating: ★★★★★★

Overview: Value Line, Inc. is involved in producing and selling investment periodicals and related publications, with a market cap of approximately $358.19 million.

Operations: The company generates revenue primarily from its publishing segment, which amounts to $35.70 million.

Trading just below its estimated fair value, Value Line stands out with no debt over the past five years and a consistent 1.6% annual earnings growth. Despite a recent dip in quarterly revenue to US$8.97 million from US$9.13 million, net income for the nine months rose to US$16.74 million from US$14.23 million, showcasing resilience and high-quality earnings. The company declared a quarterly dividend of $0.30 per share, reflecting stable shareholder returns amidst industry challenges where its 17.8% earnings growth aligns with market averages, hinting at steady performance potential in the capital markets sector.

- Click here and access our complete health analysis report to understand the dynamics of Value Line.

Assess Value Line's past performance with our detailed historical performance reports.

Ituran Location and Control (NasdaqGS:ITRN)

Simply Wall St Value Rating: ★★★★★★

Overview: Ituran Location and Control Ltd. offers location-based telematics services and machine-to-machine telematics products, with a market capitalization of approximately $749.19 million.

Operations: Ituran generates revenue primarily from telematics services and products, with telematics services contributing $242.49 million and telematics products adding $93.77 million.

Ituran Location and Control, a nimble player in the telematics space, has demonstrated robust financial health with earnings growing at an impressive 34% annually over the past five years. The company's debt to equity ratio has impressively decreased from 50% to just 0.06%, highlighting effective debt management. Recent earnings for Q4 2024 showed revenue at US$82.88 million and net income of US$13.84 million, both showing year-over-year growth. With a dividend increase to US$10 million per quarter reflecting strong cash flow, Ituran's strategic partnerships and subscriber growth initiatives position it well for future expansion despite potential risks like currency volatility.

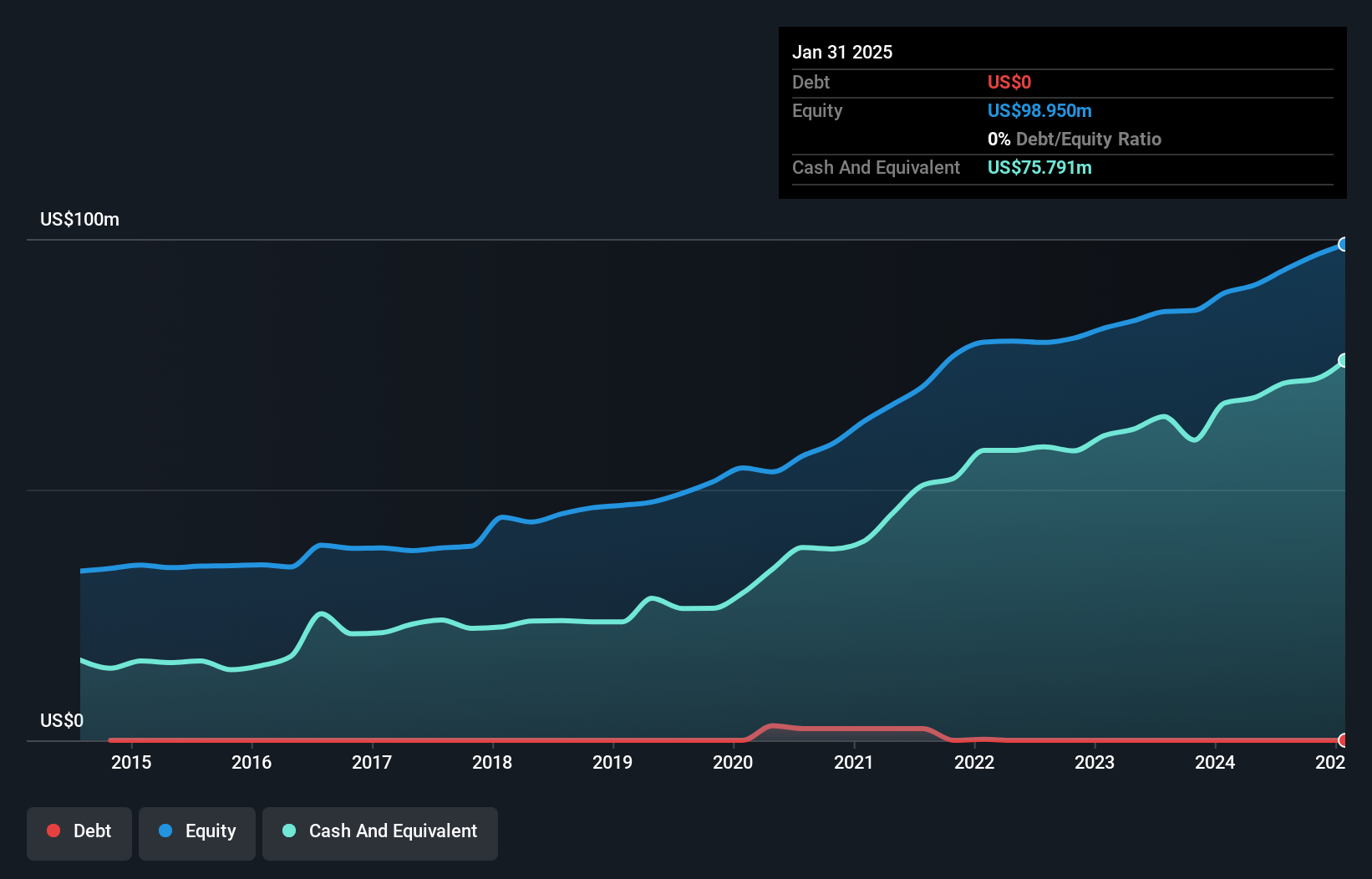

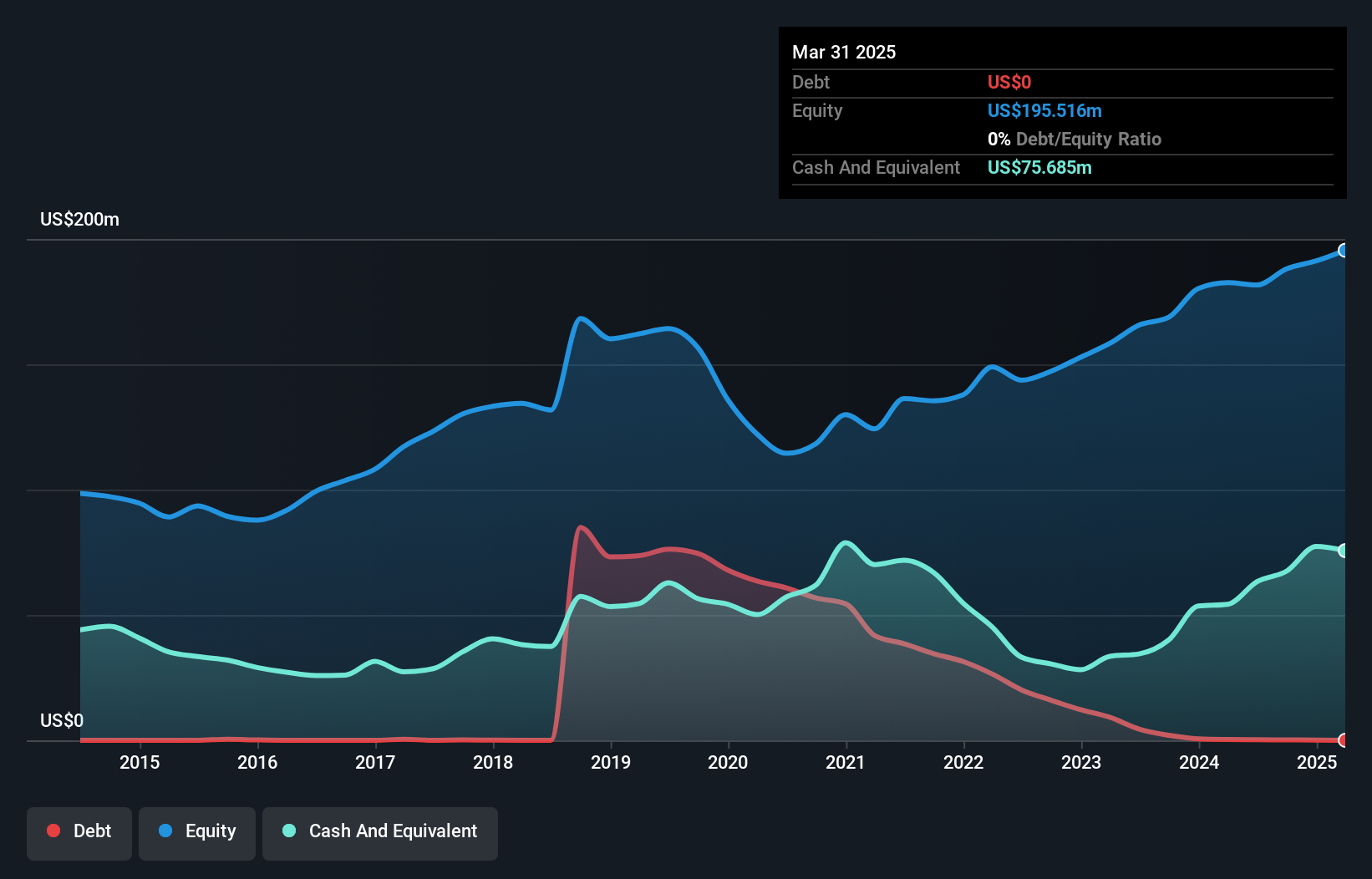

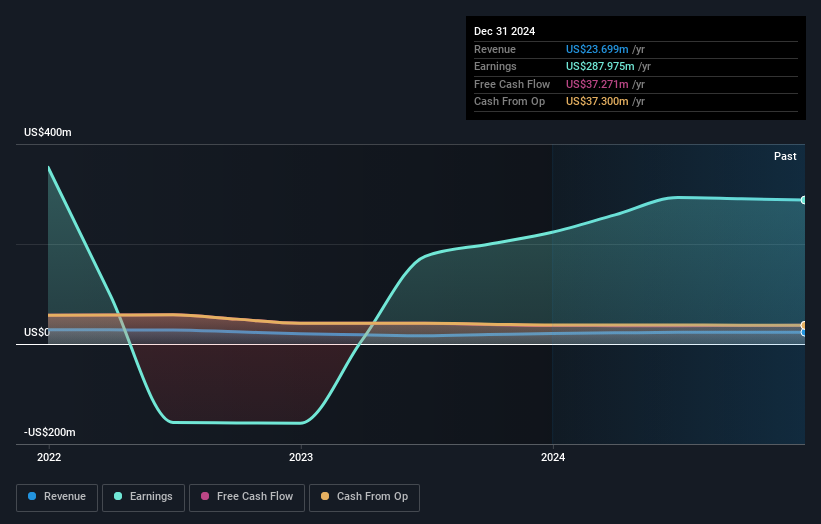

Central Securities (NYSEAM:CET)

Simply Wall St Value Rating: ★★★★★★

Overview: Central Securities Corp. is a publicly owned investment manager with a market cap of $1.32 billion.

Operations: Central Securities Corp. generates revenue primarily from its financial services segment, specifically closed-end funds, amounting to $23.70 million.

Central Securities, a nimble player in the market, has demonstrated impressive growth with earnings surging 28.8% over the past year, outpacing its industry peers at 17.8%. Trading significantly below its estimated fair value by 65.2%, it appears to offer substantial upside potential for investors seeking undervalued opportunities. The firm is debt-free and boasts high-quality earnings, although a notable one-off gain of US$272.5 million impacted recent financial results through December 2024. With positive free cash flow and no debt concerns, Central Securities seems well-positioned for future stability and growth within the capital markets sector.

Turning Ideas Into Actions

- Navigate through the entire inventory of 283 US Undiscovered Gems With Strong Fundamentals here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Central Securities, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSEAM:CET

Central Securities

Central Securities Corp. is a publicly owned investment manager.

Flawless balance sheet and good value.

Market Insights

Community Narratives