Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:SYF

Synchrony Financial (NYSE:SYF) Is Paying Out A Larger Dividend Than Last Year

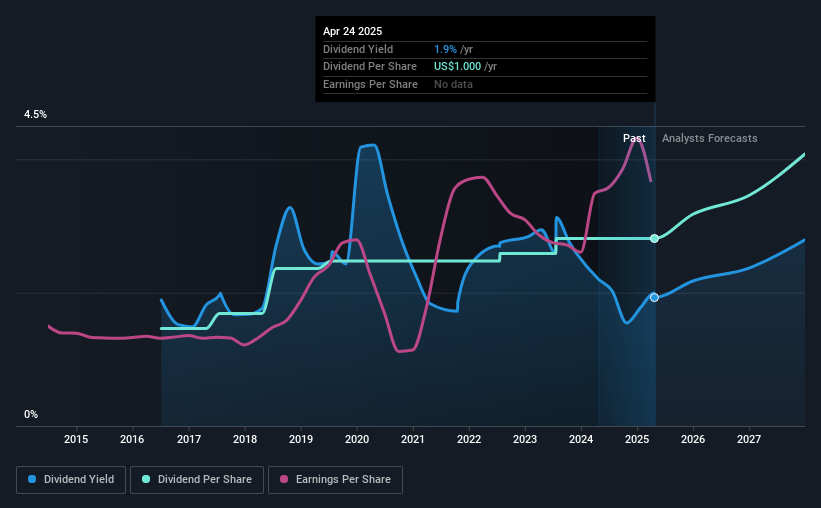

The board of Synchrony Financial (NYSE:SYF) has announced that the dividend on 15th of May will be increased to $0.30, which will be 20% higher than last year's payment of $0.25 which covered the same period. Based on this payment, the dividend yield for the company will be 1.9%, which is fairly typical for the industry.

We check all companies for important risks. See what we found for Synchrony Financial in our free report.Synchrony Financial's Dividend Forecasted To Be Well Covered By Earnings

Solid dividend yields are great, but they only really help us if the payment is sustainable.

Synchrony Financial has established itself as a dividend paying company, given its 9-year history of distributing earnings to shareholders. While past data isn't a guarantee for the future, Synchrony Financial's latest earnings report puts its payout ratio at 14%, showing that the company can pay out its dividends comfortably.

Over the next 3 years, EPS is forecast to expand by 20.7%. The future payout ratio could be 16% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Check out our latest analysis for Synchrony Financial

Synchrony Financial Is Still Building Its Track Record

It is great to see that Synchrony Financial has been paying a stable dividend for a number of years now, however we want to be a bit cautious about whether this will remain true through a full economic cycle. The dividend has gone from an annual total of $0.52 in 2016 to the most recent total annual payment of $1.00. This implies that the company grew its distributions at a yearly rate of about 7.5% over that duration. Synchrony Financial has been growing its dividend at a decent rate, and the payments have been stable. However, the payment history is very short, so there is no evidence yet that the dividend can be sustained over a full economic cycle.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that Synchrony Financial has been growing its earnings per share at 11% a year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Synchrony Financial's prospects of growing its dividend payments in the future.

Synchrony Financial Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Earnings growth generally bodes well for the future value of company dividend payments. See if the 16 Synchrony Financial analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SYF

Synchrony Financial

Operates as a consumer financial services company in the United States.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor