Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:RM

Regional Management (NYSE:RM) Is Due To Pay A Dividend Of $0.30

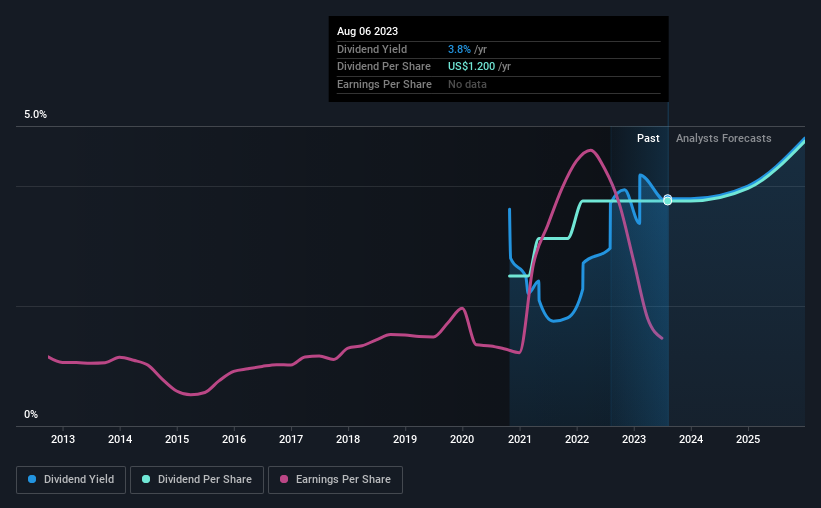

Regional Management Corp. (NYSE:RM) will pay a dividend of $0.30 on the 14th of September. This means the annual payment is 3.8% of the current stock price, which is above the average for the industry.

View our latest analysis for Regional Management

Regional Management's Dividend Is Well Covered By Earnings

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last payment, Regional Management was quite comfortably earning enough to cover the dividend. This indicates that quite a large proportion of earnings is being invested back into the business.

Looking forward, earnings per share is forecast to rise by 160.3% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could be 17% by next year, which is in a pretty sustainable range.

Regional Management Doesn't Have A Long Payment History

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 3 years, which isn't that long in the grand scheme of things. Since 2020, the annual payment back then was $0.80, compared to the most recent full-year payment of $1.20. This implies that the company grew its distributions at a yearly rate of about 14% over that duration. The dividend has been growing rapidly, however with such a short payment history we can't know for sure if payment can continue to grow over the long term, so caution may be warranted.

Regional Management May Find It Hard To Grow The Dividend

The company's investors will be pleased to have been receiving dividend income for some time. However, initial appearances might be deceiving. Although it's important to note that Regional Management's earnings per share has basically not grown from where it was five years ago, which could erode the purchasing power of the dividend over time.

In Summary

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. To that end, Regional Management has 5 warning signs (and 1 which is concerning) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:RM

Regional Management

A diversified consumer finance company, provides various installment loan products primarily to customers with limited access to consumer credit from banks, thrifts, credit card companies, and other lenders in the United States.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets