Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:EVR

What Evercore (EVR)'s Expanding M&A Client Base Means for Shareholders

Simply Wall St

Reviewed by Sasha Jovanovic

- Recent reports highlighted that Evercore is expanding its advisory client base and is expected to benefit from a rebound in mergers and acquisitions activity, which could drive investment banking revenues higher in the coming quarters.

- This emphasis on growth prospects in M&A activity has drawn attention to Evercore’s positioning in the evolving global investment banking landscape.

- To assess the implications of this increasing M&A optimism, we'll examine how expanded client relationships might reinforce Evercore's investment narrative.

These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Evercore Investment Narrative Recap

To be a shareholder in Evercore right now, you need to believe in a sustained upswing in global M&A activity and the firm's ability to translate expanded client relationships into increased advisory revenues. The recent news about Evercore broadening its advisory client base supports this optimistic outlook, but the sharpest near-term catalyst, an M&A rebound, remains highly sensitive to macroeconomic and geopolitical risks, while intensifying competition and rising costs could still present meaningful headwinds. On balance, this news reinforces the growth thesis but does not materially reduce the company's largest risks at this time.

Among recent company announcements, the appointment of Alexander Virgo as a senior managing director in London stands out as especially relevant, signaling Evercore's commitment to strengthening its European platform. This hire could support client acquisition among multi-industry firms and help capture a greater share of advisory fee pools as M&A markets recover.

By contrast, investors should also keep in mind that as fixed costs rise with office expansions and talent hiring, any slowdown in deal activity could quickly pressure net margins and...

Read the full narrative on Evercore (it's free!)

Evercore's narrative projects $5.4 billion revenue and $953.1 million earnings by 2028. This requires 18.7% yearly revenue growth and a $490.9 million earnings increase from $462.2 million currently.

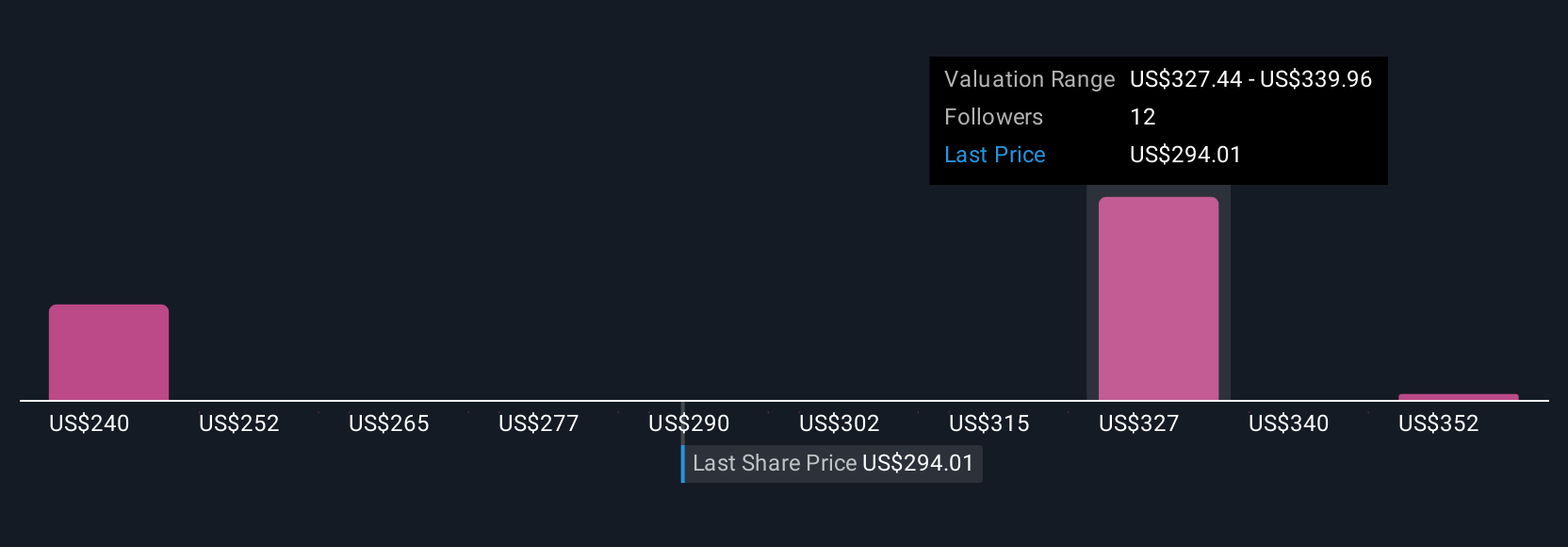

Uncover how Evercore's forecasts yield a $369.00 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community set fair value estimates for Evercore ranging from US$226 to US$369 per share. While these opinions vary widely, rising non-compensation expenses and ongoing expansion efforts could be pivotal factors influencing long-term performance across these perspectives.

Explore 3 other fair value estimates on Evercore - why the stock might be worth 28% less than the current price!

Build Your Own Evercore Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Evercore research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Evercore research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Evercore's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evercore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EVR

Evercore

Operates as an independent investment banking firm in the Americas, Europe, Middle East, Africa, and Asia-Pacific.

High growth potential with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.4% undervalued

TR

Community Contributor