Advertisement

- United States

- /

- Consumer Finance

- /

- NasdaqGS:QFIN

Can Qfin Holdings' (QFIN) Expanding Consumer Base Reinforce Its Long-Term Competitive Advantage?

Simply Wall St

Reviewed by Sasha Jovanovic

- Qfin Holdings released its unaudited fiscal second quarter results for 2025 in August, highlighting an 11.4% increase in platform consumers from the previous year, growing from 247.6 million to 275.8 million.

- This surge in consumer numbers comes as several analysts, including DBS and J.P. Morgan, reiterated their positive ratings for the company following the results.

- We'll now examine how the consumer growth highlighted in the recent results could reshape Qfin Holdings' investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Qfin Holdings Investment Narrative Recap

To be a shareholder of Qfin Holdings, you need to believe that large-scale consumer growth, combined with effective technology integration, can offset ongoing regulatory and credit challenges in China’s consumer finance sector. The recent surge in platform consumers may support the short-term outlook for loan origination and revenue, but does not materially reduce the biggest risk at present: uncertainty from the anticipated regulatory tightening and new lending rules in October that could still impact growth and margins.

Among the recent announcements, the fiscal second quarter results reported in August stand out as most relevant. Not only did Qfin report an 11.4% growth in its consumer base, but revenue and net income also rose significantly year over year, pointing to operational momentum even as regulatory headwinds loom. These numbers reinforce the key catalyst of ongoing digital channel expansion, which management emphasizes as central to future growth against an uncertain backdrop.

However, investors should remain aware that even strong consumer growth may not fully offset the effects of...

Read the full narrative on Qfin Holdings (it's free!)

Qfin Holdings' outlook anticipates CN¥23.0 billion in revenue and CN¥8.4 billion in earnings by 2028. To achieve this, analysts expect a 7.0% annual revenue growth rate and a CN¥1.1 billion earnings increase from the current CN¥7.3 billion.

Uncover how Qfin Holdings' forecasts yield a $49.30 fair value, a 77% upside to its current price.

Exploring Other Perspectives

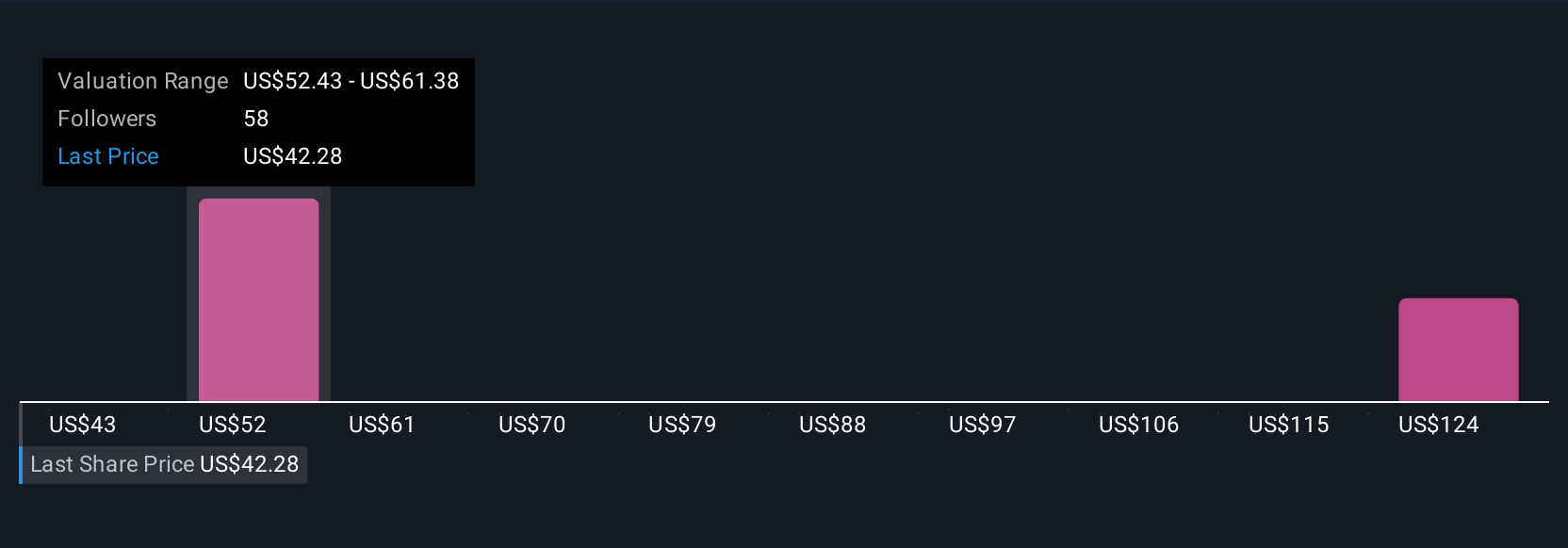

A dozen Simply Wall St Community members estimate Qfin’s fair value between US$36.30 and US$120.19 per share. While platform growth is accelerating, looming regulatory changes could challenge profitability, so consider a range of views before making any conclusions.

Explore 12 other fair value estimates on Qfin Holdings - why the stock might be worth just $36.30!

Build Your Own Qfin Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Qfin Holdings research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Qfin Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Qfin Holdings' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Qfin Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:QFIN

Qfin Holdings

Qfin Holdings, Inc., together with its subsidiaries, operate AI- driven credit-tech platform under the Qifu Jietiao brand in the People’s Republic of China.

Very undervalued with outstanding track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor