- United States

- /

- Hospitality

- /

- NYSE:YUMC

Do Its Financials Have Any Role To Play In Driving Yum China Holdings, Inc.'s (NYSE:YUMC) Stock Up Recently?

Yum China Holdings (NYSE:YUMC) has had a great run on the share market with its stock up by a significant 44% over the last three months. As most would know, fundamentals are what usually guide market price movements over the long-term, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. Particularly, we will be paying attention to Yum China Holdings' ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Yum China Holdings

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Yum China Holdings is:

14% = US$961m ÷ US$6.7b (Based on the trailing twelve months to September 2024).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.14 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Yum China Holdings' Earnings Growth And 14% ROE

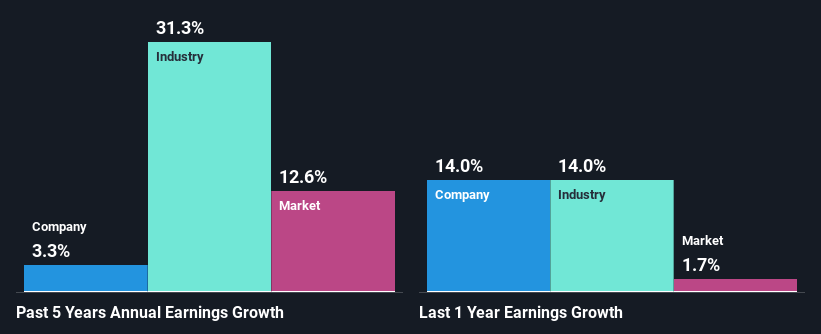

To begin with, Yum China Holdings seems to have a respectable ROE. Further, the company's ROE is similar to the industry average of 12%. Despite the modest returns, Yum China Holdings' five year net income growth was quite low, averaging at only 3.3%. So, there could be some other factors at play that could be impacting the company's growth. For instance, the company pays out a huge portion of its earnings as dividends, or is faced with competitive pressures.

Next, on comparing with the industry net income growth, we found that Yum China Holdings' reported growth was lower than the industry growth of 31% over the last few years, which is not something we like to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is YUMC fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Yum China Holdings Making Efficient Use Of Its Profits?

Despite having a moderate three-year median payout ratio of 27% (implying that the company retains the remaining 73% of its income), Yum China Holdings' earnings growth was quite low. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

Moreover, Yum China Holdings has been paying dividends for seven years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 29% of its profits over the next three years. Regardless, the future ROE for Yum China Holdings is predicted to rise to 17% despite there being not much change expected in its payout ratio.

Conclusion

Overall, we feel that Yum China Holdings certainly does have some positive factors to consider. Yet, the low earnings growth is a bit concerning, especially given that the company has a high rate of return and is reinvesting ma huge portion of its profits. By the looks of it, there could be some other factors, not necessarily in control of the business, that's preventing growth. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you're looking to trade Yum China Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:YUMC

Yum China Holdings

Owns, operates, and franchises restaurants in the People’s Republic of China.

Undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives