- United States

- /

- Hospitality

- /

- NYSE:RCL

Royal Caribbean Cruises (NYSE:RCL) Upsizes Credit Facilities To US$6.35 Billion

Reviewed by Simply Wall St

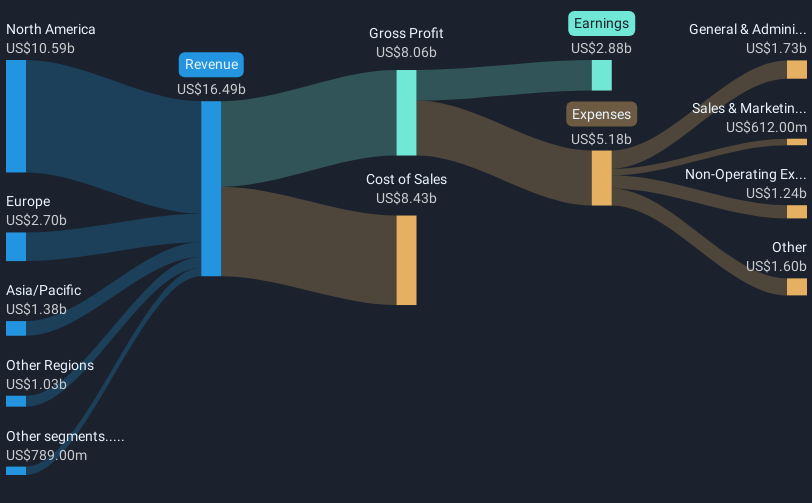

Royal Caribbean Cruises (NYSE:RCL) announced significant amendments to its credit facilities, increasing commitments by $2.28 billion and extending maturities, which could provide greater financial flexibility. This development aligns with a period of favorable market performance, where the S&P 500, Dow Jones, and Nasdaq Composite experienced gains, supported by easing global trade tensions and encouraging U.S. economic data. The company's recent earnings growth, alongside a declared dividend and a completed share buyback, offer additional positive signals. While Royal Caribbean's 31% share price increase outpaced the broader market, these events likely added weight to the upward movement.

We've spotted 2 risks for Royal Caribbean Cruises you should be aware of.

The amendments to Royal Caribbean Cruises' credit facilities enhance its financial flexibility, potentially strengthening its capacity for ongoing investments in new ships and private destinations. These developments could support the narrative of expanding markets and increased per-passenger spending, aligning with earnings growth and revenue initiatives. Over the past five years, the company has delivered a very large total return of 522.20%, reflecting significant appreciation in shareholder value. Over the past year, Royal Caribbean outperformed the US Hospitality industry, which returned 13.2%, further emphasizing its effective positioning within the sector.

Analysts project robust revenue and earnings growth bolstered by increased spending on new experiences, although macroeconomic uncertainties could pose risks. The 31% share price rise over recent periods underlines a buoyant market perception, yet it is still at a 5.13% discount to the consensus price target of US$264.26. Despite strong recent performance, risks such as consumer spending decline or shifts in competitive pricing remain potential challenges to forecasted growth. The share price movement in relation to the consensus target suggests room for further valuation alignment, contingent on meeting earnings expectations.

Assess Royal Caribbean Cruises' previous results with our detailed historical performance reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Royal Caribbean Cruises, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RCL

Undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives