Advertisement

- United States

- /

- Hospitality

- /

- NYSE:QSR

A Fresh Look at Restaurant Brands International (NYSE:QSR) Valuation After Mini-Tender Offer Warning and Earnings Divergence

Simply Wall St

Reviewed by Kshitija Bhandaru

Restaurant Brands International (NYSE:QSR) has issued a public warning to shareholders about an unsolicited mini-tender offer from Ocehan LLC, which is attempting to buy up to 50,000 company shares at prices well below the current market value. The company is advising shareholders to steer clear because this offer is not endorsed by Restaurant Brands International and poses risks to investors who may not realize the discount. This event highlights shareholder risks and raises questions about how outside parties are valuing the company compared to its own business fundamentals.

This warning comes at a time when Restaurant Brands International has already been on investors’ radar for other reasons. While core international segments like Tim Hortons Canada and Burger King China are delivering growth, the company’s U.S. operations have lagged and valuation pressure has become more visible, especially this year. The stock is down about 5.8% over the year, and short-term performance has edged lower even as revenue and net income have seen positive momentum. The mixed signals between ongoing global growth and sluggish U.S. results are sparking debate about the company’s longer-term potential.

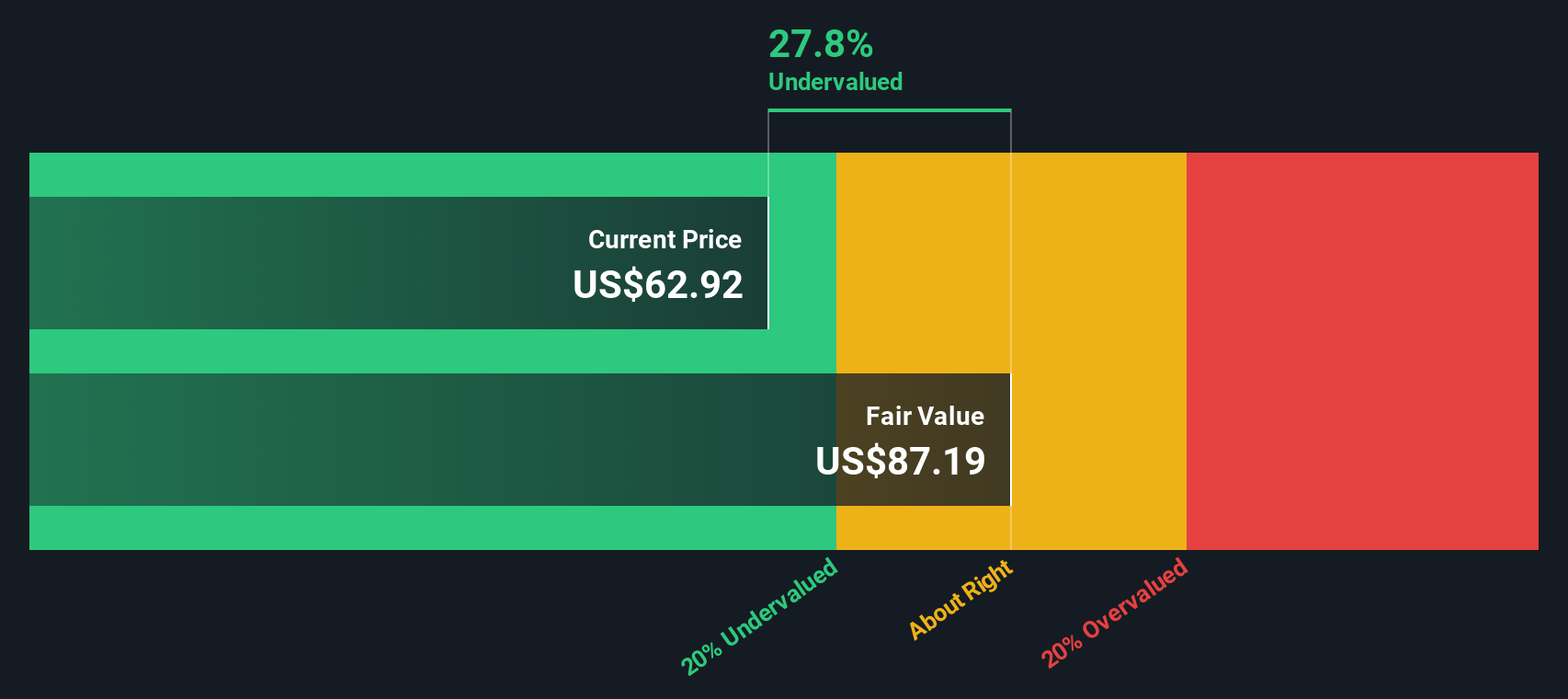

After the dip in the share price and this latest shareholder development, some are questioning whether Restaurant Brands International is being undervalued, or if the market is already accounting for future challenges and opportunities.

Most Popular Narrative: 15.9% Undervalued

Analyst consensus suggests Restaurant Brands International is trading at a considerable discount to its fair value, with substantial room for upside if targets are hit.

Rapid international expansion, particularly through the franchise-led model in markets such as China, India, Turkey, Japan, and Brazil, is driving double-digit unit and system-wide sales growth. This directly supports recurring, capital-light revenue streams and higher long-term earnings visibility.

Curious about why top analysts think this company’s value is set to surge? Dig into the financial playbook behind its global growth strategy and see which powerful assumptions are shaping its sky-high price target. Hungry to discover the narrative fueling expectations of outperformance? The numbers and logic are more surprising than you might expect.

Result: Fair Value of $76.32 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent cost inflation and unexpected setbacks in international expansion could quickly undermine the optimistic outlook for Restaurant Brands International’s future growth.

Find out about the key risks to this Restaurant Brands International narrative.Another View: Testing the Numbers

Looking through a different lens, the SWS DCF model also suggests the company is trading below its intrinsic value. This supports the idea that there's room for upside. But can either model truly capture shifting consumer trends and execution risk, or is something important being missed?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Restaurant Brands International Narrative

If you think the standard view misses the mark or want to dig deeper yourself, you can assemble your own perspective in just a few minutes using our tools. Do it your way

A great starting point for your Restaurant Brands International research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors don’t stand still. Open new doors by targeting companies riding big themes and trends using our hand-picked stock lists. Miss these and you could be skipping powerful opportunities hiding in plain sight:

- Spot fast-growing global businesses set to shake up tomorrow’s economy by scanning companies primed for expansion with strong fundamentals. Use our undervalued stocks based on cash flows.

- Accelerate your potential returns and harness breakthrough tech growth by focusing on future-shaping leaders. Explore with our AI penny stocks.

- Secure steady income and gain confidence in rising market stability when you identify yield-rich companies through our dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:QSR

Restaurant Brands International

Operates as a quick-service restaurant company in Canada, the United States, and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor