Advertisement

- United States

- /

- Hospitality

- /

- NYSE:BYD

FanDuel Stake Sale and Buyback Expansion Could Be a Game Changer for Boyd Gaming (BYD)

Simply Wall St

Reviewed by Simply Wall St

- Boyd Gaming recently reported strong second-quarter results, highlighted by year-over-year growth in revenue and earnings, and announced the sale of its 5% equity stake in FanDuel to Flutter Entertainment for approximately US$1.76 billion.

- The company expanded its share repurchase program and plans to use proceeds from the FanDuel sale to reduce debt, signaling a focus on financial strength and shareholder returns.

- We'll examine how the FanDuel stake sale and buyback expansion may influence Boyd Gaming's capital allocation strategy and earnings outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Boyd Gaming Investment Narrative Recap

For those considering Boyd Gaming, the core investment narrative rests on the stability and growth potential of its regional casino operations, balanced by disciplined capital allocation. The recent sale of Boyd’s 5% equity stake in FanDuel for approximately US$1.76 billion, coupled with a buyback expansion, strengthens the balance sheet and likely enhances flexibility for growth initiatives, though it does not fundamentally shift the importance of Boyd’s ability to compete with digital gaming rivals, still the biggest risk facing the company in the near term.

Among recent developments, Boyd’s aggressive share repurchase program stands out, with 34.38% of shares retired since 2021 and an increase in buyback authorization following the FanDuel sale. This move underscores the company’s intent to return capital to shareholders, but it should be considered in light of both the benefits and opportunity costs, especially as digital competition intensifies and traditional casino market share faces pressure from online alternatives.

Yet, while buybacks continue to boost returns, investors should also ask whether discipline in capital allocation is enough to offset the persistent headwinds from...

Read the full narrative on Boyd Gaming (it's free!)

Boyd Gaming's outlook anticipates $3.5 billion in revenue and $556.3 million in earnings by 2028. This scenario reflects a 4.3% annual revenue decline and a decrease of $8.2 million in earnings from the current $564.5 million.

Uncover how Boyd Gaming's forecasts yield a $89.92 fair value, a 4% upside to its current price.

Exploring Other Perspectives

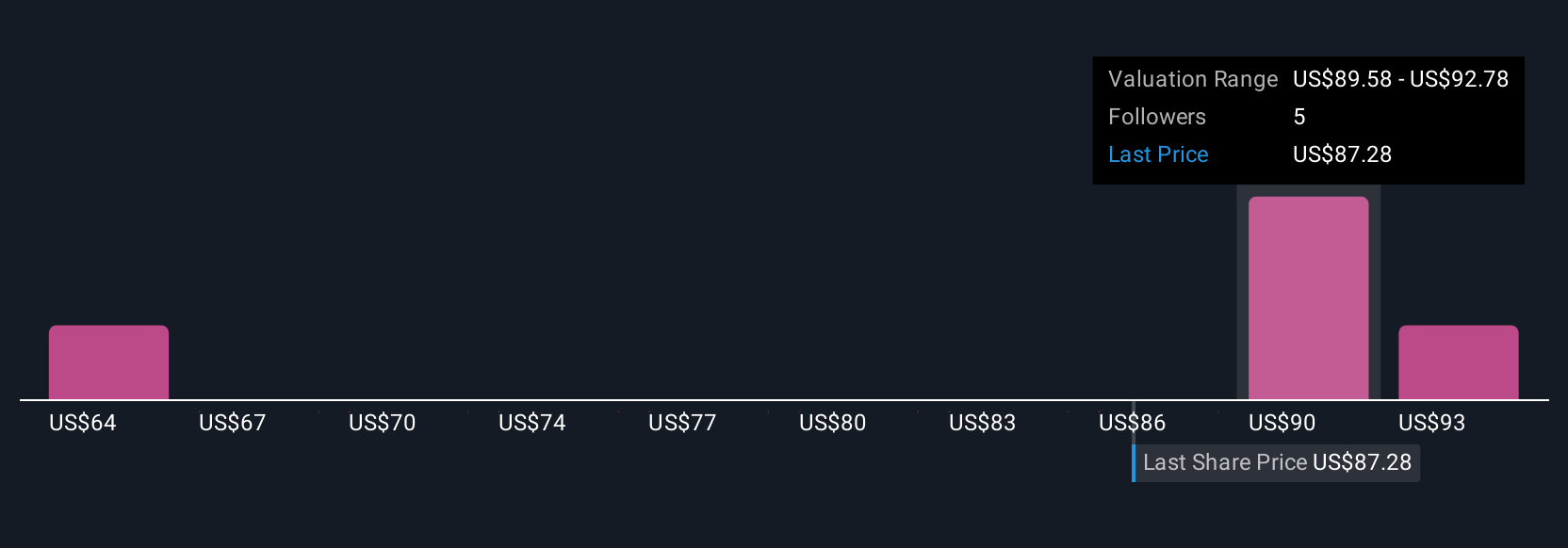

Four Simply Wall St Community members estimated Boyd Gaming’s fair value between US$64.03 and US$111.47. As digital competitors continue to grow, this wide range shows just how differently investors can view Boyd’s future, explore these perspectives to see which aligns with your outlook.

Explore 4 other fair value estimates on Boyd Gaming - why the stock might be worth as much as 29% more than the current price!

Build Your Own Boyd Gaming Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Boyd Gaming research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boyd Gaming research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boyd Gaming's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 25 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boyd Gaming might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BYD

Boyd Gaming

Operates as a multi-jurisdictional gaming company in the United States and Canada.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor