Advertisement

- United States

- /

- Hospitality

- /

- NYSE:ACEL

3 Growth Companies With Insider Ownership Up To 30%

Simply Wall St

Reviewed by Simply Wall St

In a remarkable turn of events, the U.S. stock markets experienced a significant surge, with the Dow Jones climbing 3,000 points and the Nasdaq soaring by 12% following President Trump's announcement of a temporary pause on tariffs. Amidst this backdrop of volatility and opportunity, investors often seek companies with strong growth potential and high insider ownership as these factors can indicate confidence in the company's future prospects.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Super Micro Computer (NasdaqGS:SMCI) | 14.2% | 29.8% |

| Hims & Hers Health (NYSE:HIMS) | 13.3% | 21.8% |

| Duolingo (NasdaqGS:DUOL) | 14.4% | 37.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 12.3% | 64.8% |

| Astera Labs (NasdaqGS:ALAB) | 15.8% | 61.4% |

| Red Cat Holdings (NasdaqCM:RCAT) | 19.4% | 122.6% |

| Niu Technologies (NasdaqGM:NIU) | 36.2% | 82.8% |

| Clene (NasdaqCM:CLNN) | 19.5% | 63.1% |

| Upstart Holdings (NasdaqGS:UPST) | 12.7% | 100.1% |

| Credit Acceptance (NasdaqGS:CACC) | 14.4% | 33.8% |

Let's review some notable picks from our screened stocks.

Sportradar Group (NasdaqGS:SRAD)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sportradar Group AG, along with its subsidiaries, provides sports data services globally including in the United Kingdom, the United States, Malta, and Switzerland, with a market cap of approximately $6.21 billion.

Operations: The company's revenue is primarily derived from its Data Processing segment, which generated approximately €1.11 billion.

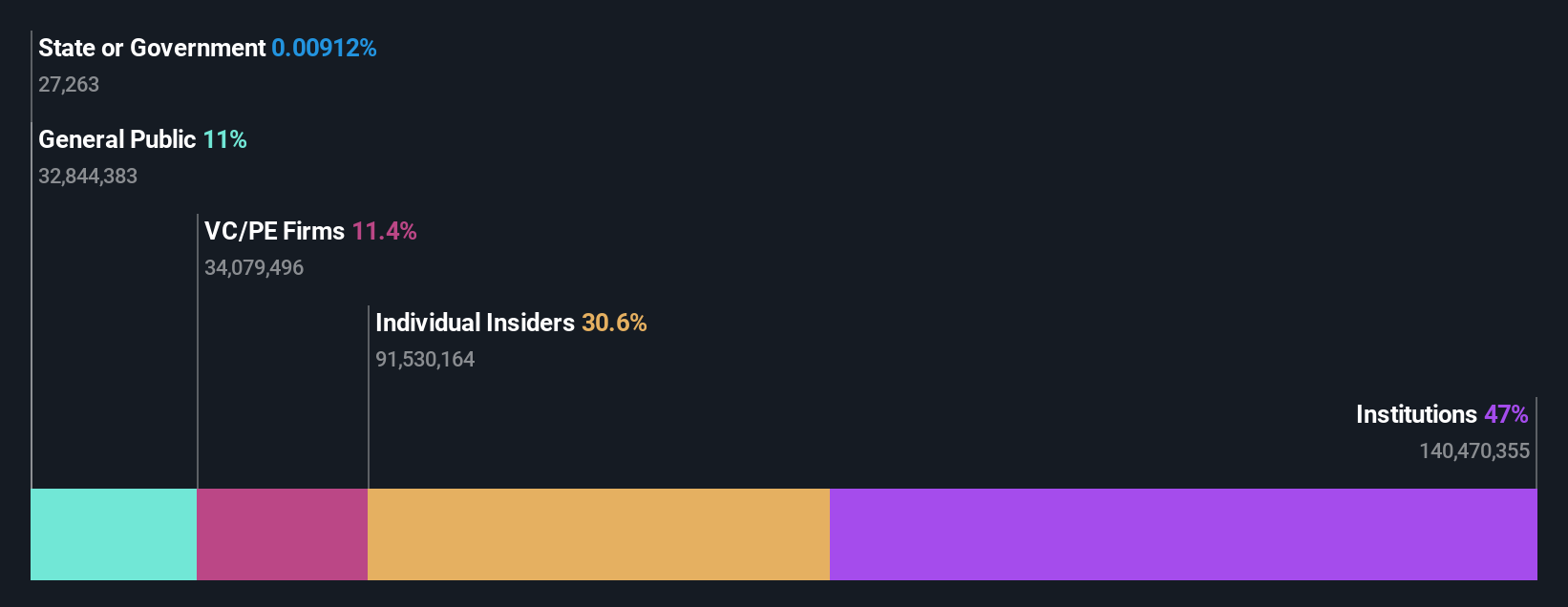

Insider Ownership: 30.6%

Sportradar Group is poised for significant growth, with earnings projected to increase 33.6% annually, outpacing the US market. Despite trading below its fair value estimate, it maintains a strong balance sheet with over $350 million in cash and no debt. The company plans to leverage over $1 billion in available capital for organic investments and strategic acquisitions, such as the pending acquisition of IMG, to enhance margins beyond 30%. Recent revenue guidance anticipates robust growth of at least 15% year-on-year.

- Take a closer look at Sportradar Group's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, Sportradar Group's share price might be too optimistic.

Accel Entertainment (NYSE:ACEL)

Simply Wall St Growth Rating: ★★★★☆☆

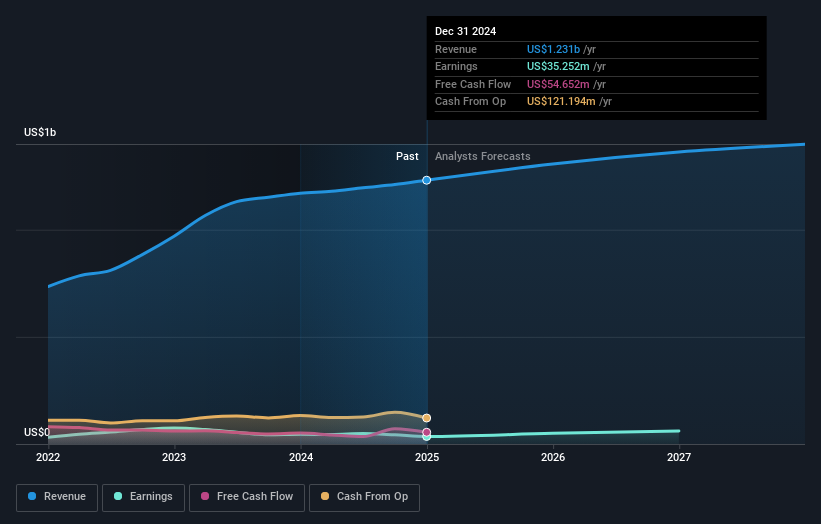

Overview: Accel Entertainment, Inc., along with its subsidiaries, operates as a distributed gaming and local entertainment company in the United States, with a market cap of approximately $853.90 million.

Operations: The company generates revenue from its Casinos & Resorts segment, which amounts to $1.23 billion.

Insider Ownership: 11.1%

Accel Entertainment is positioned for growth with earnings projected to rise 26.91% annually, surpassing the US market average. Despite trading below analyst price targets, its revenue growth of 4.5% per year lags behind the broader market's 8.2%. Recent executive changes, including appointing Scott Levin as Chief Legal Officer, aim to bolster expansion efforts across gaming operations and retail sectors. However, interest payments are not well covered by earnings, indicating potential financial constraints.

- Unlock comprehensive insights into our analysis of Accel Entertainment stock in this growth report.

- According our valuation report, there's an indication that Accel Entertainment's share price might be on the expensive side.

Spotify Technology (NYSE:SPOT)

Simply Wall St Growth Rating: ★★★★★☆

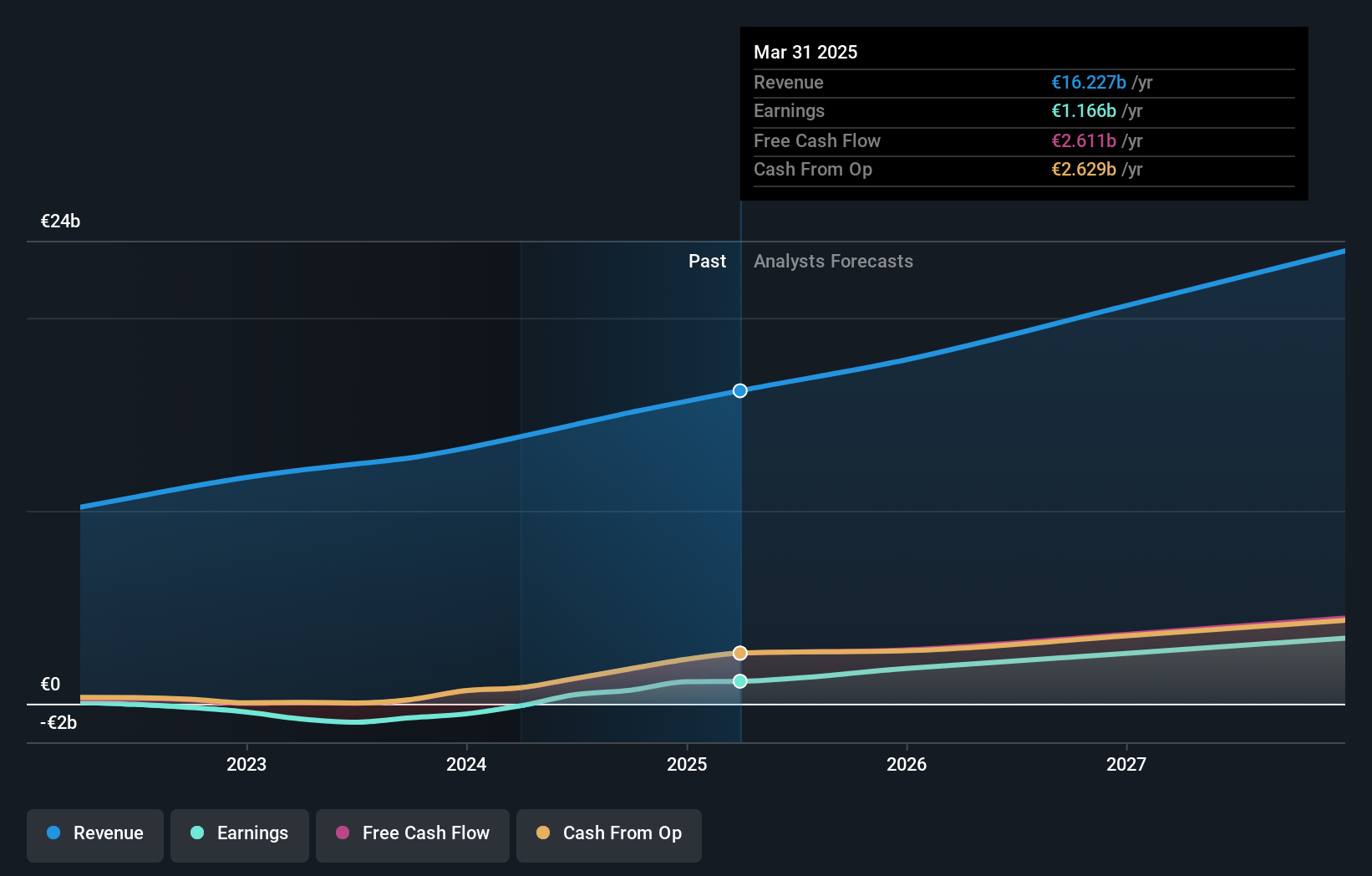

Overview: Spotify Technology S.A., along with its subsidiaries, offers audio streaming subscription services globally and has a market cap of approximately $106.11 billion.

Operations: Spotify's revenue is primarily derived from its Premium segment, generating €13.82 billion, and its Ad-Supported segment, contributing €1.85 billion.

Insider Ownership: 16.2%

Spotify Technology shows potential for growth, with earnings expected to rise 23.7% annually, outpacing the US market's average. Its revenue is forecasted to grow at 12.1% per year, faster than the overall market rate of 8.3%. Recent strategic alliances with Warner Music Group aim to enhance its music ecosystem and artist engagement. Despite trading below estimated fair value, Spotify's profitability and strategic moves position it well within its industry landscape.

- Delve into the full analysis future growth report here for a deeper understanding of Spotify Technology.

- Our valuation report here indicates Spotify Technology may be overvalued.

Turning Ideas Into Actions

- Reveal the 199 hidden gems among our Fast Growing US Companies With High Insider Ownership screener with a single click here.

- Looking For Alternative Opportunities? Rare earth metals are the new gold rush. Find out which 20 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ACEL

Accel Entertainment

Operates as a distributed gaming and local entertainment operator in the United States.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets