Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:WING

What Do Recent Wingstop Price Drops Mean for Its 2025 Valuation?

Simply Wall St

Reviewed by Bailey Pemberton

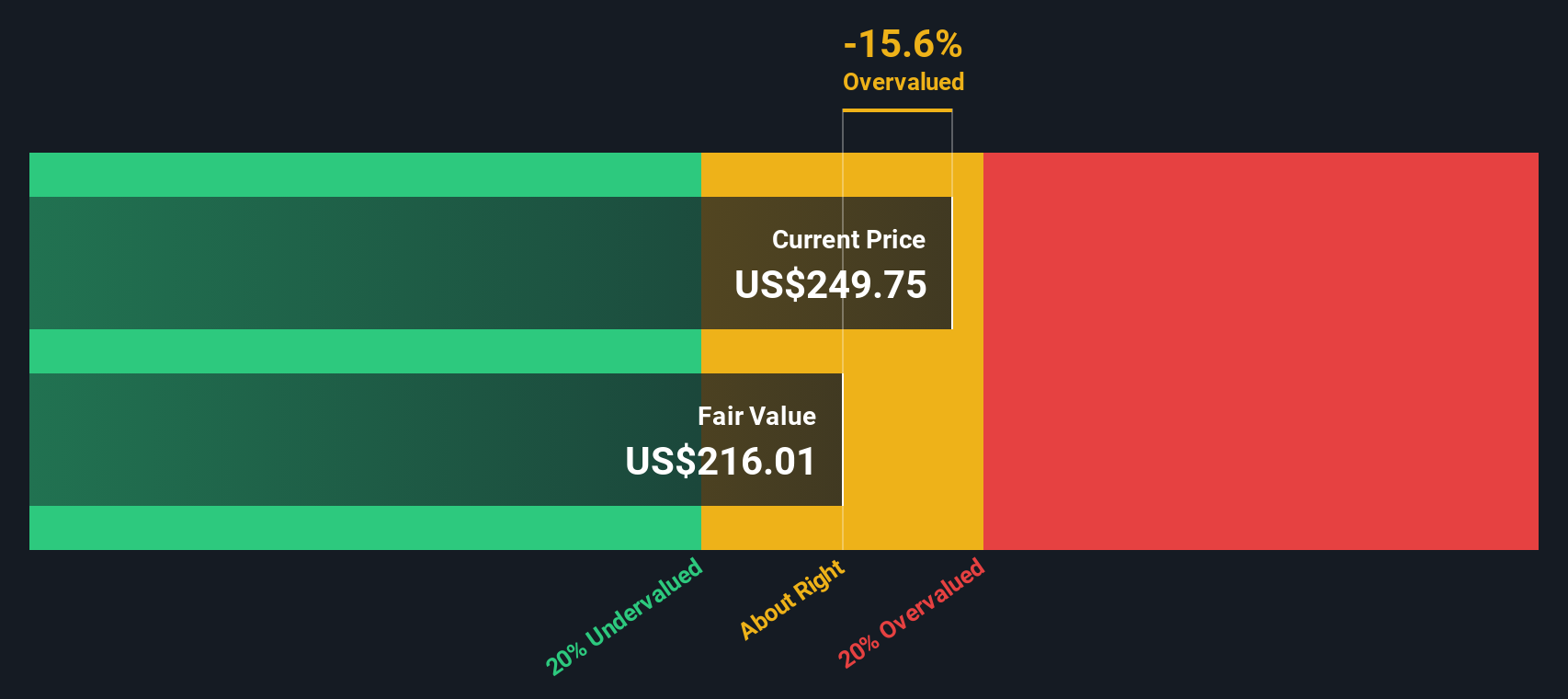

If you’re staring at Wingstop’s latest stock chart and wondering whether this is a dip worth buying or a warning signal to steer clear, you’re not alone. The buzz around Wingstop has ramped up as investors try to figure out if recent turbulence signals a bargain or more trouble ahead. In the past year, Wingstop’s shares have tumbled by 37.9%, including a 14.7% decline year-to-date. These returns raise clear questions about where the value lies now. The last month alone delivered a sharp 18.3% drop, with some traders pointing to changing industry dynamics and broader market volatility as key culprits. Yet, if we zoom out, long-term holders have seen this company soar over 100% in the last three and five years, a reminder of its growth potential even when sentiment shifts suddenly.

With shares closing most recently at $249.01, it’s natural to wonder what makes this price fair or not. Traditional valuation metrics can offer clues: on our scale, Wingstop scores a 1 out of 6 for being undervalued, signaling that by most checks it’s not flashing the “cheap” sign just yet. But the real puzzle is whether these numbers are missing something beneath the surface. Let’s break down the major valuation approaches used by analysts everywhere and stick around, because we’ll be exploring an even sharper way to assess what Wingstop stock is truly worth by the end of the article.

Wingstop scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Wingstop Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a popular valuation approach that estimates a company’s intrinsic value by forecasting its future cash flows, then discounting them back to their present value. In essence, it asks: if you owned all of Wingstop’s future cash earnings today, what would they be worth?

For Wingstop, analysts estimate its latest free cash flow at $56.7 million. These projections point to accelerating growth, with estimates seeing free cash flow climb each year and reaching approximately $292.2 million by 2029. While the first five years of this timeline rely directly on analyst forecasts, longer-term numbers are extrapolated using industry trends and the company’s trajectory. All cash flows are evaluated in U.S. dollars.

After crunching the numbers, the DCF model calculates a fair intrinsic value of $197.07 per share. With the current market price at $249.01, this implies Wingstop shares are trading at a 26.4% premium above what this projection suggests they’re worth. According to this analysis, the stock looks overvalued right now.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Wingstop may be overvalued by 26.4%. Find undervalued stocks or create your own screener to find better value opportunities.

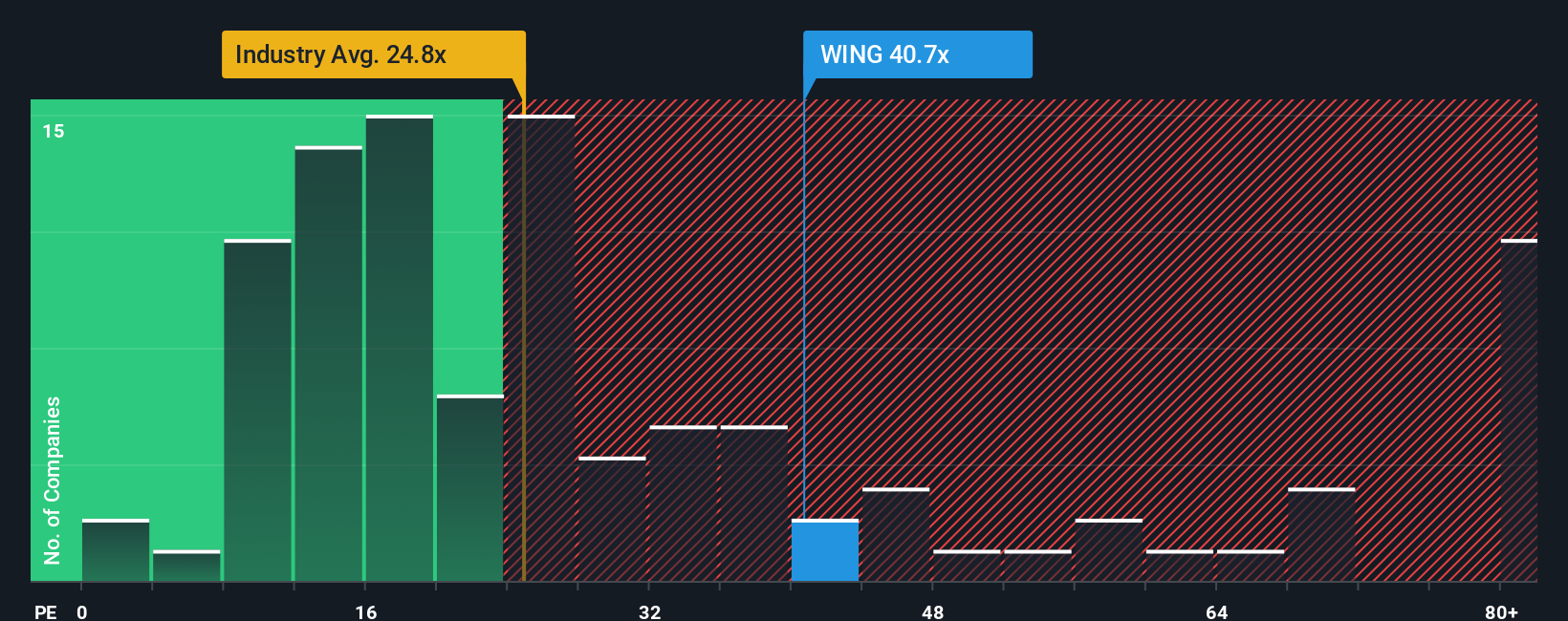

Approach 2: Wingstop Price vs Earnings (P/E Ratio)

For profitable companies like Wingstop, the price-to-earnings (P/E) ratio is a widely used measure of valuation. Because it relates the price of the stock to its actual earnings, it provides an accessible snapshot of how much investors are willing to pay for each dollar of profit. This is a direct way to gauge sentiment about a company’s future prospects.

Growth expectations and risks play a big role in deciding what constitutes a “fair” P/E ratio. Fast-growing companies, or those with a strong competitive position, often deserve a higher P/E because investors anticipate bigger profits ahead. Meanwhile, sectors with cyclicality or other risks tend to trade at lower averages.

Wingstop currently trades at a P/E of 40.5x. For context, this is below the average of its peer group, which stands at 49.4x, but well above the broader hospitality industry average of 24.8x. At first glance, this suggests investors are factoring in above-average growth or resilience compared to most industry players, even if the valuation is not the highest among its closest rivals.

To dig deeper, we use the “Fair Ratio,” which is Simply Wall St’s tailored multiple that considers company-specific factors like Wingstop’s earnings growth forecast, profit margins, overall industry conditions, company size, and inherent risks. Unlike a plain industry average or peer comparison, the Fair Ratio reflects all these nuances to deliver a more precise sense of what is justified for Wingstop right now. For this analysis, the Fair Ratio comes out at 20.1x, substantially lower than both the company’s actual P/E and its peer average.

With Wingstop’s P/E at 40.5x and its Fair Ratio at 20.1x, the stock looks richly valued using this lens. This signals that, even considering growth and risk, the market price is outpacing what would be considered reasonable.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Wingstop Narrative

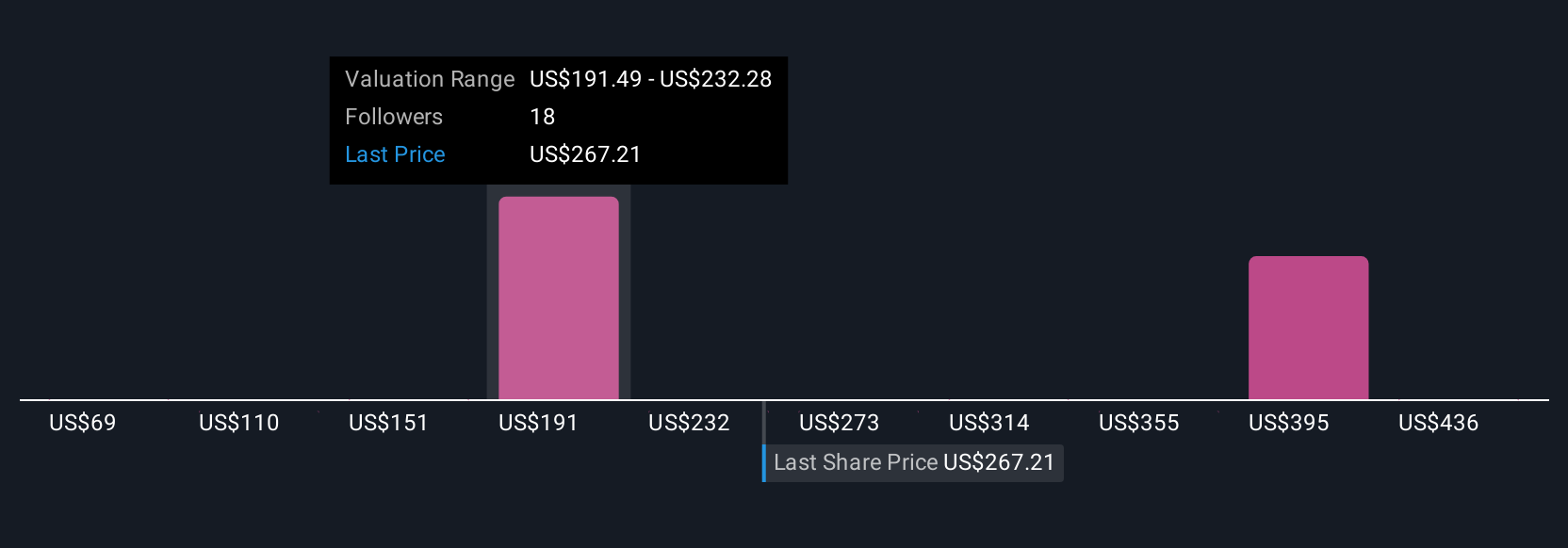

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. In simple terms, a Narrative is your personalized story about a company, your view of how its future will play out, including your estimates for revenue, earnings, and margins, as well as your fair value for the business.

Narratives bridge the gap between stories and numbers by linking your perspective on a company's fundamentals to a fully quantified financial forecast and fair value calculation. This approach takes you beyond basic ratios, giving you a practical tool to capture what you actually believe about a stock’s future and what it’s worth today.

Narratives are easy and accessible for everyone to use on Simply Wall St’s platform, available within the Community page and trusted by millions of investors. You can quickly see whether your view suggests Wingstop is undervalued or overvalued by comparing your calculated Fair Value to the current share price.

Even better, Narratives update automatically whenever new information such as earnings releases or news emerges, so your outlook always stays relevant. For example, the most bullish Narrative on Wingstop estimates a fair value as high as $477, while the most cautious sees it closer to $185, showing just how perspectives can differ depending on each investor’s assumptions and story.

Do you think there's more to the story for Wingstop? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wingstop might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WING

Wingstop

Wingstop Inc., together with its subsidiaries, franchises and operates restaurants under the Wingstop brand in United States, Australia, Bahrain, Kuwait, Puerto Rico, Saudi Arabia, and The Netherlands.

Proven track record with low risk.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1161.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

62 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative