The board of Red Rock Resorts, Inc. (NASDAQ:RRR) has announced that it will pay a dividend on the 29th of September, with investors receiving $0.25 per share. Based on this payment, the dividend yield on the company's stock will be 4.4%, which is an attractive boost to shareholder returns.

See our latest analysis for Red Rock Resorts

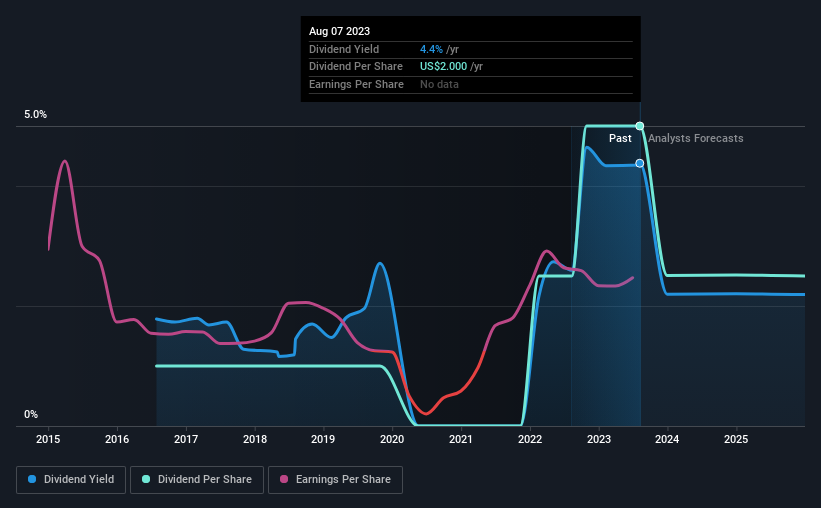

Red Rock Resorts' Earnings Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. Prior to this announcement, Red Rock Resorts' dividend was only 26% of earnings, however it was paying out 395% of free cash flows. The business might be trying to strike a balance between returning cash to shareholders and reinvesting back into the business, but this high of a payout ratio could definitely force the dividend to be cut if the company runs into a bit of a tough spot.

Over the next year, EPS is forecast to fall by 37.8%. If recent patterns in the dividend continue, we could see the payout ratio reaching 94% in the next 12 months, which is on the higher end of the range we would say is sustainable.

Red Rock Resorts' Dividend Has Lacked Consistency

It's comforting to see that Red Rock Resorts has been paying a dividend for a number of years now, however it has been cut at least once in that time. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2016, the dividend has gone from $0.40 total annually to $2.00. This implies that the company grew its distributions at a yearly rate of about 26% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Has Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Red Rock Resorts has seen EPS rising for the last five years, at 8.9% per annum. With a decent amount of growth and a low payout ratio, we think this bodes well for Red Rock Resorts' prospects of growing its dividend payments in the future.

In Summary

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Red Rock Resorts' payments, as there could be some issues with sustaining them into the future. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, Red Rock Resorts has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about. Is Red Rock Resorts not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:RRR

Red Rock Resorts

Through its interest in Station Casinos LLC, develops and operates casino and entertainment properties in the United States.

Very undervalued low.