Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Potbelly Corporation (NASDAQ:PBPB) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Potbelly

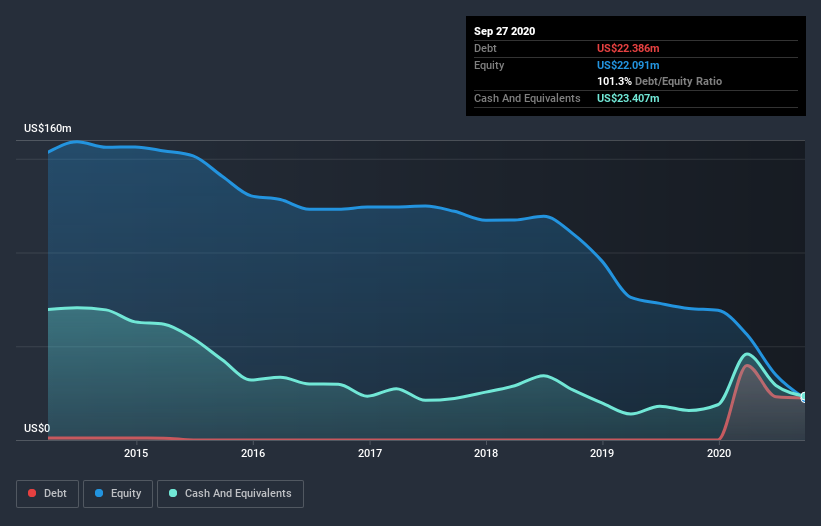

What Is Potbelly's Net Debt?

As you can see below, at the end of September 2020, Potbelly had US$22.4m of debt, up from none a year ago. Click the image for more detail. But on the other hand it also has US$23.4m in cash, leading to a US$1.02m net cash position.

A Look At Potbelly's Liabilities

We can see from the most recent balance sheet that Potbelly had liabilities of US$60.9m falling due within a year, and liabilities of US$223.8m due beyond that. Offsetting these obligations, it had cash of US$23.4m as well as receivables valued at US$4.58m due within 12 months. So it has liabilities totalling US$256.7m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$106.5m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Potbelly would probably need a major re-capitalization if its creditors were to demand repayment. Given that Potbelly has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Potbelly can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Potbelly made a loss at the EBIT level, and saw its revenue drop to US$318m, which is a fall of 22%. That makes us nervous, to say the least.

So How Risky Is Potbelly?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Potbelly lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$13m and booked a US$50m accounting loss. But the saving grace is the US$1.02m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - Potbelly has 3 warning signs (and 1 which is concerning) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you’re looking to trade Potbelly, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:PBPB

Potbelly

Owns, operates, and franchises Potbelly sandwich shops in the United States.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor