Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:EXPE

Does Expedia’s Set-Jetting Hub and New AI Focus Reshape the Bull Case for EXPE?

Simply Wall St

Reviewed by Sasha Jovanovic

- In early December 2025, Expedia Group launched its Unpack ’26 Set-Jetting travel hub, a curated, shoppable platform linking blockbuster-inspired destinations with hotels, activities, and flights as screen-based travel planning gains traction among younger travelers.

- By turning “watchlist wanderlust” into bookable itineraries and tying in perks like VIP Access properties, Expedia is sharpening its appeal to Gen Z and Millennial customers who increasingly choose trips based on what they watch.

- Now we’ll examine how Expedia’s Set-Jetting travel hub and AI leadership appointment could influence its existing investment narrative and outlook.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Expedia Group Investment Narrative Recap

To own Expedia Group, you need to believe its unified platform, data capabilities, and brand portfolio can convert rising digital travel demand into durable earnings, despite intense competition and U.S. consumer uncertainty. The Set Jetting travel hub and new AI leadership look directionally supportive of conversion and engagement, but they do not materially change the near term dependence on U.S. B2C health as the key catalyst, or the risk that competition and traffic costs could still pressure margins.

The appointment of Xavier Amatriain as Expedia’s first chief artificial intelligence and data officer is particularly relevant here, because it speaks directly to one of the main potential catalysts: using AI to sharpen personalization, improve search outcomes, and strengthen marketing efficiency across brands like Expedia, Hotels.com, and Vrbo. How effectively this AI push offsets rising acquisition costs and alternative travel platforms will be central to the stock’s ongoing investment case.

However, investors also need to be aware that growing reliance on external traffic partners could still...

Read the full narrative on Expedia Group (it's free!)

Expedia Group's narrative projects $16.9 billion revenue and $2.1 billion earnings by 2028. This requires 6.4% yearly revenue growth and about a $1.0 billion earnings increase from $1.1 billion today.

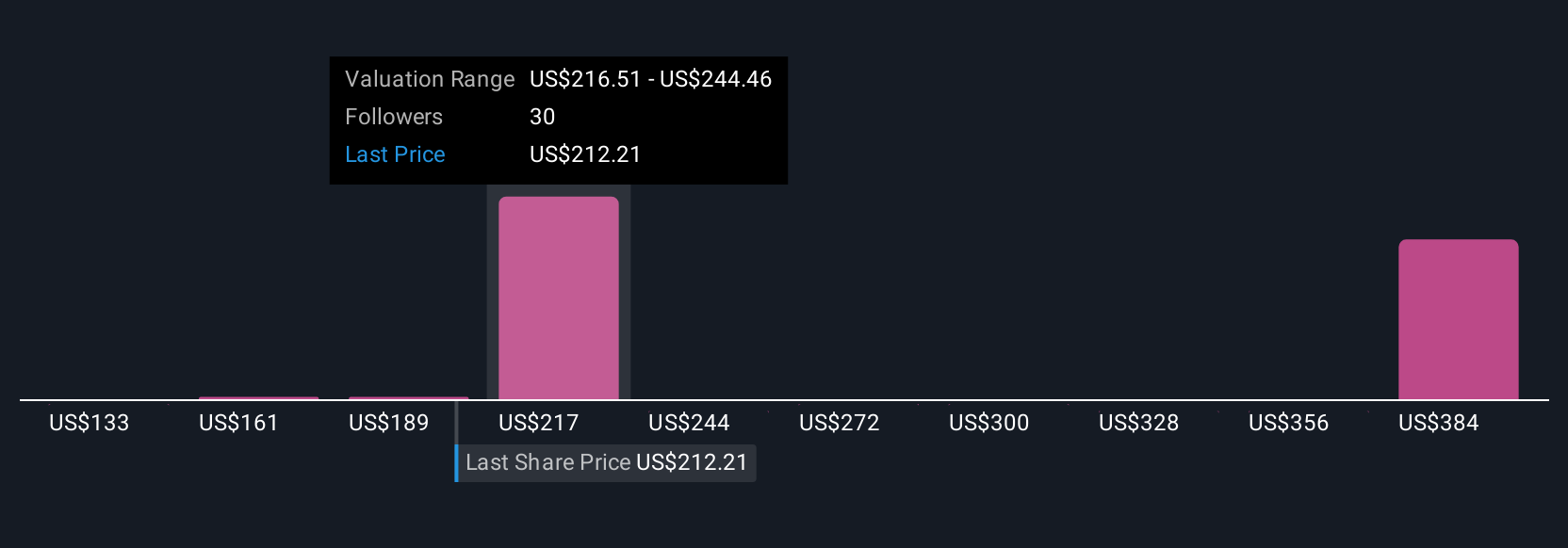

Uncover how Expedia Group's forecasts yield a $269.79 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Nine fair value estimates from the Simply Wall St Community span roughly US$133 to US$520 per share, underscoring how differently people are modeling Expedia’s future. When you weigh those views against the risk that external traffic dependence and evolving search behavior could pressure acquisition costs, it becomes even more important to compare several perspectives before forming a view on Expedia’s long term performance.

Explore 9 other fair value estimates on Expedia Group - why the stock might be worth over 2x more than the current price!

Build Your Own Expedia Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Expedia Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Expedia Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Expedia Group's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Expedia Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:EXPE

Expedia Group

Operates as an online travel company in the United States and internationally.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

44 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Trending Discussion

US

User on IMPACT Silver ·

I had this as very easy 10 bagger. But hey, your case makes sense. Thanks!

1

|1