Advertisement

- United States

- /

- Consumer Services

- /

- NasdaqGS:DUOL

3 US Stocks That May Be Trading Below Their Estimated Value In September 2024

Simply Wall St

Reviewed by Simply Wall St

As the U.S. stock market reacts to the Federal Reserve's recent rate cut decision, major indices have experienced fluctuations, reflecting investor uncertainty. This environment can create opportunities for discerning investors to identify stocks that may be trading below their estimated value. In such a volatile market, a good stock is often characterized by strong fundamentals, resilient earnings potential, and favorable industry positioning. Here are three U.S. stocks that may be trading below their estimated value in September 2024.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Western Alliance Bancorporation (NYSE:WAL) | $84.85 | $168.28 | 49.6% |

| Heartland Financial USA (NasdaqGS:HTLF) | $56.94 | $112.77 | 49.5% |

| EQT (NYSE:EQT) | $33.53 | $65.86 | 49.1% |

| California Resources (NYSE:CRC) | $52.31 | $104.32 | 49.9% |

| Trustmark (NasdaqGS:TRMK) | $32.75 | $64.82 | 49.5% |

| Progress Software (NasdaqGS:PRGS) | $57.52 | $114.90 | 49.9% |

| ChromaDex (NasdaqCM:CDXC) | $3.55 | $7.10 | 50% |

| American Superconductor (NasdaqGS:AMSC) | $20.725 | $40.71 | 49.1% |

| TransMedics Group (NasdaqGM:TMDX) | $155.96 | $305.23 | 48.9% |

| Carter Bankshares (NasdaqGS:CARE) | $17.75 | $35.20 | 49.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

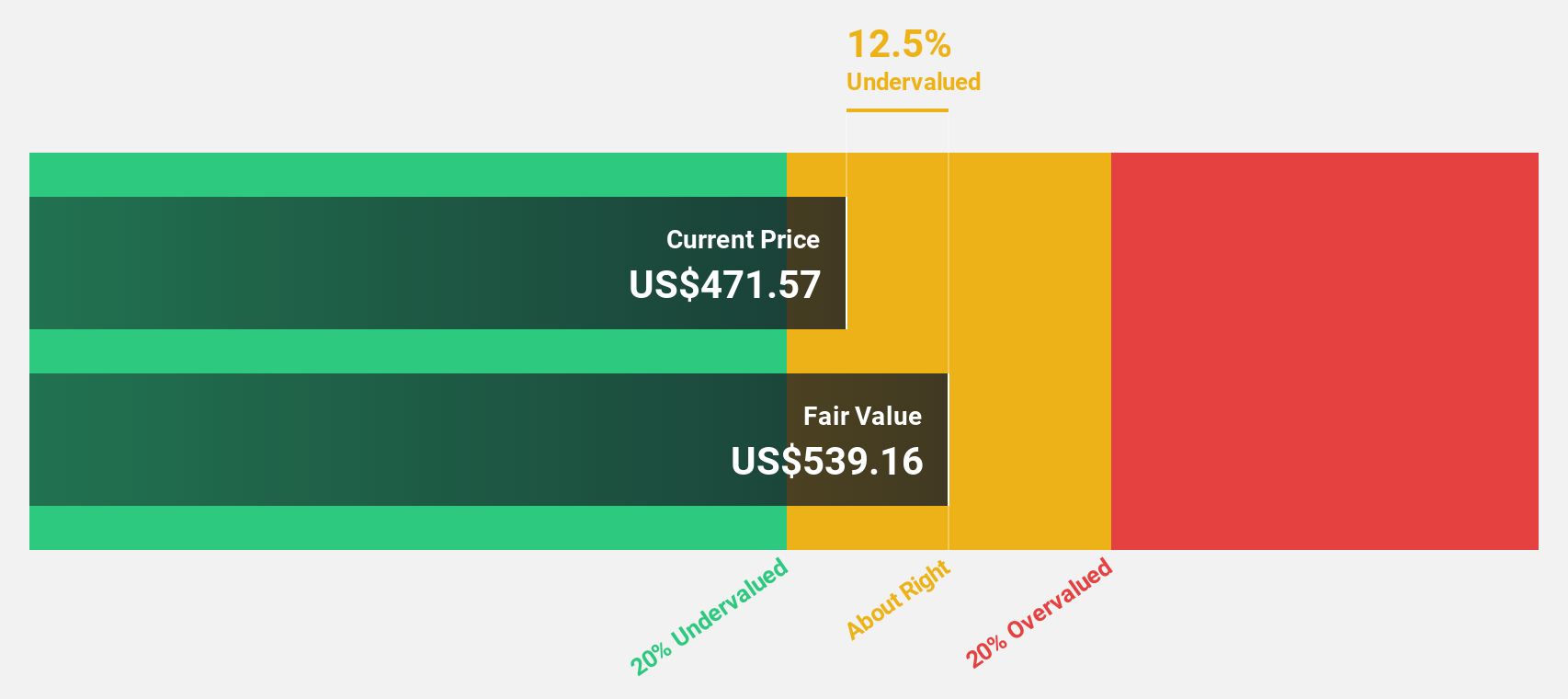

Duolingo (NasdaqGS:DUOL)

Overview: Duolingo, Inc. operates as a mobile learning platform in the United States, the United Kingdom, and internationally with a market cap of $10.56 billion (NasdaqGS:DUOL).

Operations: The company's revenue from educational software is $634.49 million.

Estimated Discount To Fair Value: 46.5%

Duolingo's recent earnings report shows strong financial performance with Q2 sales of US$178.33 million and net income of US$24.35 million, reflecting significant year-over-year growth. The company is trading at 46.5% below its estimated fair value and is highly undervalued based on discounted cash flow analysis (DCF). With expected annual revenue growth of 24.4% and earnings forecasted to grow significantly over the next three years, Duolingo presents a compelling case for being undervalued based on cash flows.

- Upon reviewing our latest growth report, Duolingo's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Duolingo.

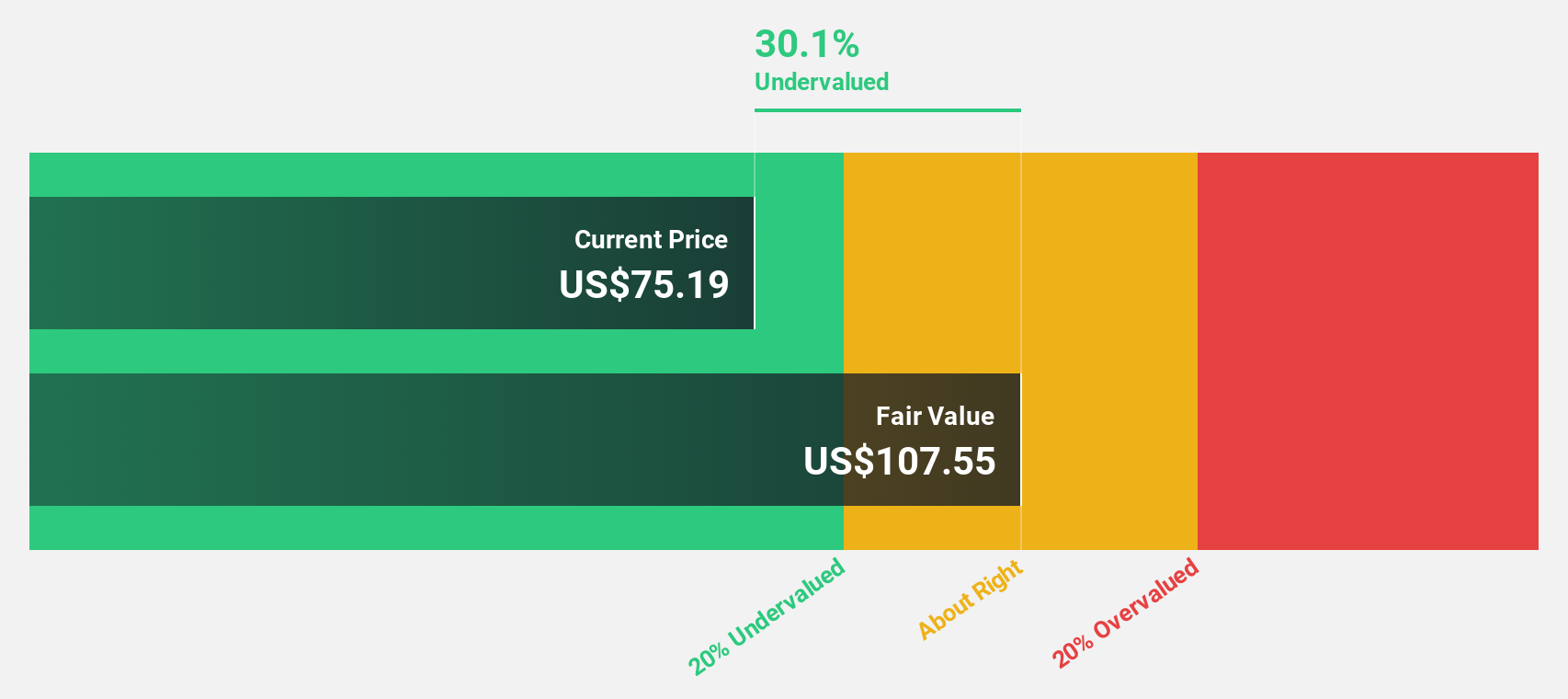

Estée Lauder Companies (NYSE:EL)

Overview: The Estée Lauder Companies Inc. manufactures, markets, and sells skin care, makeup, fragrance, and hair care products worldwide with a market cap of approximately $31.60 billion.

Operations: The company's revenue segments include skin care ($7.91 billion), makeup ($4.47 billion), fragrance ($2.49 billion), and hair care ($629 million).

Estimated Discount To Fair Value: 25%

Estée Lauder Companies, trading at US$88, is 25% below its estimated fair value of US$117.37 based on discounted cash flow analysis. Despite high debt levels and a dividend not well covered by earnings, the company's forecasted annual profit growth of 27.75% outpaces the US market average. Recent financials show decreased net income due to significant impairments, but future earnings are expected to grow significantly over the next three years.

- Insights from our recent growth report point to a promising forecast for Estée Lauder Companies' business outlook.

- Dive into the specifics of Estée Lauder Companies here with our thorough financial health report.

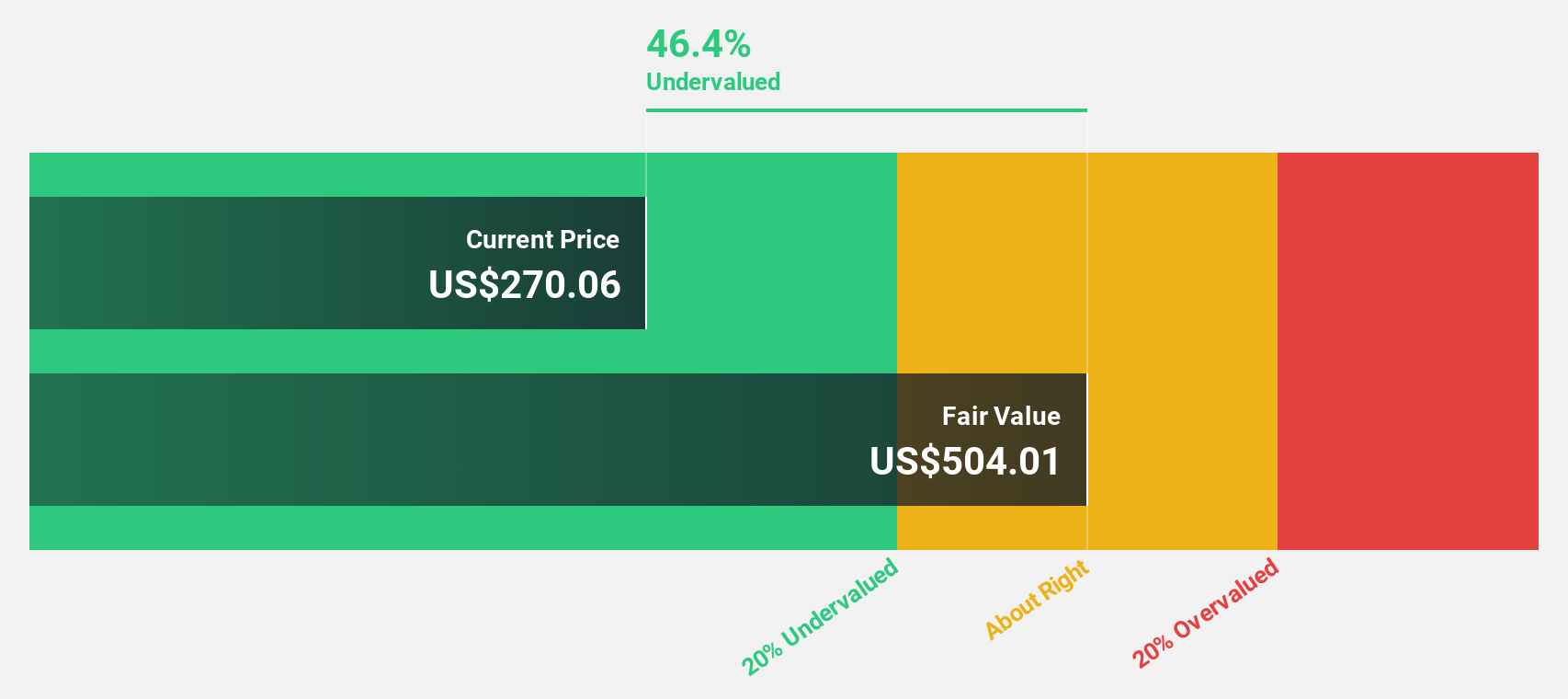

Flutter Entertainment (NYSE:FLUT)

Overview: Flutter Entertainment plc is a global sports betting and gaming company with operations in the United Kingdom, Ireland, Australia, the United States, Italy, and other international markets, boasting a market cap of $40.98 billion.

Operations: The company's revenue segments include $5.25 billion from the US, $3.31 billion from the UK and Ireland, $1.39 billion from Australia, and $2.93 billion from international markets.

Estimated Discount To Fair Value: 21.1%

Flutter Entertainment, trading at US$229.05, is 21.1% below its estimated fair value of US$290.36 based on discounted cash flow analysis. The company is forecast to become profitable within three years and expects annual revenue growth of 11.2%, outpacing the US market average of 8.7%. Recent discussions about acquiring Snaitech S.p.A., alongside a strong Q2 performance with net income rising to $297 million, underscore its potential for sustained growth driven by the US market's success with FanDuel.

- Our comprehensive growth report raises the possibility that Flutter Entertainment is poised for substantial financial growth.

- Click here to discover the nuances of Flutter Entertainment with our detailed financial health report.

Make It Happen

- Dive into all 192 of the Undervalued US Stocks Based On Cash Flows we have identified here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DUOL

Duolingo

Operates as a mobile learning platform in the United States, the United Kingdom, and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.3% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.6% undervalued

MA

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor