- United States

- /

- Hospitality

- /

- NasdaqGS:DNUT

Krispy Kreme (NASDAQ:DNUT) Has Announced A Dividend Of $0.035

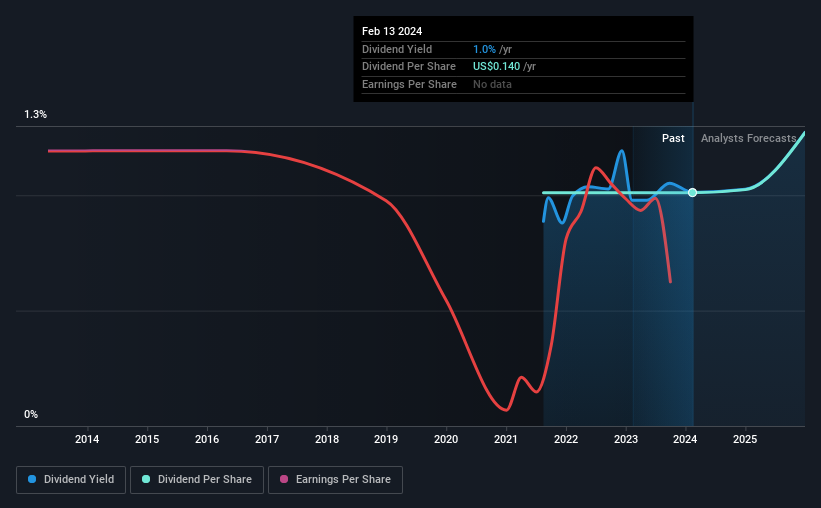

Krispy Kreme, Inc. (NASDAQ:DNUT) has announced that it will pay a dividend of $0.035 per share on the 8th of May. The dividend yield is 1.0% based on this payment, which is a little bit low compared to the other companies in the industry.

View our latest analysis for Krispy Kreme

Krispy Kreme's Payment Has Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. Even though Krispy Kreme is not generating a profit, it is still paying a dividend. Along with this, it is also not generating free cash flows, which raises concerns about the sustainability of the dividend.

According to analysts, EPS should be several times higher next year. If the dividend continues along recent trends, we estimate the payout ratio will be 6.6%, so there isn't too much pressure on the dividend.

Krispy Kreme Doesn't Have A Long Payment History

Looking back, the dividend has been stable, but the company hasn't been paying a dividend for very long so we can't be confident that the dividend will remain stable through all economic environments. The last annual payment of $0.14 was flat on the annual payment from2 years ago. Modest dividend growth is good to see, especially with the payments being relatively stable. However, the payment history is relatively short and we wouldn't want to rely on this dividend too much.

The Company Could Face Some Challenges Growing The Dividend

Investors could be attracted to the stock based on the quality of its payment history. Krispy Kreme has impressed us by growing EPS at 19% per year over the past five years. Even though the company isn't making a profit, strong earnings growth could turn that around in the near future. As long as the company becomes profitable soon, it is on a trajectory that could see it being a solid dividend payer.

Krispy Kreme's Dividend Doesn't Look Sustainable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. In general, the distributions are a little bit higher than we would like, but we can't ignore the fact the quickly growing earnings gives this stock great potential in the future. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 10 Krispy Kreme analysts we track are forecasting continued growth with our free report on analyst estimates for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Krispy Kreme might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:DNUT

Krispy Kreme

Produces doughnuts in the United States, the United Kingdom, Ireland, Australia, New Zealand, Mexico, Canada, Japan, and internationally.

Slight and fair value.