Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:DKNG

DraftKings (DKNG): Examining Valuation After Recent Volatility and Momentum in the Stock

Reviewed by Simply Wall St

If you have been tracking DraftKings (DKNG), you may have noticed the stock’s recent movement and are likely wondering what is next. While there is no clear event driving the action right now, the current volatility still raises interesting questions for anyone considering a position. Sometimes, it is moves without direct catalysts that signal shifts in market sentiment or present valuation mismatches worth a closer look.

Looking at the bigger picture, DraftKings has seen its share price climb roughly 28% over the past year, with gains accelerating in the past 3 months. Short-term momentum appears to be building again after a modest pullback last week. These swings come amid ongoing revenue growth and, notably, a substantial improvement in net income. These factors continue to shape expectations for the company’s path toward profitability.

So, after a year of sharp gains and a strong fundamental backdrop, is DraftKings trading at a discount to fair value, or is the market already pricing in the next wave of growth?

Most Popular Narrative: 15.6% Undervalued

According to the most widely followed narrative, DraftKings is currently trading at a discount to its intrinsic value, with a fair value estimate higher than the prevailing market price. This suggests that analysts see fundamental upside not yet reflected in the current share price.

DraftKings' proprietary technology, enhanced by the acquisition of Simplebet and in-house developments, is enabling unique betting formats and vertical integration. This is expected to support higher gross margins and strengthen competitive positioning, positively impacting long-term earnings and operating leverage.

Curious what helps DraftKings stand apart in the rapidly evolving world of online betting? Underneath this valuation lies a powerful bet on future growth, expanding margins, and strategic tech moves that could shake up the industry. Want to know which financial assumptions are driving these bullish targets? The details may surprise you. Discover what’s fueling this enthusiastic outlook.

Result: Fair Value of $54.86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, DraftKings faces mounting regulatory risk and rising state-level tax policies. These factors could challenge the optimistic outlook if conditions worsen.

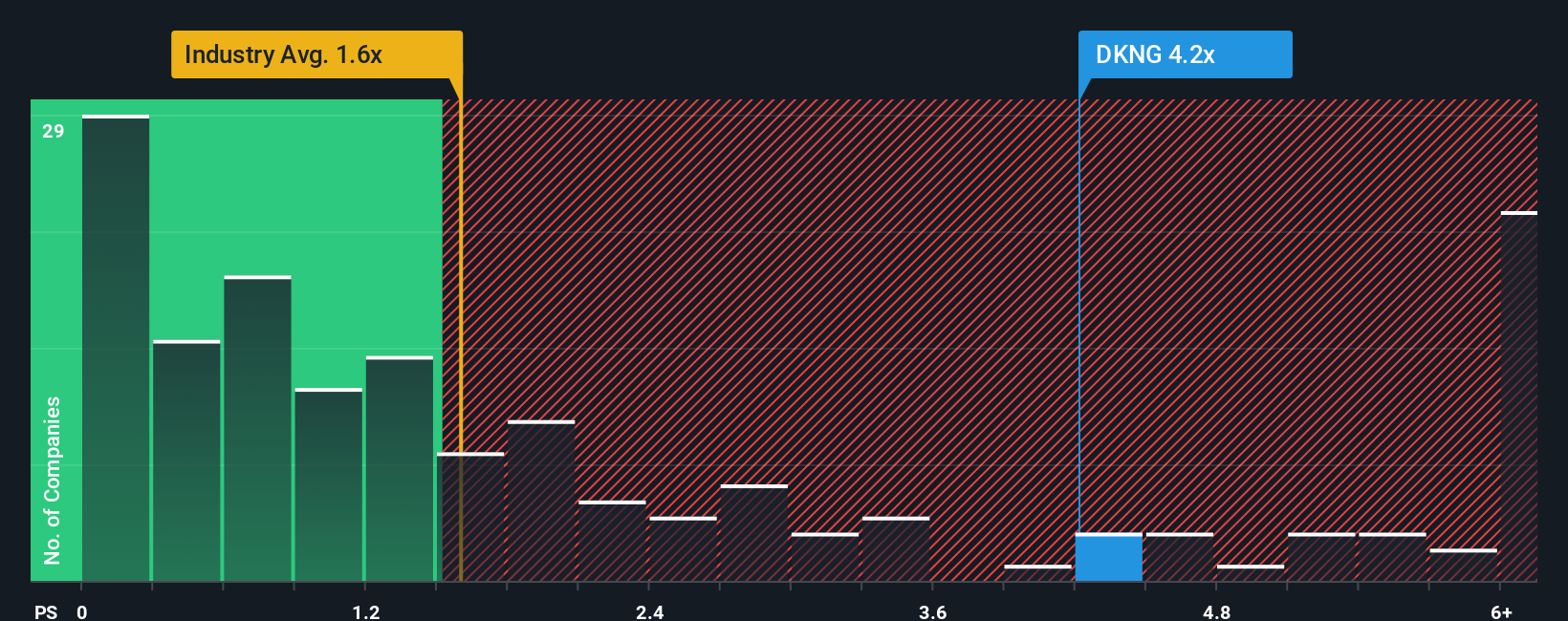

Find out about the key risks to this DraftKings narrative.Another View: Looking at the Market Multiple

While some see DraftKings as undervalued based on future cash flows, comparing its price-to-sales against the industry average suggests the opposite. Could market enthusiasm be pushing shares ahead of what fundamentals support?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own DraftKings Narrative

If you see things differently or want to dive into your own research, it is quick and easy to build your own valuation story. Do it your way

A great starting point for your DraftKings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for Your Next Winning Stock?

Why limit your portfolio to just one contender? Use the Simply Wall Street Screener to uncover standout stocks and fresh opportunities that fit your unique investment strategy.

- Tap into untapped growth by checking out penny stocks with strong financials through penny stocks with strong financials, and spot companies often overlooked by the market.

- Supercharge your watchlist with the latest AI breakthroughs by searching for AI penny stocks, and get ahead in the fast-evolving world of artificial intelligence.

- Secure greater value for your money by finding undervalued stocks based on cash flows using fundamental analysis to highlight promising investments that may be trading below their true worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:DKNG

DraftKings

Operates as a digital sports entertainment and gaming company in the United States and internationally.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

158 followersusers have followed this narrative

0 commentsusers have commented on this narrative

27 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

CH

ChuckN on NextEra Energy ·

Investor Thesis: Why the NextEra Energy / Dominion Energy Merger Could Be a Major AI Power Infrastructure Event

Fair Value:US$93.719.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.1% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PA

pablo_ on Kodiak AI ·

Kodiak AI: The Tech Already Works — The Race Is Against Cash Burn

Fair Value:US$6.4630.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

281 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

166 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0