- United States

- /

- Hospitality

- /

- NasdaqGS:DASH

NYC Tipping Lawsuit Might Change The Case For Investing In DoorDash (DASH)

Reviewed by Sasha Jovanovic

- In recent days, DoorDash and Uber filed a lawsuit against New York City challenging new rules that require food-delivery apps to display a default minimum 10% tip at checkout, arguing the law infringes on their constitutional rights and harms their business model.

- This legal fight highlights how changes to tipping rules in a key market could influence DoorDash’s cost structure, customer behavior, and long-term operating flexibility.

- We’ll now examine how this legal pushback against New York’s mandatory default tipping rules may alter DoorDash’s investment narrative and risk profile.

Find companies with promising cash flow potential yet trading below their fair value.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe its broad delivery platform and subscription ecosystem can keep scaling, even as regulations and competition evolve. The New York default tipping lawsuit and the recent driver product‑tampering case both underline near term risk around trust and regulation, but neither appears to fundamentally change the current key catalyst: execution in new verticals and markets. The biggest risk remains that rising complexity and regulatory pressure push up costs faster than revenue.

In this context, DoorDash’s expanding partnerships, such as the Amazon same day grocery competition shock and the new Woolworths Australia grocery deal, matter more to the story than this isolated driver incident. These moves tie directly into the main catalyst for the stock right now: whether DoorDash can extend its reach in grocery and everyday retail while protecting margins against higher labor, compliance and fulfillment expenses.

Yet even as these growth moves attract attention, investors should be aware that rising labor and regulatory costs could...

Read the full narrative on DoorDash (it's free!)

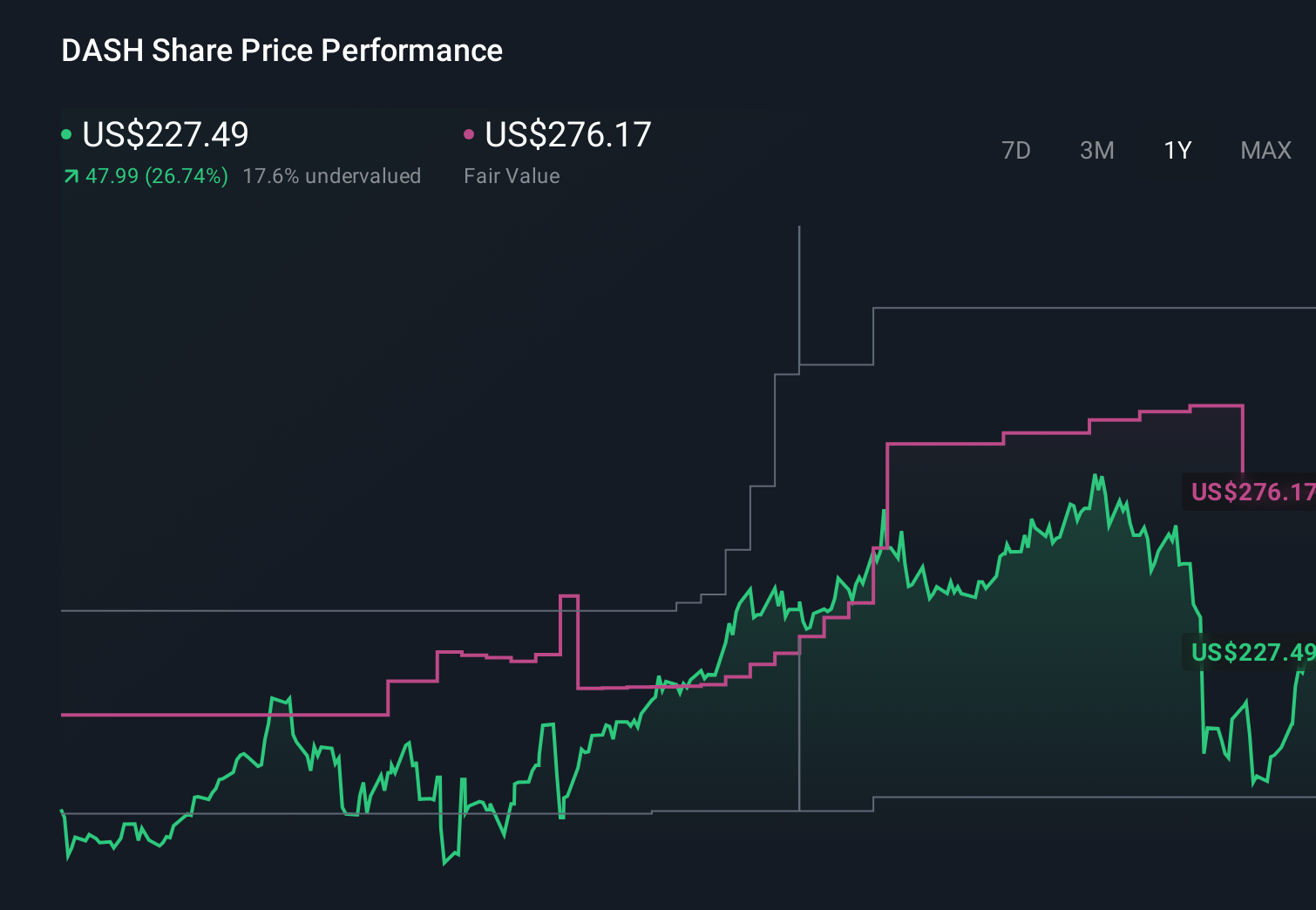

DoorDash's narrative projects $20.4 billion revenue and $3.2 billion earnings by 2028. This requires 19.6% yearly revenue growth and an earnings increase of about $2.4 billion from $781.0 million today.

Uncover how DoorDash's forecasts yield a $276.41 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Twelve Simply Wall St Community fair value estimates for DoorDash span roughly US$194 to US$357 per share, showing wide disagreement on upside. Against that backdrop, the risk that higher labor and regulatory costs squeeze margins is a key lens for thinking about how the business might perform and why it is worth comparing several viewpoints before acting.

Explore 12 other fair value estimates on DoorDash - why the stock might be worth 14% less than the current price!

Build Your Own DoorDash Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DASH

DoorDash

Operates a commerce platform that connects merchants, consumers, and independent contractors in the United States and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)