Advertisement

- United States

- /

- Consumer Services

- /

- NasdaqCM:CLEU

China Liberal Education Holdings' (NASDAQ:CLEU) Robust Earnings Might Be Weaker Than You Think

China Liberal Education Holdings Limited (NASDAQ:CLEU) posted some decent earnings, but shareholders didn't react strongly. We think that they might be concerned about some underlying details that our analysis found.

See our latest analysis for China Liberal Education Holdings

Zooming In On China Liberal Education Holdings' Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

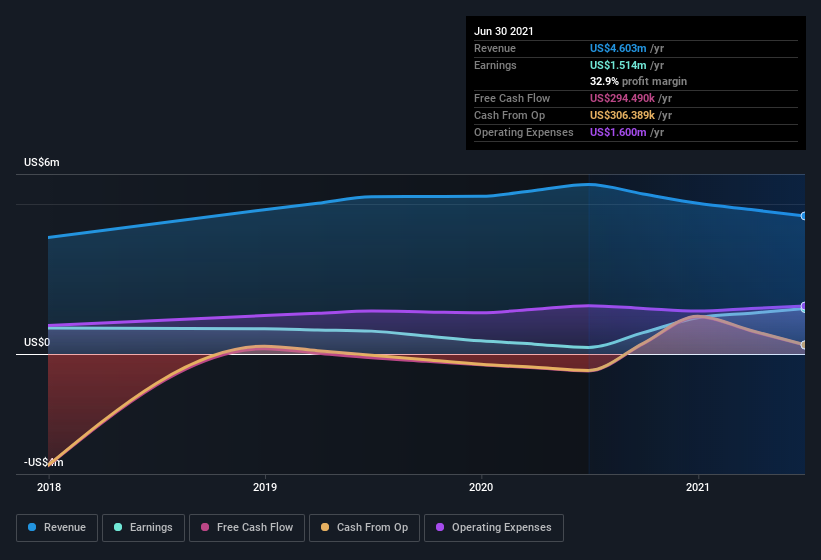

Over the twelve months to June 2021, China Liberal Education Holdings recorded an accrual ratio of 0.22. Unfortunately, that means its free cash flow fell significantly short of its reported profits. In fact, it had free cash flow of US$294k in the last year, which was a lot less than its statutory profit of US$1.51m. Given that China Liberal Education Holdings had negative free cash flow in the prior corresponding period, the trailing twelve month resul of US$294k would seem to be a step in the right direction. Unfortunately for shareholders, the company has also been issuing new shares, diluting their share of future earnings.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of China Liberal Education Holdings.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, China Liberal Education Holdings increased the number of shares on issue by 95% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out China Liberal Education Holdings' historical EPS growth by clicking on this link.

How Is Dilution Impacting China Liberal Education Holdings' Earnings Per Share? (EPS)

As you can see above, China Liberal Education Holdings has been growing its net income over the last few years, with an annualized gain of 77% over three years. But EPS was only up 17% per year, in the exact same period. And the 591% profit boost in the last year certainly seems impressive at first glance. On the other hand, earnings per share are only up 374% in that time. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

In the long term, earnings per share growth should beget share price growth. So China Liberal Education Holdings shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On China Liberal Education Holdings' Profit Performance

As it turns out, China Liberal Education Holdings couldn't match its profit with cashflow and its dilution means that earnings per share growth is lagging net income growth. Considering all this we'd argue China Liberal Education Holdings' profits probably give an overly generous impression of its sustainable level of profitability. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. To that end, you should learn about the 5 warning signs we've spotted with China Liberal Education Holdings (including 2 which are a bit concerning).

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:CLEU

China Liberal Education Holdings

Provides educational services and products under the China Liberal brand name in the People’s Republic of China.

Medium-low with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor