- United States

- /

- Food and Staples Retail

- /

- NYSE:TGT

Target (NYSE:TGT) Expands Third-Party Marketplace With ButcherBox Offerings Starting At US$99

Reviewed by Simply Wall St

Recently, ButcherBox launched its products on Target Plus, expanding its market reach without requiring subscriptions. This strategic move could potentially enhance Target's (NYSE:TGT) digital marketplace offerings. However, Target's share price decreased by 8% last week, amidst broader market selloffs where the Dow dropped 4%. The company's partnership with ButcherBox may have provided some balance but didn't prevent the decline. The volatility in major indices, influenced by broader market pressures such as tech sector declines, likely overshadowed any positive impacts from recent partnerships and strategic initiatives.

We've spotted 2 warning signs for Target you should be aware of.

Find companies with promising cash flow potential yet trading below their fair value.

Target's recent collaboration with ButcherBox aims to expand its marketplace reach, potentially impacting its digital sales and overall revenue. The move comes as the company focuses on enhancing customer experience through digital channels, in-store improvements, and loyalty programs. These initiatives align with its long-term growth objectives, although the recent strategic news has yet to significantly alter market sentiments, indicated by the share price decline amidst broader market challenges.

Over the past five years, including dividends, Target's total shareholder return was a modest 3.52%. In comparison, over the previous year, the company notably underperformed both the US Consumer Retailing industry, which returned 26.2%, and the broader US market, which gained 4.7%. Such performance metrics highlight challenges Target faces amidst shifting consumer preferences and market conditions.

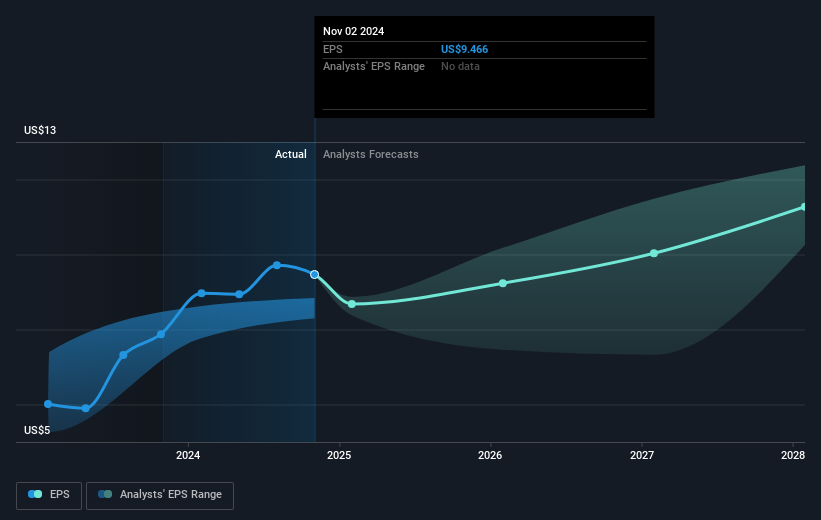

The recent partnership might influence analysts' revenue and earnings forecasts, considering Target's aim to drive growth through online marketplaces and customer-centric improvements. Analysts project annual revenue growth of 2.3% over the next three years, with earnings potentially reaching US$4.6 billion by 2028. Nevertheless, the current share price of US$88.76 reflects a 33.7% discount to the consensus price target of approximately US$133.97, signaling room for potential valuation alignment if growth materializes as forecasted.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Target, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Target might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TGT

Very undervalued established dividend payer.

Similar Companies

Market Insights

Community Narratives