- United States

- /

- Food and Staples Retail

- /

- NYSE:KR

Has the Albertsons Merger Scrutiny Created an Opportunity in Kroger Stock?

Reviewed by Bailey Pemberton

- Wondering if Kroger at around $63 a share is still a smart buy or if the easy money has already been made? This breakdown is designed to give you a clear, valuation first answer.

- The stock is up 0.8% over the last week and 2.0% year to date, but that sits against a modest 3.9% gain over 1 year and much stronger returns of 52.4% over 3 years and 127.7% over 5 years, hinting at a long term uptrend that has cooled recently.

- Recent headlines have centered on Kroger's ongoing antitrust scrutiny around its proposed merger with Albertsons and regulatory pushback from the FTC. Together these issues have kept risk perceptions elevated and the share price choppy. At the same time, coverage has highlighted how a larger combined footprint could strengthen Kroger's buying power and loyalty ecosystem if the deal clears, which is part of what the market is trying to price in.

- Kroger currently scores 2 out of 6 on our undervaluation checks, so we will walk through what the main valuation models say about that score, and then finish by looking at a more holistic way to judge whether the stock is genuinely good value or just statistically cheap.

Kroger scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Kroger Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to the present.

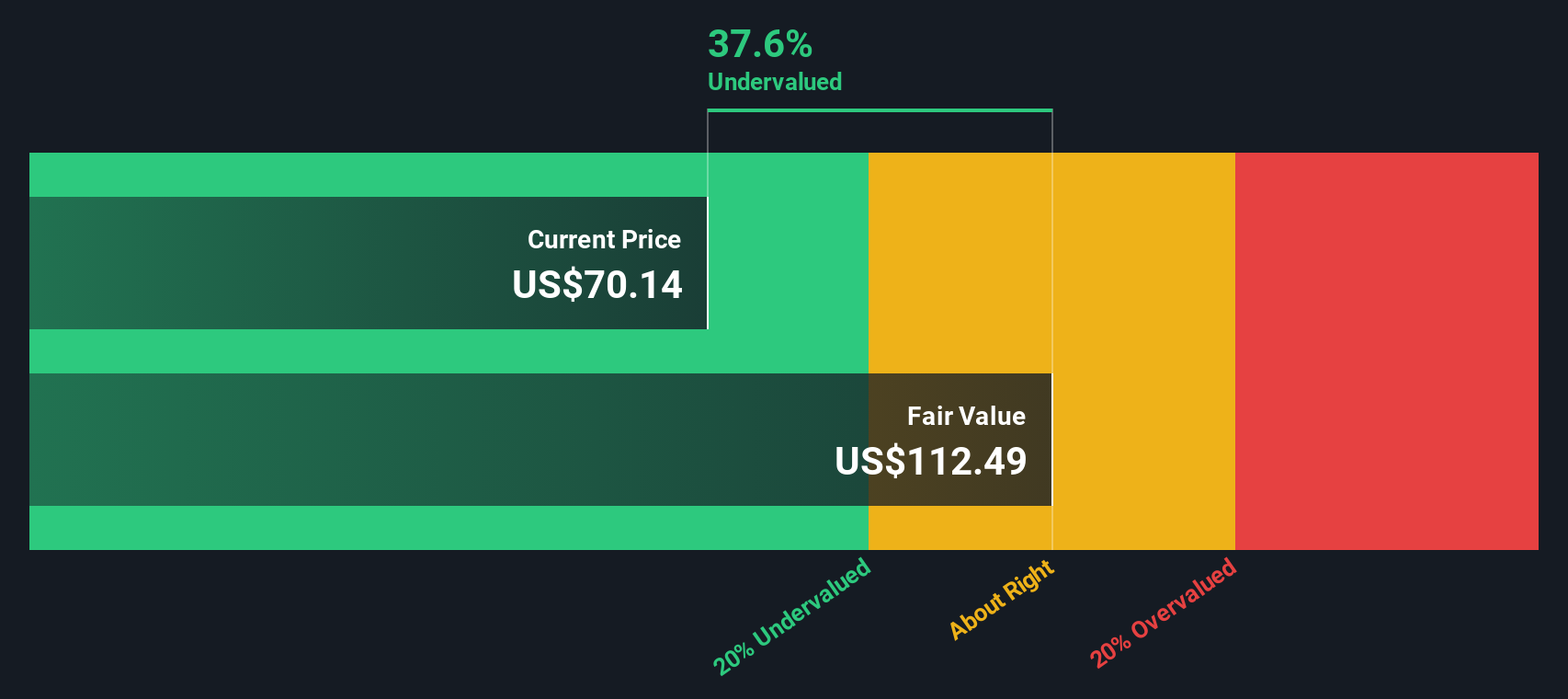

For Kroger, the latest twelve month free cash flow is about $2.2 billion. Analysts expect this to grow steadily, with projections and extrapolations pointing to free cash flow of roughly $3.1 billion by 2030. This is based on a two stage Free Cash Flow to Equity model that blends explicit analyst forecasts with longer term estimates from Simply Wall St.

When all those future cash flows are discounted back, the model arrives at an intrinsic value of about $88.82 per share. Versus a share price around $63, this implies Kroger is trading at roughly a 28.9% discount to its estimated fair value. This suggests investors are not fully pricing in its cash generation power.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kroger is undervalued by 28.9%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

Approach 2: Kroger Price vs Earnings

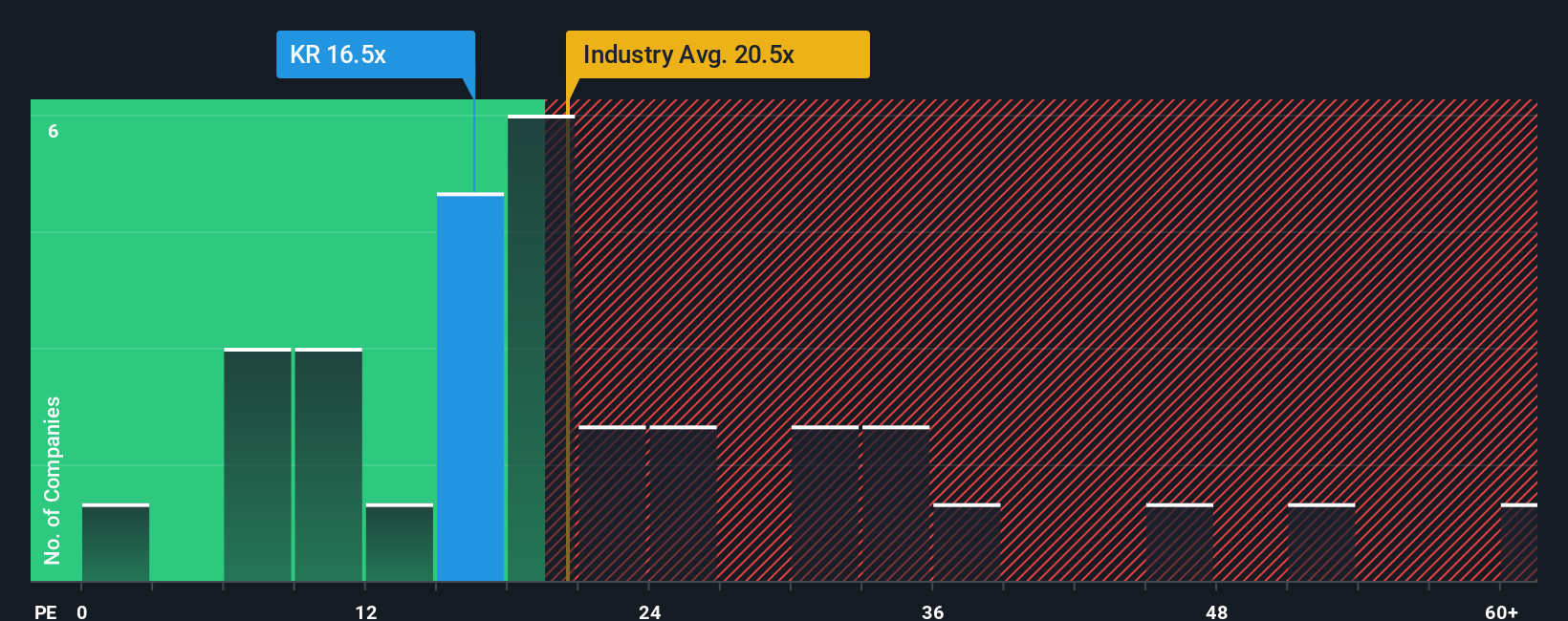

The price to earnings ratio is a useful way to value mature, profitable companies like Kroger because it links what investors pay directly to the earnings the business generates each year. In general, faster growth and lower risk justify a higher normal PE, while slower growth or higher uncertainty call for a lower one.

Kroger currently trades on a PE of about 52.8x, which is well above the Consumer Retailing industry average of roughly 22.7x and also higher than the peer group average of around 20.3x. At face value, that suggests the market is assigning a hefty premium to Kroger’s earnings.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what Kroger’s PE should be after adjusting for its specific earnings growth outlook, margins, risk profile, market cap and industry. On this basis, Kroger’s Fair Ratio comes out at about 37.6x, which is still below the current 52.8x. That gap indicates investors are paying more than what these fundamentals would typically justify, even after accounting for Kroger’s strengths and prospects.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kroger Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that lets you tell a clear story about Kroger; link that story to specific assumptions about its future revenue, earnings and margins; and instantly see a fair value you can compare with today’s price to decide whether to buy or sell. The whole view updates automatically as new news and earnings arrive. For example, one Kroger investor might build a bullish narrative around expanding delivery partnerships, healthier private label growth and rising EPS that supports a fair value in the mid $80s. Another might focus on e commerce profitability challenges, labor inflation and execution risk on automation and fulfillment, leading them to peg fair value closer to the low $60s. Narratives makes both perspectives transparent, quantified and easy to track over time.

Do you think there's more to the story for Kroger? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kroger might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KR

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)