- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:DLTR

Dollar Tree (DLTR) Completes Buyback, Reports Strong Earnings and Revenue Growth

Reviewed by Simply Wall St

Dollar Tree (DLTR) recently announced strong Q2 results with a rise in sales and net income, alongside a continued commitment to its share repurchase program. The company's updated fiscal guidance, along with its innovative partnership with Uber Eats, aligns with broader market trends of enhancing customer accessibility and operational efficiency. These initiatives likely supported the 25% quarterly price increase, despite the market being influenced by tech sector advancements and subtle movements in interest rates. As the S&P 500 and Nasdaq rose, Dollar Tree's strategic expansions and robust financial performance may have added more weight to its share price momentum.

We've spotted 3 possible red flags for Dollar Tree you should be aware of.

The recent developments at Dollar Tree, such as strong Q2 results and the partnership with Uber Eats, may provide substantial support to the company’s operational efficiency narrative. These moves align with the firm's strategy to focus on core business activities, potentially boosting revenue and net margins post-Family Dollar sale. The emphasis on multi-price assortments and store format upgrades could further invigorate sales and earnings, though continued strategic challenges like tariff exposure and rising costs may present hurdles to sustaining growth trajectory. Over the last year, Dollar Tree generated a total shareholder return of 36.37%, outperforming the broader market return of 15.7% and the Consumer Retailing industry return of 15.4%, signaling robust shareholder value creation relative to peers.

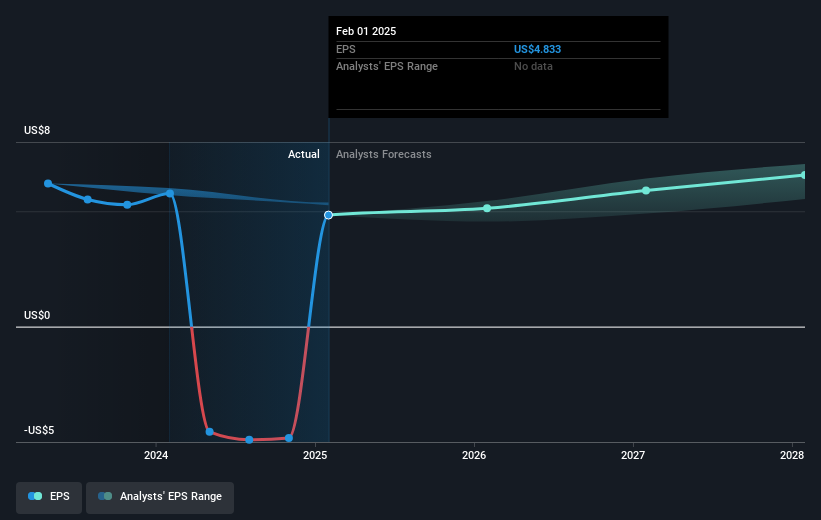

The analysts' consensus price target puts Dollar Tree slightly above its fair value, with the current share price closely mirroring the target at US$111.35. This indicates that the market believes the company is appropriately valued under current growth and risk assumptions. The company's shares have been gradually aligning with its projected earnings, where anticipated future earnings rise to US$1.4 billion by 2028 could justify tighter earnings forecasts. Revenue estimations are buoyed by upgrades and enhanced operational efficiency driven by recent corporate actions, although investor consideration of potential risks remains crucial. Overall, Dollar Tree's strategic alignment and financial performance appear supportive of its longer-term price target expectations.

Assess Dollar Tree's previous results with our detailed historical performance reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DLTR

Dollar Tree

Operates retail discount stores under the Dollar Tree and Dollar Tree Canada brands in the United States and Canada.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives