- United States

- /

- Consumer Durables

- /

- NasdaqGS:FLXS

Will Weakness in Flexsteel Industries, Inc.'s (NASDAQ:FLXS) Stock Prove Temporary Given Strong Fundamentals?

Flexsteel Industries (NASDAQ:FLXS) has had a rough three months with its share price down 36%. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. In this article, we decided to focus on Flexsteel Industries' ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Flexsteel Industries is:

12% = US$20m ÷ US$162m (Based on the trailing twelve months to December 2024).

The 'return' is the yearly profit. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.12 in profit.

See our latest analysis for Flexsteel Industries

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Flexsteel Industries' Earnings Growth And 12% ROE

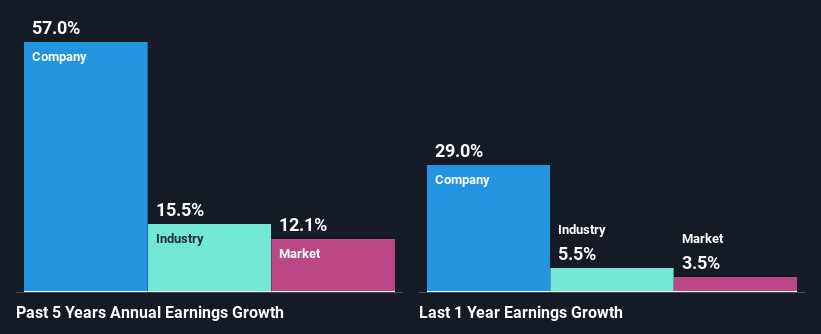

At first glance, Flexsteel Industries seems to have a decent ROE. And on comparing with the industry, we found that the the average industry ROE is similar at 15%. This certainly adds some context to Flexsteel Industries' exceptional 57% net income growth seen over the past five years. However, there could also be other drivers behind this growth. For instance, the company has a low payout ratio or is being managed efficiently.

As a next step, we compared Flexsteel Industries' net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 16%.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Flexsteel Industries fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Flexsteel Industries Efficiently Re-investing Its Profits?

Flexsteel Industries' three-year median payout ratio to shareholders is 23%, which is quite low. This implies that the company is retaining 77% of its profits. So it looks like Flexsteel Industries is reinvesting profits heavily to grow its business, which shows in its earnings growth.

Moreover, Flexsteel Industries is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years.

Summary

On the whole, we feel that Flexsteel Industries' performance has been quite good. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you're looking to trade Flexsteel Industries, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:FLXS

Flexsteel Industries

Operates as a manufacturer, importer, and markets of furniture for residential markets in the United States.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives