Advertisement

- United States

- /

- Professional Services

- /

- NYSE:TRU

Is TransUnion’s (TRU) Upbeat Q3 Results and Buybacks Reshaping Its Investment Case?

Simply Wall St

Reviewed by Sasha Jovanovic

- TransUnion recently reported third-quarter 2025 earnings showing year-over-year increases in both revenue and net income, while also raising its full-year guidance and reaching key milestones in its share repurchase program.

- The company’s announcement reflects growing confidence in its operational momentum and continued progress in shareholder return initiatives through buybacks.

- We’ll examine how TransUnion’s improved financial outlook and raised guidance are influencing its investment narrative moving forward.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

TransUnion Investment Narrative Recap

At its core, the investment case for TransUnion rests on belief in the expanding demand for consumer credit data, analytics, and identity solutions across global markets. The latest third-quarter results, highlighting solid revenue and earnings growth, as well as a raised full-year outlook, reinforce management's view that technology and product investments are paying off. This new momentum supports the narrative around ongoing profit growth, though it does not fundamentally alter the primary short-term catalyst (increasing adoption of new analytics offerings) or the biggest risk (regulatory and privacy headwinds), both of which remain central to the story.

The company’s completion of a $198.43 million buyback covering over 2.26 million shares and the recent increase in buyback authorization to $1 billion directly connects to the near-term focus on shareholder returns. While this signals confidence from the board and may add a meaningful component to total returns, its influence still operates within the broader context of business execution and margin resilience, especially as TransUnion builds scale in advanced analytics and fraud solutions.

But even as TransUnion advances on multiple fronts, investors should not lose sight of the continued pressure from tightening data privacy requirements worldwide ...

Read the full narrative on TransUnion (it's free!)

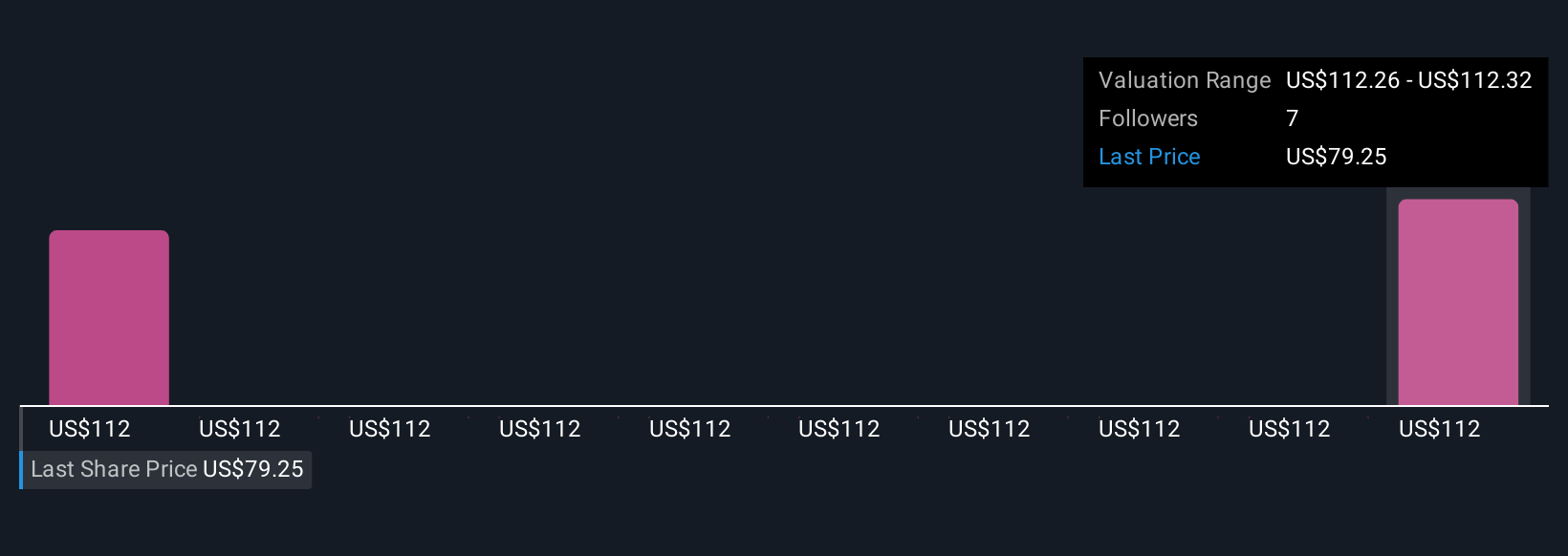

TransUnion's narrative projects $5.6 billion in revenue and $869.9 million in earnings by 2028. This requires 8.4% yearly revenue growth and a $477.9 million increase in earnings from the current level of $392.0 million.

Uncover how TransUnion's forecasts yield a $106.70 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members put fair value for TransUnion shares in a tight range between US$106.70 and US$108.64, with 2 separate viewpoints represented. Yet, regulatory scrutiny and shifting privacy demands persist as central concerns that could shape the company's growth and profitability going forward, compare these different outlooks and see how your own expectations align.

Explore 2 other fair value estimates on TransUnion - why the stock might be worth just $106.70!

Build Your Own TransUnion Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TransUnion research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free TransUnion research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TransUnion's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TransUnion might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TRU

TransUnion

Operates as a global consumer credit reporting agency that provides risk and information solutions.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor