- United States

- /

- Professional Services

- /

- NYSE:NSP

Here's What Insperity's (NYSE:NSP) Strong Returns On Capital Mean

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Ergo, when we looked at the ROCE trends at Insperity (NYSE:NSP), we liked what we saw.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Insperity:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

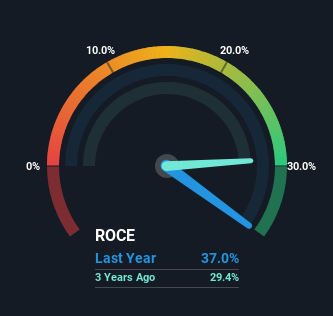

0.37 = US$273m ÷ (US$2.0b - US$1.3b) (Based on the trailing twelve months to March 2023).

Thus, Insperity has an ROCE of 37%. That's a fantastic return and not only that, it outpaces the average of 12% earned by companies in a similar industry.

See our latest analysis for Insperity

Above you can see how the current ROCE for Insperity compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Insperity here for free.

SWOT Analysis for Insperity

- Earnings growth over the past year exceeded the industry.

- Debt is not viewed as a risk.

- Dividends are covered by earnings and cash flows.

- Dividend is low compared to the top 25% of dividend payers in the Professional Services market.

- Annual revenue is forecast to grow faster than the American market.

- Current share price is below our estimate of fair value.

- Annual earnings are forecast to grow slower than the American market.

How Are Returns Trending?

Insperity deserves to be commended in regards to it's returns. The company has consistently earned 37% for the last five years, and the capital employed within the business has risen 93% in that time. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. If Insperity can keep this up, we'd be very optimistic about its future.

On a side note, Insperity's current liabilities are still rather high at 64% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

In Conclusion...

In the end, the company has proven it can reinvest it's capital at high rates of returns, which you'll remember is a trait of a multi-bagger. In light of this, the stock has only gained 35% over the last five years for shareholders who have owned the stock in this period. So because of the trends we're seeing, we'd recommend looking further into this stock to see if it has the makings of a multi-bagger.

If you'd like to know about the risks facing Insperity, we've discovered 1 warning sign that you should be aware of.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NSP

Insperity

Engages in the provision of human resources (HR) and business solutions to improve business performance for small and medium-sized businesses primarily in the United States.

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives