Jacobs (J): Valuation Check After Winning Key Role on Queensland’s Logan and Gold Coast Faster Rail Project

Reviewed by Simply Wall St

Jacobs Solutions (J) just picked up a meaningful role in Australia, being named Project Independent Certifier, alongside Arcadis, for Queensland's Logan and Gold Coast Faster Rail Project. This contract reinforces its complex infrastructure credentials.

See our latest analysis for Jacobs Solutions.

The new Australian rail role lands at a time when Jacobs’ 1 month share price return of negative 12.10 percent has cooled the stock’s near term momentum, even as its 3 year total shareholder return of 41.58 percent still reflects a solid long term compounding story.

If this kind of infrastructure exposure appeals to you, it could be worth exploring aerospace and defense stocks as another way to find companies leveraged to large, long dated government and engineering programs.

Yet with shares pulling back even as analysts see double digit upside to their price targets and fundamentals still compounding, is Jacobs quietly slipping into undervalued territory, or is the market already baking in years of growth?

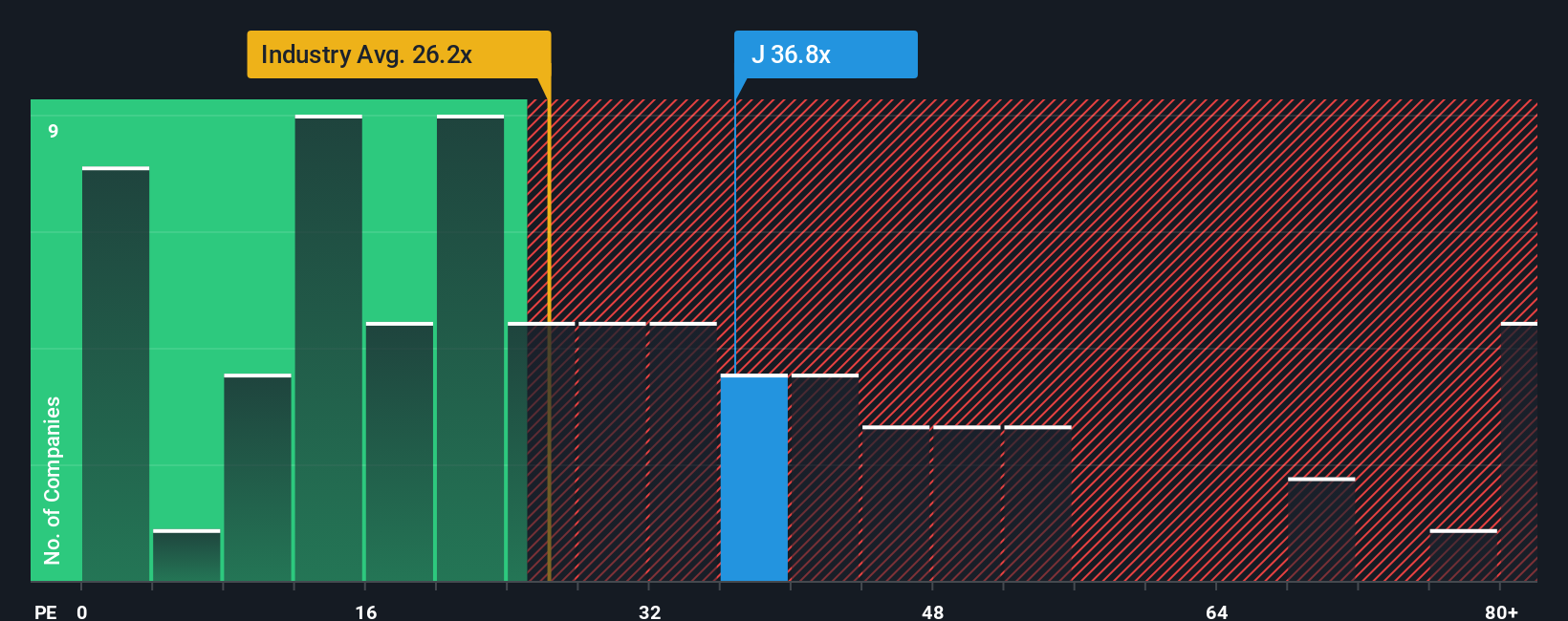

Most Popular Narrative: 15% Undervalued

Compared with Jacobs Solutions' last close at $135.72, the most followed narrative points to a materially higher fair value anchored in compounding fundamentals.

Record-high backlog growth (up 14% year over year) in Water, Advanced Facilities, and Critical Infrastructure driven by global infrastructure modernization, water scarcity, and data center expansion provides strong visibility into multi-year revenue growth and supports confidence in accelerating top-line results into FY '26 and beyond.

Want to see what turns that backlog into a higher valuation? The narrative leans on faster earnings growth, rising margins, and a future multiple that assumes sustained execution. Curious how those pieces fit together into that higher fair value?

Result: Fair Value of $159.69 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside case could be challenged if government infrastructure budgets tighten or large, long dated projects encounter execution issues and cost overruns.

Find out about the key risks to this Jacobs Solutions narrative.

Another Angle on Value

Our fair value work paints Jacobs as 41.7 percent undervalued, but the earnings multiple tells a tougher story. At 51.3 times earnings, versus 25 times for the US Professional Services industry and a 31.4 times fair ratio, the stock screens expensive. Is this a quality premium or downside risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Jacobs Solutions Narrative

If you see the story differently, or prefer building your own view from the numbers, you can assemble a full narrative in minutes: Do it your way.

A great starting point for your Jacobs Solutions research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next watchlist upgrades by using the Simply Wall St Screener to uncover focused opportunities you would not want to miss.

- Target steady cash returns with these 13 dividend stocks with yields > 3% that can help support an income focused portfolio through changing market cycles.

- Amplify your growth potential by scanning these 26 AI penny stocks that are poised to benefit from the accelerating adoption of artificial intelligence across industries.

- Strengthen your value playbook with these 908 undervalued stocks based on cash flows that may be trading below their intrinsic worth based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:J

Jacobs Solutions

Engages in the infrastructure and advanced facilities, and consulting businesses in the United States, Europe, Canada, India, Asia, Australia, New Zealand, the Middle East, and Africa.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)