Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:VRSK

With EPS Growth And More, Verisk Analytics (NASDAQ:VRSK) Makes An Interesting Case

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

In contrast to all that, many investors prefer to focus on companies like Verisk Analytics (NASDAQ:VRSK), which has not only revenues, but also profits. While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Verisk Analytics

How Quickly Is Verisk Analytics Increasing Earnings Per Share?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. We can see that in the last three years Verisk Analytics grew its EPS by 14% per year. That's a good rate of growth, if it can be sustained.

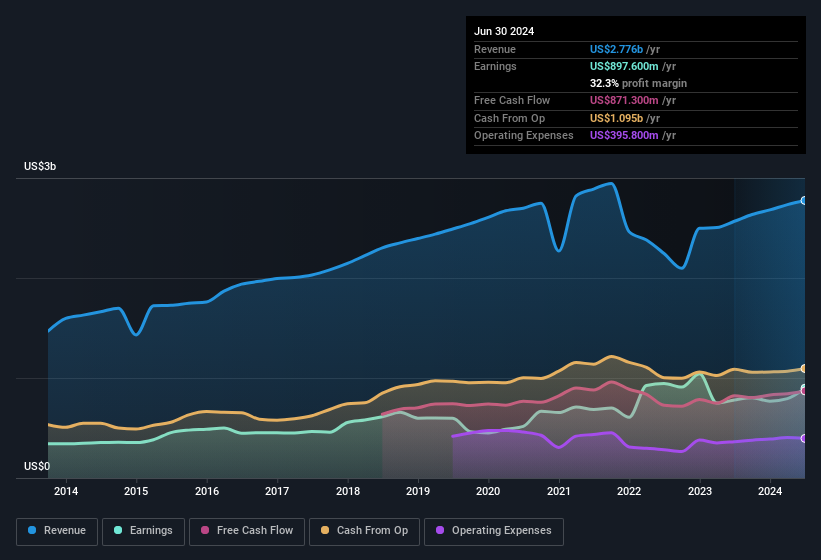

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. While we note Verisk Analytics achieved similar EBIT margins to last year, revenue grew by a solid 8.1% to US$2.8b. That's a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Verisk Analytics' future profits.

Are Verisk Analytics Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

It's worth noting that there was some insider selling of Verisk Analytics shares last year, worth US$54k. This falls short of the share acquisition by Independent Director Wendy Lane, who has acquired US$158k worth of shares, at an average price of US$264. And that's a reason to be optimistic.

The good news, alongside the insider buying, for Verisk Analytics bulls is that insiders (collectively) have a meaningful investment in the stock. With a whopping US$59m worth of shares as a group, insiders have plenty riding on the company's success. This should keep them focused on creating long term value for shareholders.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That's because Verisk Analytics' CEO, Lee Shavel, is paid at a relatively modest level when compared to other CEOs for companies of this size. Our analysis has discovered that the median total compensation for the CEOs of companies like Verisk Analytics, with market caps over US$8.0b, is about US$13m.

The Verisk Analytics CEO received US$10m in compensation for the year ending December 2023. That is actually below the median for CEO's of similarly sized companies. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of good governance, more generally.

Should You Add Verisk Analytics To Your Watchlist?

As previously touched on, Verisk Analytics is a growing business, which is encouraging. On top of that, we've seen insiders buying shares even though they already own plenty. That should do plenty in prompting budding investors to undertake a bit more research - or even adding the company to their watchlists. We don't want to rain on the parade too much, but we did also find 1 warning sign for Verisk Analytics that you need to be mindful of.

Keen growth investors love to see insider activity. Thankfully, Verisk Analytics isn't the only one. You can see a a curated list of companies which have exhibited consistent growth accompanied by high insider ownership.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:VRSK

Verisk Analytics

Engages in the provision of data analytics and technology solutions to the insurance industry in the United States and internationally.

Solid track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor