- United States

- /

- Professional Services

- /

- NasdaqGS:HSII

December 2024's Undervalued Small Caps With Insider Action On US Markets

Reviewed by Simply Wall St

Over the last 7 days, the United States market has remained flat, yet it has seen a significant rise of 27% over the past 12 months, with earnings forecasted to grow by 15% annually. In this context, identifying small-cap stocks that are potentially undervalued and have insider activity can present intriguing opportunities for investors looking to navigate these dynamic market conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Capital Bancorp | 15.7x | 3.2x | 42.12% | ★★★★☆☆ |

| Franklin Financial Services | 10.4x | 2.0x | 36.64% | ★★★★☆☆ |

| McEwen Mining | 4.3x | 2.2x | 44.66% | ★★★★☆☆ |

| ProPetro Holding | NA | 0.6x | 38.16% | ★★★★☆☆ |

| German American Bancorp | 16.1x | 5.3x | 40.66% | ★★★☆☆☆ |

| First United | 14.3x | 3.2x | 44.98% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Tilray Brands | NA | 1.3x | -62.08% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -56.11% | ★★★☆☆☆ |

| Sabre | NA | 0.5x | -91.22% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

Capital Bancorp (NasdaqGS:CBNK)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Capital Bancorp operates as a diversified financial services company with segments in commercial banking, home loans, and an OpenSky credit card division, and has a market cap of approximately $0.33 billion.

Operations: Capital Bancorp generates revenue primarily through its Commercial Bank and Opensky segments, contributing $79.24 million and $69.46 million respectively. The company has consistently achieved a gross profit margin of 100%, indicating that it incurs no cost of goods sold in its financial reporting. Operating expenses are dominated by general and administrative costs, which were approximately $92.24 million in the latest period, impacting the net income margin which was 20.57%.

PE: 15.7x

Capital Bancorp, a smaller U.S. company, shows potential in the undervalued stock category. Recent earnings for Q3 2024 revealed net interest income of US$38.35 million, up from US$36.81 million the previous year, though net income slightly declined to US$8.67 million from US$9.79 million last year. Despite some challenges like increased charge-offs of US$2.66 million, insider confidence is evident with recent share repurchases completed at 543,215 shares for US$9.69 million since July 2022's buyback announcement.

- Click to explore a detailed breakdown of our findings in Capital Bancorp's valuation report.

Understand Capital Bancorp's track record by examining our Past report.

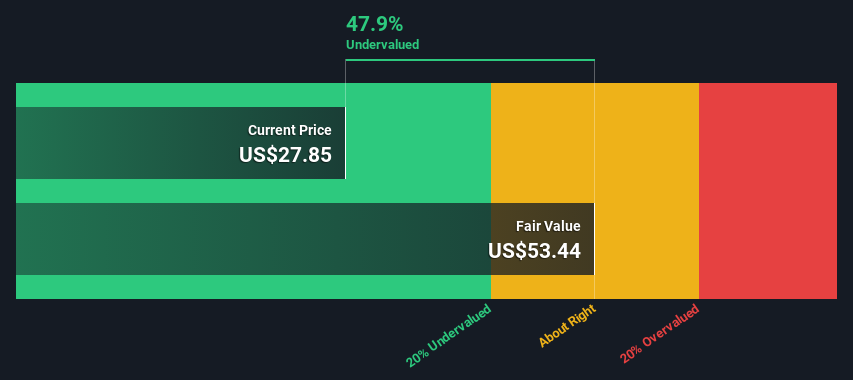

Heidrick & Struggles International (NasdaqGS:HSII)

Simply Wall St Value Rating: ★★★★★☆

Overview: Heidrick & Struggles International is a global executive search and consulting firm offering services in on-demand talent, consulting, and executive search across the Americas, Europe, and Asia Pacific with a market capitalization of approximately $1.07 billion.

Operations: Heidrick & Struggles International generates revenue through its segments, with Executive Search in the Americas being the largest contributor at $543.08 million. The company has seen fluctuations in its net income margin, which reached 7.47% as of September 30, 2021, but declined to 3.59% by September 30, 2024. Operating expenses have varied over time and include significant general and administrative costs that were $170.09 million by late 2024.

PE: 24.1x

Heidrick & Struggles, a company with a strong presence in executive search and consulting, has recently shown signs of insider confidence as Thomas Monahan purchased 7,500 shares for approximately US$302,825. This move suggests belief in the company's future prospects despite a current net profit margin decline from 5.5% to 3.6%. The appointment of Nirupam Sinha as CFO is anticipated to bring strategic financial leadership starting January 2025. While the company faces challenges with its external borrowing structure and recent earnings dip—US$14.83 million compared to US$14.99 million last year—it forecasts earnings growth of over 29% annually, indicating potential value for investors seeking opportunities in smaller market capitalization stocks.

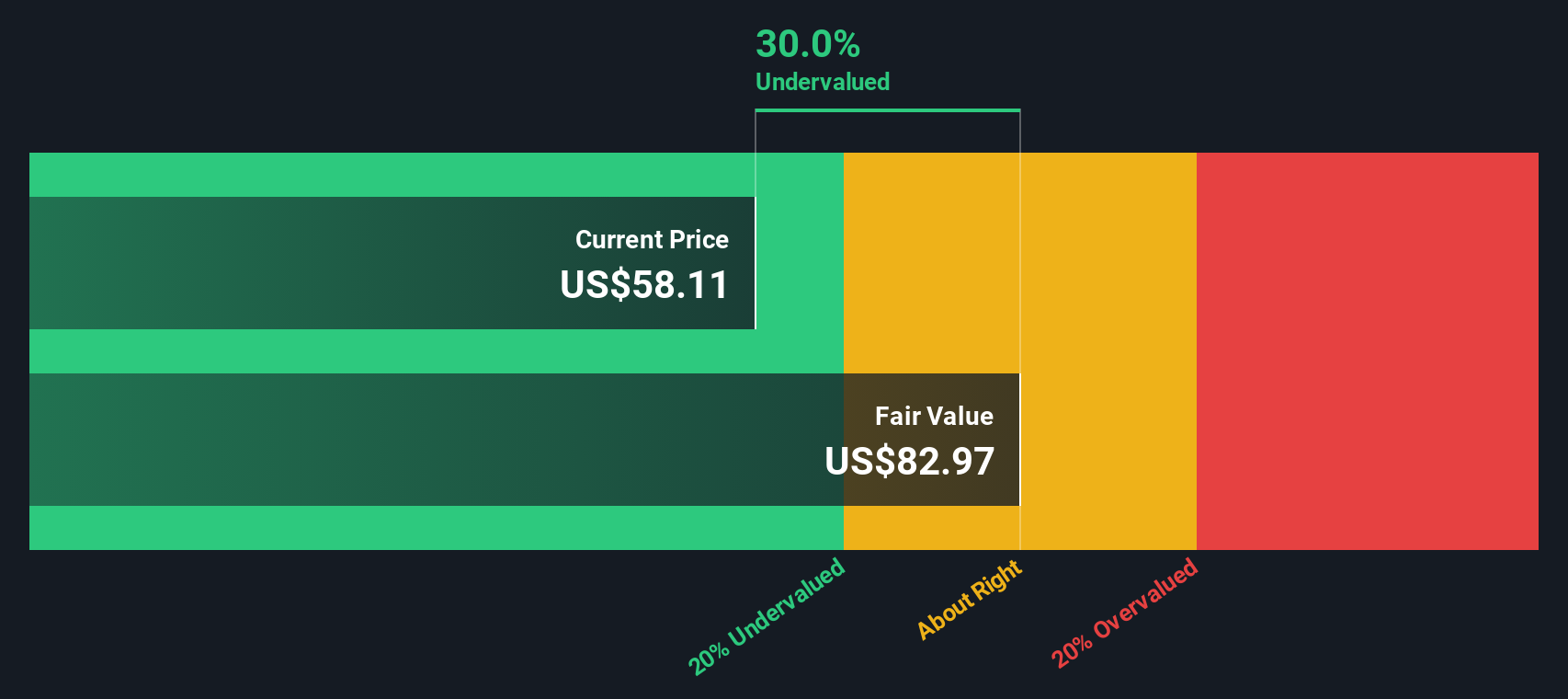

Methode Electronics (NYSE:MEI)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Methode Electronics is a company that designs and manufactures custom-engineered solutions for various industries, including automotive, industrial, and interface sectors, with a market capitalization of approximately $1.61 billion.

Operations: Methode Electronics generates revenue primarily from the Automotive and Industrial segments, contributing $576.30 million and $499.30 million respectively. Over recent periods, the company's gross profit margin has shown a declining trend, reaching 16.21% in the latest period. Operating expenses have increased to $183.4 million, impacting overall profitability with net income margins turning negative at -8.16%.

PE: -5.2x

Methode Electronics, a smaller company in the U.S. market, has seen insider confidence with Independent Director David Blom purchasing 9,320 shares for US$100,749 in recent months. Despite facing operational challenges and legal issues impacting its automotive segment, the company's earnings forecast suggests potential growth of 163% annually. Recent financial results show a narrowing net loss and steady sales figures. Additionally, Methode declared a quarterly dividend of US$0.14 per share to be paid early next year.

Where To Now?

- Unlock more gems! Our Undervalued US Small Caps With Insider Buying screener has unearthed 38 more companies for you to explore.Click here to unveil our expertly curated list of 41 Undervalued US Small Caps With Insider Buying.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Heidrick & Struggles International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Heidrick & Struggles International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HSII

Heidrick & Struggles International

Provides executive search, consulting, and on-demand talent services to businesses and business leaders worldwide.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives