- United States

- /

- Commercial Services

- /

- NasdaqGS:CMPR

Forecast Changes Might Change the Case for Investing in Cimpress (CMPR)

Reviewed by Sasha Jovanovic

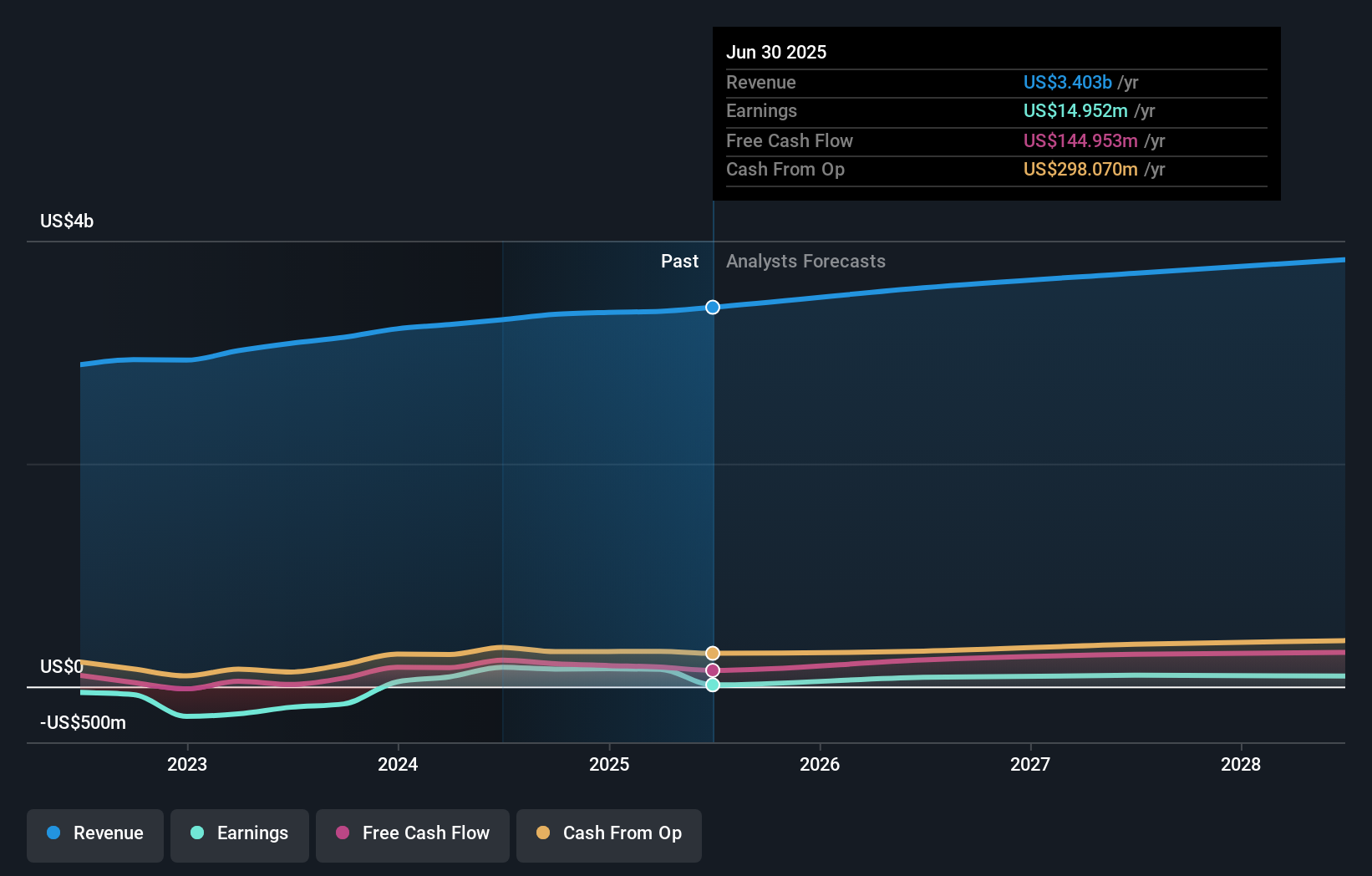

- Cimpress PLC's Q1 2026 earnings report was released on October 29, 2025, following a previous quarter where the company surpassed revenue expectations but reported an earnings miss, prompting a wave of analyst estimate revisions.

- While analysts have raised full-year 2026 revenue projections, they have concurrently lowered earnings forecasts, reflecting renewed attention on the company's evolving margin outlook and cost-efficiency plans.

- We'll explore how the recent updates to Cimpress's revenue and earnings forecasts may influence its long-term investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Cimpress Investment Narrative Recap

To be a Cimpress shareholder, you need to see long-term opportunity in its shift from declining print categories to higher-value, customized products and technology-driven efficiency. The latest news, where earnings estimates come down while revenue projections rise, primarily highlights continued margin pressures as the near-term catalyst, but it does not fundamentally change the most urgent risk, which is whether new segments can offset core print decline. Of Cimpress’s recent moves, its ongoing share buybacks stand out given recent performance. While these repurchases signal confidence in the business and have supported the stock price in the wake of the last earnings release, their impact is closely tied to whether the company can eventually convert higher revenue into stronger earnings and sustained free cash flow. But for investors, it’s worth noting that despite revenue optimism, the margin pressures may not be…

Read the full narrative on Cimpress (it's free!)

Cimpress' outlook forecasts $3.8 billion in revenue and $94.7 million in earnings by 2028. This is based on analysts' expectations of 4.0% annual revenue growth and an increase in earnings of $79.7 million from the current $15.0 million.

Uncover how Cimpress' forecasts yield a $77.50 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Three individuals from the Simply Wall St Community estimate Cimpress’s fair value between US$77.50 and US$3,107.51. As the company pushes into higher-value categories with slower top-line growth, readers will see opinions can differ, and it’s smart to consider multiple perspectives.

Explore 3 other fair value estimates on Cimpress - why the stock might be worth just $77.50!

Build Your Own Cimpress Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cimpress research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cimpress research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cimpress' overall financial health at a glance.

No Opportunity In Cimpress?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CMPR

Cimpress

Provides various mass customization of printing and related products in North America, Europe, and internationally.

Moderate growth potential with low risk.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)