- United States

- /

- Machinery

- /

- NYSE:OTIS

Is Otis a Smart Pick After Recent Flat Performance and Five Year Outperformance?

Reviewed by Bailey Pemberton

Thinking about what to do with your Otis Worldwide shares, or deciding if now is the right time to jump in? You are not alone. Otis may not always grab the headlines, but recent stock movements have surely challenged investor expectations. After a relatively flat 30 days, with the stock inching up just 0.1%, and a slight dip of 1.8% over the last week, some are taking a closer look, especially considering Otis is still down 13.9% over the past year. Yet, zoom out a bit, and the picture brightens. Over the last five years, the stock is up an impressive 49.1%, handily outpacing many industrial peers, and it has notched an impressive 43.2% return over three years.

So is this a case of the market underestimating Otis, or is there greater risk looming? A run of muted short-term performance can sometimes signal opportunity. Savvy investors are often most interested when attention is elsewhere. Our latest valuation analysis gives Otis a score of 4 out of 6 on key “undervalued” checks, suggesting the company is currently more attractively priced than most in its sector.

Up next, we will walk through these valuation checks and see what they really mean for your investing decisions. If you are looking for more than just the numbers, stick around. There is an even more insightful way to judge Otis’s true value that we will reveal at the end.

Why Otis Worldwide is lagging behind its peers

Approach 1: Otis Worldwide Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today’s value. This approach helps investors determine if a stock is trading below or above what those future cash flows are truly worth.

For Otis Worldwide, the latest reported Free Cash Flow is $1.36 Billion, forming the baseline for the valuation. Analysts have provided estimates for the next five years, expecting steady growth in cash flows. According to projections, Otis’s Free Cash Flow could reach $3.08 Billion by 2035. Estimates beyond 2029 are extrapolations rather than direct analyst forecasts.

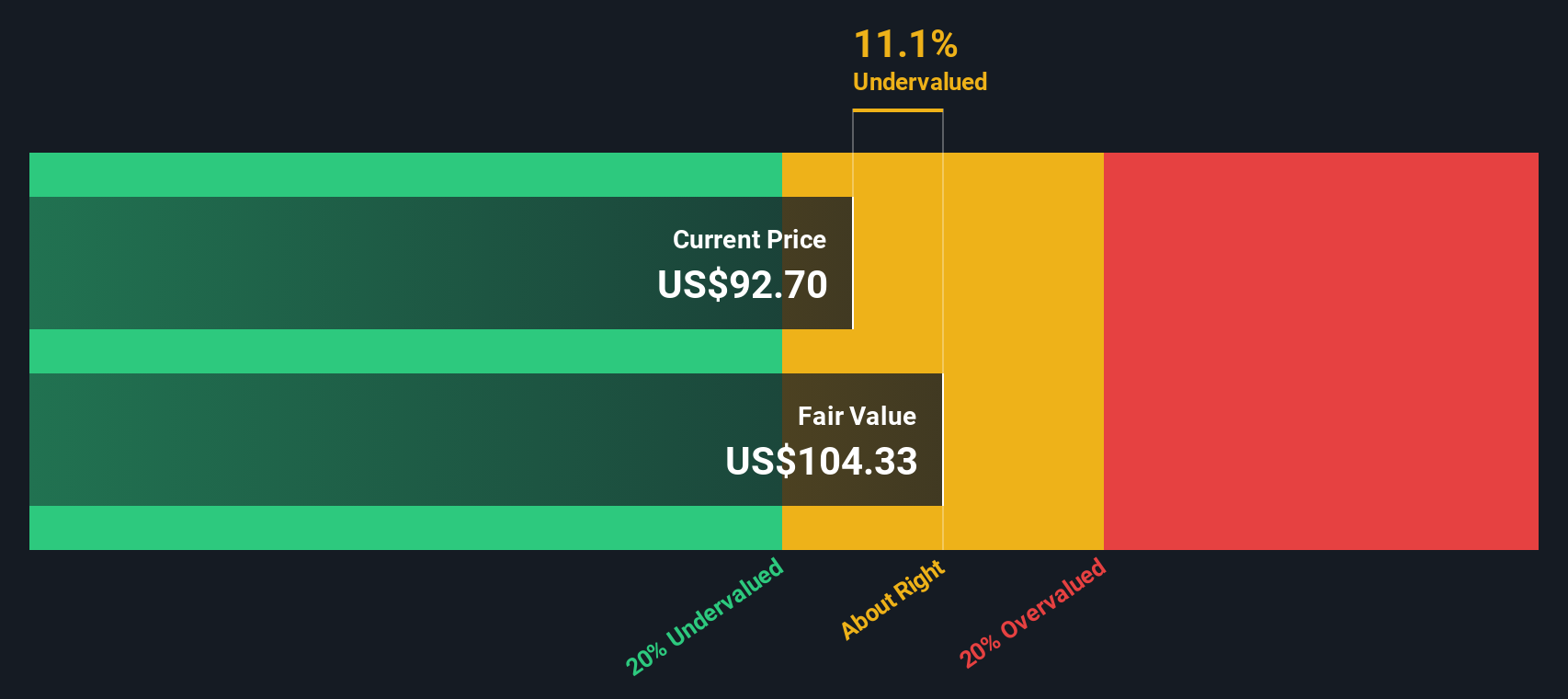

The DCF analysis assigns an intrinsic value of $104.87 per share to Otis, compared to recent market pricing. This suggests the stock is 15.0% undervalued and that there may be a notable margin of safety at current levels. The model indicates that, despite recent short-term volatility, underlying cash generation is projected to rise meaningfully over the next decade.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Otis Worldwide is undervalued by 15.0%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Otis Worldwide Price vs Earnings

When analyzing a consistently profitable company like Otis Worldwide, the Price-to-Earnings (PE) ratio is often the most relevant valuation metric. The PE ratio provides a straightforward snapshot of how much investors are willing to pay for each dollar of the company’s earnings, making it a reliable tool for comparing relative value among profitable peers.

What constitutes a "normal" or "fair" PE ratio depends on a balancing act between a company’s expected earnings growth and the risks it faces. Typically, higher growth prospects or lower risk profiles justify higher PE multiples. Mature companies or those facing significant uncertainty often command lower PE ratios.

Currently, Otis trades at a PE ratio of 23.1x. That is just below the Machinery industry average of 23.5x and well below the peer group average of 36.4x. Looking beyond these raw comparisons, Simply Wall St calculates a “Fair Ratio” for Otis of 24.7x. This Fair Ratio integrates essential factors such as expected earnings growth, risk profile, profit margins, market cap, and the broader industry landscape. Unlike simple industry or peer averages, the Fair Ratio provides a more personalized benchmark for Otis’s valuation.

Given the Fair Ratio is just a touch above the current PE, this analysis suggests Otis is valued about right in context of its fundamentals and future outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Otis Worldwide Narrative

Earlier we mentioned there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is your personalized story that ties together what you believe about a company, how that impacts its expected future performance, and the fair value you assign to the stock. Narratives help you go beyond the numbers by linking your view on Otis’s competitive strengths, industry shifts, and future catalysts directly to your own revenue, margin, and valuation forecasts.

This intuitive tool, available for free in the Simply Wall St Community, empowers millions of investors to capture and track their unique perspectives right on the company’s page in just a few minutes. With Narratives, you can easily compare your Fair Value to current market prices and decide whether Otis is a buy, hold, or sell. At the same time, you can see how your investment thesis evolves over time as new information or earnings updates arrive.

For example, some investors build bullish Narratives for Otis based on hopes for large-scale modernization orders and robust service growth, resulting in a fair value as high as $134, while others adopt a more cautious view focused on demand risks and price in a lower target around $90. Narratives give you the freedom and structure to make smarter, more personalized investment decisions in real time.

Do you think there's more to the story for Otis Worldwide? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OTIS

Otis Worldwide

Engages in manufacturing, installation, and servicing of elevators and escalators in the United States, China, and internationally.

Good value second-rate dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)