- United States

- /

- Software

- /

- NYSE:PRO

3 Undervalued Small Caps In United States With Insider Buying

Reviewed by Simply Wall St

Over the last 7 days, the United States market has remained flat, yet it has experienced a significant rise of 39% over the past 12 months, with earnings forecasted to grow by 15% annually. In this context, identifying small-cap stocks that are perceived as undervalued and have insider buying activity can be an intriguing opportunity for investors seeking potential growth amidst steady market conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Columbus McKinnon | 20.2x | 0.9x | 44.37% | ★★★★★★ |

| Hanover Bancorp | 9.6x | 2.2x | 45.69% | ★★★★★☆ |

| Franklin Financial Services | 10.3x | 2.0x | 31.50% | ★★★★☆☆ |

| HighPeak Energy | 10.9x | 1.4x | 40.72% | ★★★★☆☆ |

| Citizens & Northern | 13.4x | 2.9x | 43.88% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Orion Group Holdings | NA | 0.3x | -96.12% | ★★★☆☆☆ |

| Sabre | NA | 0.5x | -61.88% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -45.24% | ★★★☆☆☆ |

| Industrial Logistics Properties Trust | NA | 0.6x | -183.42% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

Sabre (NasdaqGS:SABR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Sabre operates as a technology solutions provider for the global travel and tourism industry, with a market cap of $1.43 billion.

Operations: Sabre generates revenue primarily from its Travel Solutions and Hospitality Solutions segments, with recent figures showing $2.70 billion and $315.74 million respectively. The company's gross profit margin has shown variability, recently recorded at 59.47%. Operating expenses have been significant, with research and development costs being a major component at $882.44 million in the latest period analyzed.

PE: -3.5x

Sabre Corporation, a prominent player in travel technology, is gaining attention as a potentially undervalued stock. Despite recent shareholder dilution and reliance on external borrowing for funding, Sabre's strategic moves include new distribution agreements with Premier Inn and World Travel, enhancing its global reach. The company forecasts significant earnings growth of 90% annually. Recent insider confidence is evident with share purchases over the past year. Upcoming board changes may influence future strategic direction positively.

- Dive into the specifics of Sabre here with our thorough valuation report.

Examine Sabre's past performance report to understand how it has performed in the past.

Custom Truck One Source (NYSE:CTOS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Custom Truck One Source provides specialized truck and heavy equipment solutions, including sales, aftermarket parts and services, and equipment rental solutions, with a market cap of approximately $1.59 billion.

Operations: The company generates revenue primarily from Truck and Equipment Sales, Aftermarket Parts and Services, and Equipment Rental Solutions. The gross profit margin has shown variability, peaking at 32.78% in December 2019 before experiencing fluctuations to reach 23.12% by October 2024. Operating expenses have been a significant cost factor, with General & Administrative Expenses being a notable component within this category.

PE: -63.5x

Custom Truck One Source, a smaller company in the U.S. market, is attracting attention due to its potential for growth despite recent financial setbacks. Earnings are projected to grow by 92.85% annually, indicating strong future prospects. However, the company relies entirely on external borrowing for funding, which poses higher risks compared to customer deposits. Notably, insider confidence is evident with significant share repurchases from April to June 2024 totaling US$16.87 million. As they prepare to announce Q3 results today, investors might anticipate insights into their strategic direction amidst these dynamics.

- Click to explore a detailed breakdown of our findings in Custom Truck One Source's valuation report.

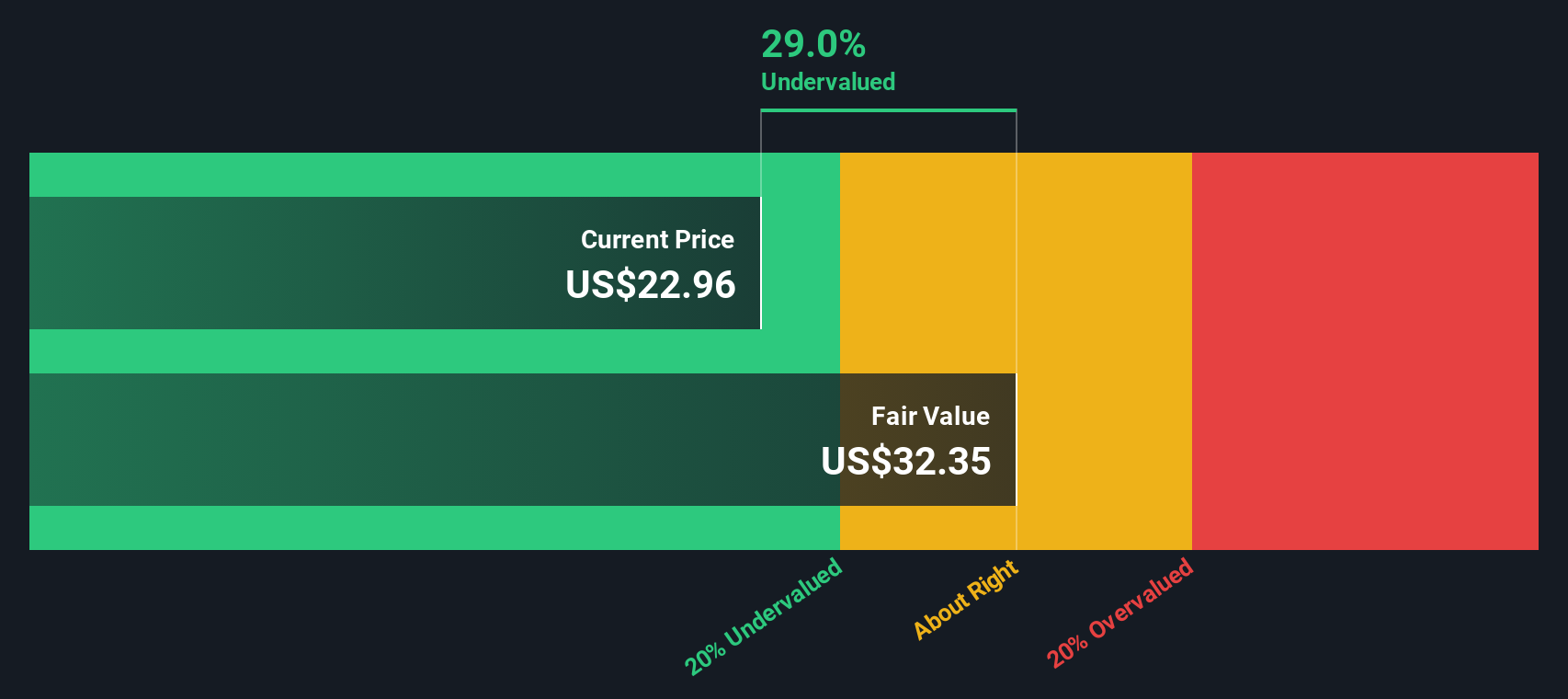

PROS Holdings (NYSE:PRO)

Simply Wall St Value Rating: ★★★★★☆

Overview: PROS Holdings is a company that specializes in providing AI-powered software solutions designed to optimize pricing, selling, and revenue management processes for businesses, with a market capitalization of approximately $1.50 billion.

Operations: PROS Holdings generates revenue primarily from its Software & Programming segment, which amounted to $317.44 million in the latest period. The company's gross profit margin has shown an upward trend, reaching 63.82% recently. Operating expenses are significant and include costs related to sales and marketing, research and development, and general administrative functions.

PE: -21.4x

PROS Holdings, a smaller company in the tech sector, recently reported a revenue increase to US$82.7 million for Q3 2024 from US$77.25 million last year and achieved a net income of US$0.235 million, reversing a loss from the previous year. Despite past shareholder dilution and reliance on external borrowing, it continues to innovate with offerings like PROS Smart Rebate Management. With insider confidence evident through recent share purchases, the company anticipates further revenue growth in Q4 2024 between US$84.1 million and US$85.1 million amidst leadership transitions as CEO Andres Reiner plans retirement while ensuring smooth succession planning.

- Get an in-depth perspective on PROS Holdings' performance by reading our valuation report here.

Review our historical performance report to gain insights into PROS Holdings''s past performance.

Seize The Opportunity

- Click here to access our complete index of 48 Undervalued US Small Caps With Insider Buying.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PRO

PROS Holdings

Provides software solutions that optimize the processes of selling and shopping in the digital economy in Europe, the Asia Pacific, the Middle East, Africa, and internationally.

Undervalued low.