Advertisement

- United States

- /

- Machinery

- /

- NasdaqGS:TWIN

Here's Why Twin Disc (NASDAQ:TWIN) Has A Meaningful Debt Burden

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Twin Disc, Incorporated (NASDAQ:TWIN) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Twin Disc

What Is Twin Disc's Debt?

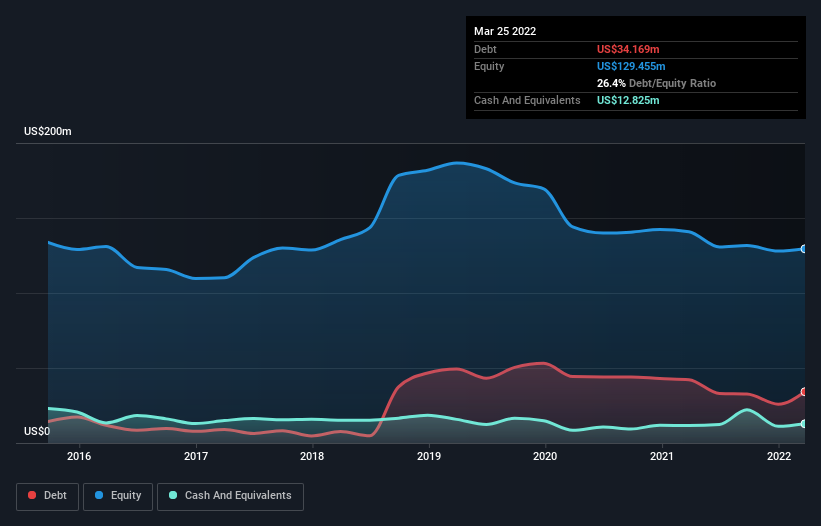

As you can see below, Twin Disc had US$34.2m of debt at March 2022, down from US$42.2m a year prior. However, because it has a cash reserve of US$12.8m, its net debt is less, at about US$21.3m.

How Healthy Is Twin Disc's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Twin Disc had liabilities of US$85.0m due within 12 months and liabilities of US$63.3m due beyond that. Offsetting these obligations, it had cash of US$12.8m as well as receivables valued at US$39.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$96.5m.

This deficit is considerable relative to its market capitalization of US$123.3m, so it does suggest shareholders should keep an eye on Twin Disc's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Twin Disc's low debt to EBITDA ratio of 1.3 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 2.9 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. We also note that Twin Disc improved its EBIT from a last year's loss to a positive US$6.4m. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Twin Disc can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, Twin Disc burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Mulling over Twin Disc's attempt at converting EBIT to free cash flow, we're certainly not enthusiastic. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Twin Disc's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. Even though Twin Disc lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check out how earnings have been trending over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Twin Disc might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TWIN

Twin Disc

Engages in the design, manufacture, and sale of marine and heavy duty off-highway power transmission equipment in the United States, the Netherlands, China, Australia, Italy, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor