- United States

- /

- Trade Distributors

- /

- NasdaqGS:TITN

Here's Why We Think Titan Machinery (NASDAQ:TITN) Is Well Worth Watching

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Titan Machinery (NASDAQ:TITN). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

See our latest analysis for Titan Machinery

Titan Machinery's Improving Profits

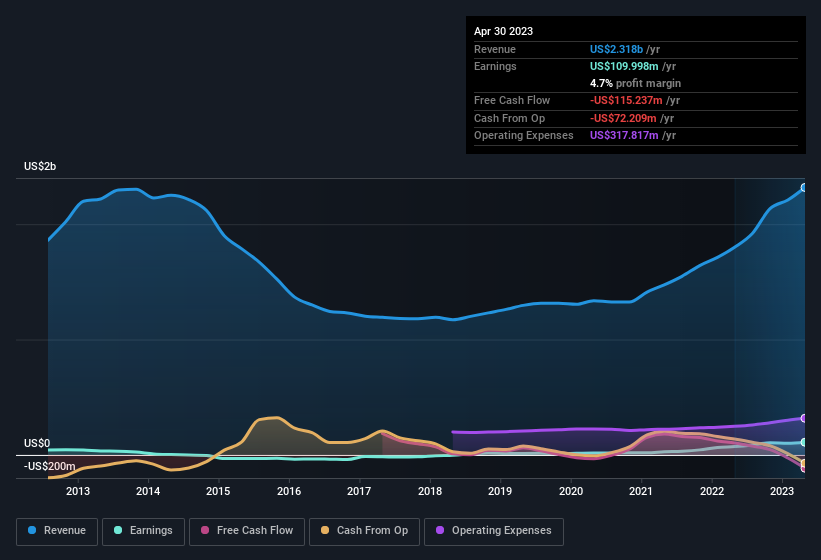

Over the last three years, Titan Machinery has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. Thus, it makes sense to focus on more recent growth rates, instead. Titan Machinery's EPS skyrocketed from US$3.23 to US$4.91, in just one year; a result that's bound to bring a smile to shareholders. That's a commendable gain of 52%.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. While we note Titan Machinery achieved similar EBIT margins to last year, revenue grew by a solid 29% to US$2.3b. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Titan Machinery's forecast profits?

Are Titan Machinery Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Belief in the company remains high for insiders as there hasn't been a single share sold by the management or company board members. But more importantly, Lead Independent Director Stan Erickson spent US$89k acquiring shares, doing so at an average price of US$29.67. Strong buying like that could be a sign of opportunity.

On top of the insider buying, it's good to see that Titan Machinery insiders have a valuable investment in the business. With a whopping US$67m worth of shares as a group, insiders have plenty riding on the company's success. That holding amounts to 11% of the stock on issue, thus making insiders influential owners of the business and aligned with the interests of shareholders.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That's because Titan Machinery's CEO, David Meyer, is paid at a relatively modest level when compared to other CEOs for companies of this size. Our analysis has discovered that the median total compensation for the CEOs of companies like Titan Machinery with market caps between US$400m and US$1.6b is about US$3.5m.

The Titan Machinery CEO received total compensation of just US$487k in the year to January 2023. First impressions seem to indicate a compensation policy that is favourable to shareholders. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Should You Add Titan Machinery To Your Watchlist?

You can't deny that Titan Machinery has grown its earnings per share at a very impressive rate. That's attractive. On top of that, insiders own a significant piece of the pie when it comes to the company's stock, and one has been buying more. Astute investors will want to keep this stock on watch. You should always think about risks though. Case in point, we've spotted 4 warning signs for Titan Machinery you should be aware of, and 3 of them are significant.

Keen growth investors love to see insider buying. Thankfully, Titan Machinery isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade Titan Machinery, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Titan Machinery might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TITN

Titan Machinery

Owns and operates a network of full service agricultural and construction equipment stores in the United States, Europe, and Australia.

Fair value with imperfect balance sheet.

Similar Companies

Market Insights

Community Narratives