Advertisement

- United States

- /

- Banks

- /

- NYSE:HTH

Weaker Profitability and Efficiency Might Change the Case for Investing in Hilltop Holdings (HTH)

Simply Wall St

Reviewed by Sasha Jovanovic

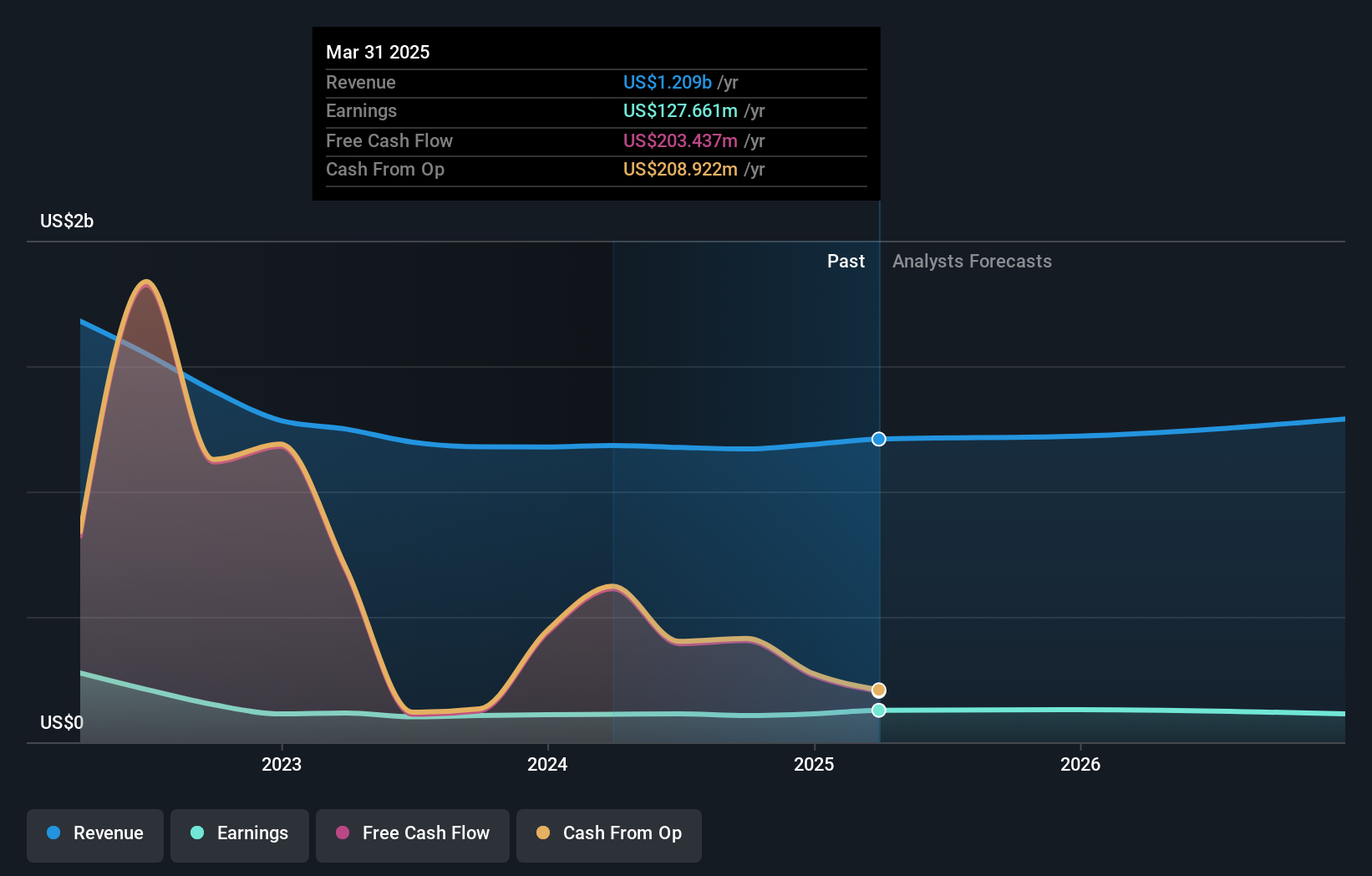

- In the past week, Hilltop Holdings reported weaker quarterly results that have drawn concern from analysts regarding its future profitability and efficiency.

- One unique insight is that persistent flat net interest income and an ongoing decline in earnings per share are leading some analysts to rate the company below industry standards.

- We'll examine how concerns around future profitability and efficiency are altering Hilltop Holdings' investment narrative and outlook.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Hilltop Holdings Investment Narrative Recap

To be a shareholder in Hilltop Holdings today, you need to believe that its core Texas and Sun Belt banking franchise, ongoing digital investments, and diversified revenue streams can offset persistent headwinds in mortgage originations and cost pressures. The recent weaker results and flat net interest income have put pressure on the most important near-term catalyst, continued loan growth and margin stability, while highlighting the biggest current risk: margin compression from intense competition and high operating expenses. For now, these impacts appear material, altering the risk-reward calculation for new and existing investors.

Among recent company developments, the July 24, 2025 share repurchase announcement, buying back 1,157,396 shares for US$34.88 million, stands out as most relevant to the latest earnings news. While buybacks can signal confidence or support share value, their positive impact may be offset if profitability and efficiency metrics remain under pressure, underscoring the need to watch for shifts in underlying business performance.

But, despite steady buybacks, investors should be aware that rising competition in key markets could further squeeze margins and limit...

Read the full narrative on Hilltop Holdings (it's free!)

Hilltop Holdings' narrative projects $1.3 billion revenue and $79.8 million earnings by 2028. This requires 1.7% yearly revenue growth and a $63.6 million decrease in earnings from $143.4 million.

Uncover how Hilltop Holdings' forecasts yield a $33.33 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community contributors placed Hilltop Holdings' fair value between US$32.23 and US$33.33 across two estimates. Yet recent analyst concerns over earnings pressure and margin compression remind you that market views and future outcomes can sharply diverge, consider multiple perspectives before making up your mind.

Explore 2 other fair value estimates on Hilltop Holdings - why the stock might be worth as much as $33.33!

Build Your Own Hilltop Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hilltop Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Hilltop Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hilltop Holdings' overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hilltop Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HTH

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor