Advertisement

- United States

- /

- Banks

- /

- NYSE:CFR

Cullen/Frost Bankers' (NYSE:CFR) Shareholders Will Receive A Bigger Dividend Than Last Year

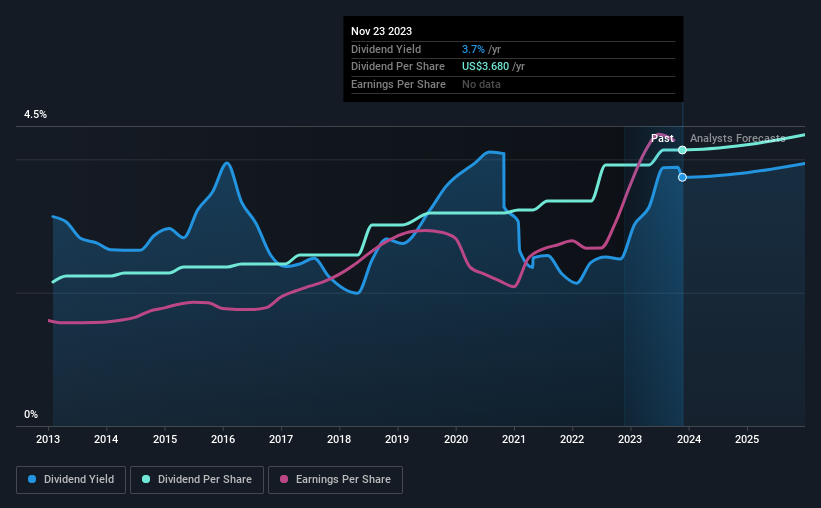

Cullen/Frost Bankers, Inc. (NYSE:CFR) has announced that it will be increasing its dividend from last year's comparable payment on the 15th of December to $0.92. This takes the annual payment to 3.7% of the current stock price, which is about average for the industry.

View our latest analysis for Cullen/Frost Bankers

Cullen/Frost Bankers' Dividend Forecasted To Be Well Covered By Earnings

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible.

Cullen/Frost Bankers has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Past distributions do not necessarily guarantee future ones, but Cullen/Frost Bankers' payout ratio of 34% is a good sign as this means that earnings decently cover dividends.

EPS is set to fall by 16.2% over the next 3 years. However, as estimated by analysts, the future payout ratio could be 44% over the same time period, which we think the company can easily maintain.

Cullen/Frost Bankers Has A Solid Track Record

The company has an extended history of paying stable dividends. The annual payment during the last 10 years was $1.92 in 2013, and the most recent fiscal year payment was $3.68. This works out to be a compound annual growth rate (CAGR) of approximately 6.7% a year over that time. Dividends have grown at a reasonable rate over this period, and without any major cuts in the payment over time, we think this is an attractive combination as it provides a nice boost to shareholder returns.

The Dividend Has Growth Potential

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that Cullen/Frost Bankers has been growing its earnings per share at 9.5% a year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

We Really Like Cullen/Frost Bankers' Dividend

Overall, a dividend increase is always good, and we think that Cullen/Frost Bankers is a strong income stock thanks to its track record and growing earnings. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. However, it is worth noting that the earnings are expected to fall over the next year, which may not change the long term outlook, but could affect the dividend payment in the next 12 months. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 1 warning sign for Cullen/Frost Bankers that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CFR

Cullen/Frost Bankers

Operates as the bank holding company for Frost Bank that provides commercial and consumer banking services in Texas.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.0% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.1% undervalued

ME

Community Contributor