- United States

- /

- Banks

- /

- NYSE:BY

A Look at Byline Bancorp’s Valuation After New Fixed-to-Floating Rate Exchange Offer Announcement

Reviewed by Simply Wall St

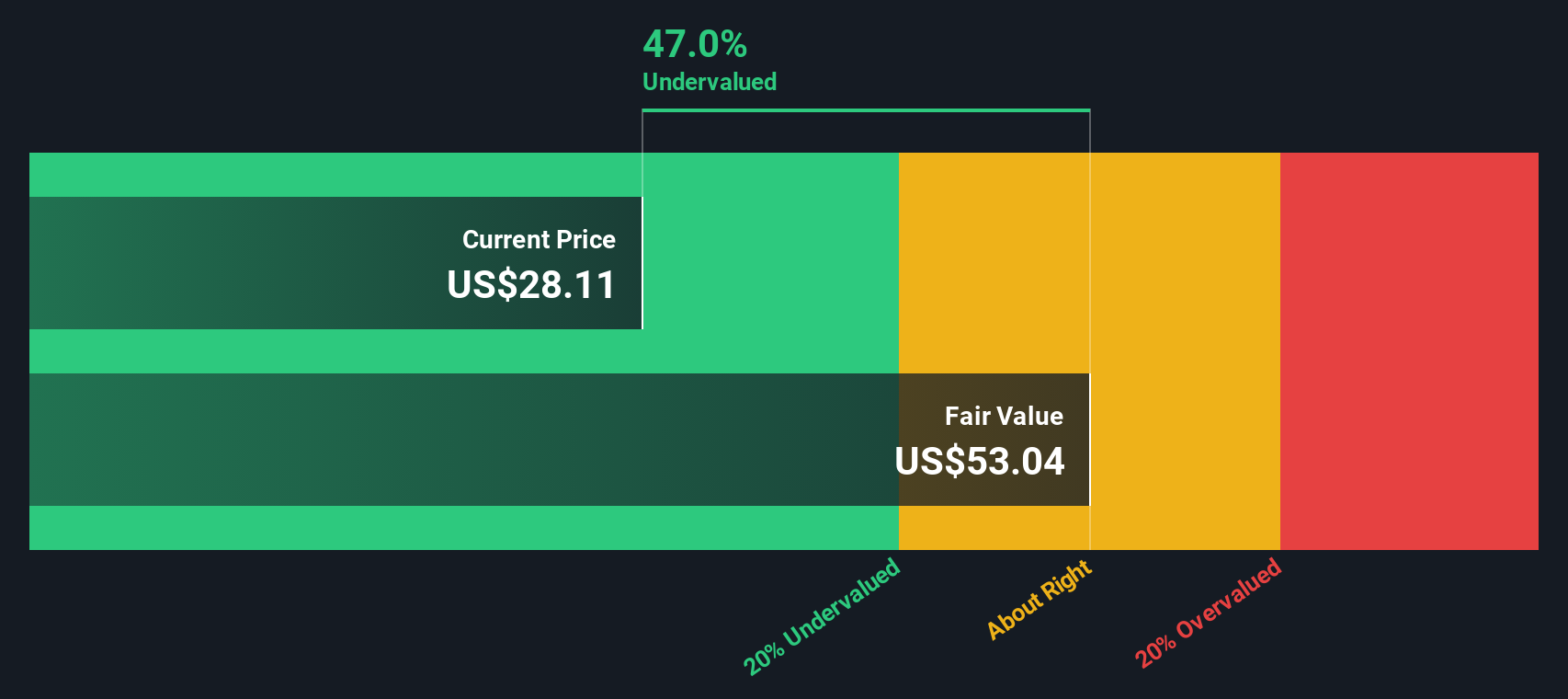

Most Popular Narrative: 8.6% Undervalued

According to the most widely followed narrative, Byline Bancorp is currently valued at approximately 8.6% below its estimated fair value. Analysts see room for upside based on future growth and operational execution.

"The successful integration of First Security, including immediate cost synergies and system upgrades, has expanded Byline Bancorp's lending and deposit base while improving operational efficiency. This development sets the stage for higher net interest income and improved net margins going forward."

Want to know what’s powering this undervaluation call? The narrative is fuelled by aggressive forward projections, major operational efficiencies, and some bold targets for future profit margins. Think you know which big assumptions are driving this valuation? Dive in to see which figures could be the difference makers. These numbers might surprise you.

Result: Fair Value of $32.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, several factors could challenge this bullish outlook, such as the risk of integration issues and potential slowdowns in digital transformation compared to its peers.

Find out about the key risks to this Byline Bancorp narrative.Another View: A Deep Discount?

A closer look from our DCF model points to a very different story. It suggests the shares could be trading at a significant discount. Does this method capture hidden value, or is it too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Byline Bancorp for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Byline Bancorp Narrative

If you see things differently or want to dig deeper into the numbers yourself, you can craft your own take in just minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Byline Bancorp.

Looking for more investment ideas?

Now is the perfect time to seize emerging opportunities and outpace the market. The right tools and fresh strategies will set your portfolio apart. Don’t let the next big winner slip by.

- Unlock higher yields when you check out dividend stars offering returns over 3% with our dividend stocks with yields > 3%.

- Spot tomorrow's tech leaders by starting your research into artificial intelligence breakthroughs using AI penny stocks.

- Capitalize on bargains by tracking down undervalued companies based on future cash flows with our undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Byline Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NYSE:BY

Byline Bancorp

Operates as the bank holding company for Byline Bank that provides various banking products and services for small and medium sized businesses, commercial real estate and financial sponsors, and consumers in the United States.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion