- United States

- /

- Energy Services

- /

- NYSE:INVX

Three Undervalued Small Caps With Insider Buying In US

Reviewed by Simply Wall St

The United States market has remained flat over the last week but has seen a 21% increase over the past year, with earnings forecasted to grow by 14% annually. In this environment, identifying stocks that are potentially undervalued can be appealing to investors seeking opportunities for growth, and insider buying may serve as an indicator of confidence in a company's future prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| OptimizeRx | NA | 1.2x | 37.80% | ★★★★★☆ |

| First United | 12.9x | 3.4x | 31.72% | ★★★★☆☆ |

| Eagle Financial Services | 7.5x | 1.6x | 36.05% | ★★★★☆☆ |

| Innovex International | 9.0x | 2.1x | 46.32% | ★★★★☆☆ |

| West Bancorporation | 15.3x | 4.7x | 41.01% | ★★★☆☆☆ |

| Limbach Holdings | 39.2x | 2.0x | 42.82% | ★★★☆☆☆ |

| ChromaDex | 282.5x | 4.6x | 31.15% | ★★★☆☆☆ |

| Franklin Financial Services | 14.9x | 2.4x | 21.87% | ★★★☆☆☆ |

| Guardian Pharmacy Services | NA | 1.1x | 33.86% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -76.34% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

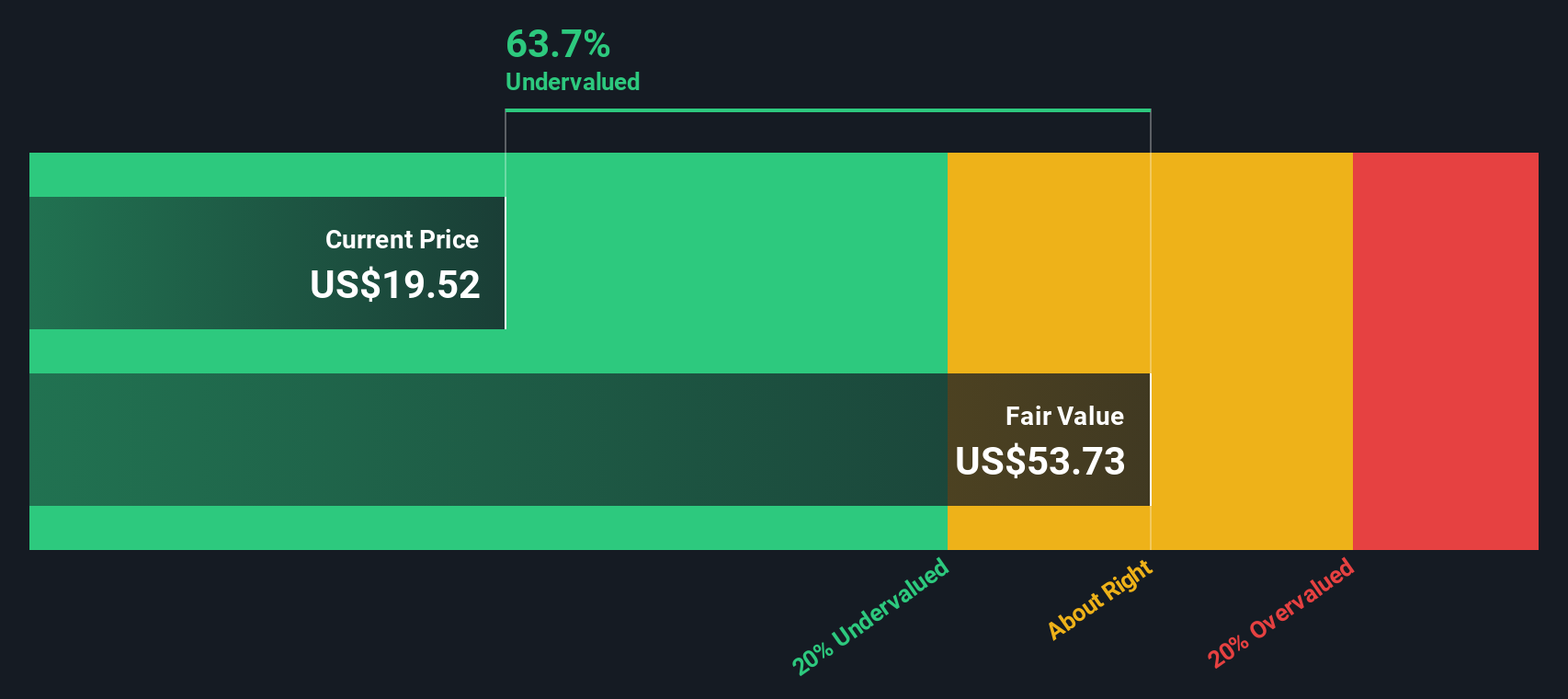

West Bancorporation (NasdaqGS:WTBA)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: West Bancorporation operates as a community banking organization, focusing on providing financial services primarily through its community banking segment, with a market capitalization of approximately $0.37 billion.

Operations: West Bancorporation generates revenue primarily through community banking, with significant operating expenses including general and administrative costs. The company's net income margin has shown variability, peaking at 47.18% in early 2022 before declining to 30.52% by the end of 2024.

PE: 15.3x

West Bancorporation, a smaller U.S. financial entity, recently showcased insider confidence with share purchases in the last quarter of 2024. Their fourth-quarter results revealed net income rising to US$7.1 million from US$4.53 million year-over-year, alongside an increase in net interest income to US$19.42 million from US$16.36 million a year prior. With earnings projected to grow at 16% annually, this company exhibits potential for future growth amidst its current market valuation challenges.

- Unlock comprehensive insights into our analysis of West Bancorporation stock in this valuation report.

Explore historical data to track West Bancorporation's performance over time in our Past section.

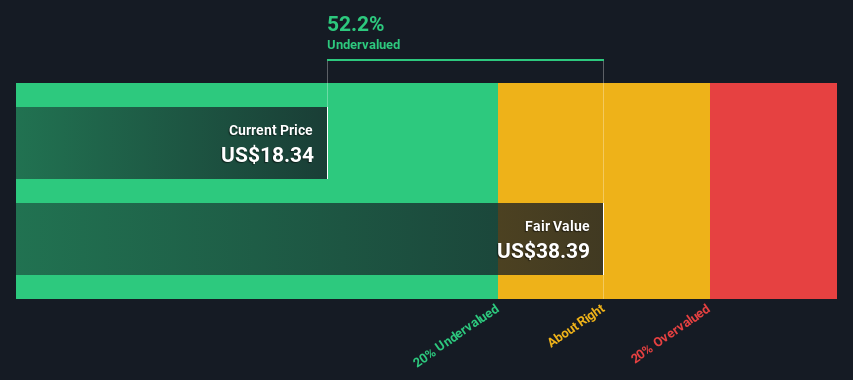

Innovex International (NYSE:INVX)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Innovex International operates in the oil well equipment and services industry, providing specialized products and solutions to enhance oilfield operations, with a market capitalization of $2.35 billion.

Operations: Innovex International generates revenue primarily from its Oil Well Equipment & Services segment, with recent figures at $543.31 million. The company has seen a notable trend in its net income margin, which reached 23.37% as of the latest reporting period.

PE: 9.0x

Innovex International, a smaller U.S. company, shows potential despite recent challenges. Revenue dipped by 1.3% over the past year, partly due to significant one-off items affecting earnings quality. The firm relies solely on external borrowing for funding, which poses higher risks compared to customer deposits. However, insider confidence is evident with notable share purchases in the last six months of 2024, suggesting belief in future growth prospects and possibly indicating an undervalued position in the market.

- Get an in-depth perspective on Innovex International's performance by reading our valuation report here.

Gain insights into Innovex International's past trends and performance with our Past report.

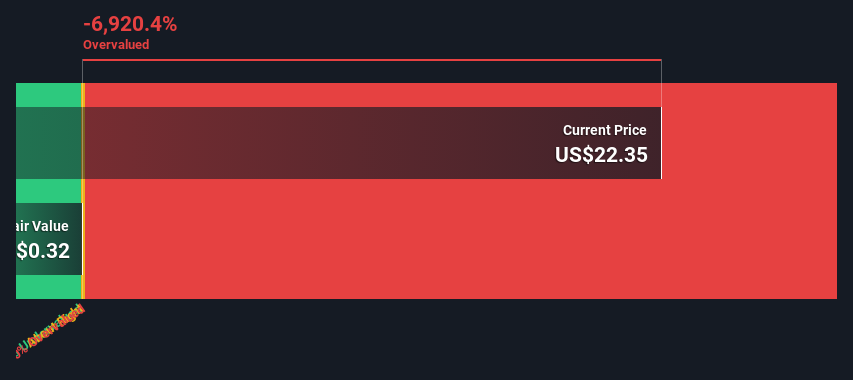

MultiPlan (NYSE:MPLN)

Simply Wall St Value Rating: ★★★★★☆

Overview: MultiPlan is a company that provides healthcare cost management solutions, with a focus on offering business services to its clients, and has a market cap of approximately $1.25 billion.

Operations: MultiPlan's revenue primarily comes from Business Services, with recent figures showing $942.61 million. The company experienced a gross profit margin of 74.23% as of the latest period ending in February 2025. Operating expenses and non-operating expenses are significant, contributing to a net income margin of -163.30%.

PE: -0.3x

MultiPlan, a company with significant experience in healthcare cost management, is making strides despite its small size. The recent strategic agreement with J2 Health aims to optimize network performance for healthcare payors, enhancing efficiency and reducing costs. Meanwhile, insider confidence is evident as their Chief Information Officer purchased 40,000 shares worth US$249,588 recently. However, the company's reliance on external borrowing poses risks. Their innovative CompleteVue platform seeks to improve pricing strategies and market insights for providers amidst a volatile share price environment.

- Click here to discover the nuances of MultiPlan with our detailed analytical valuation report.

Evaluate MultiPlan's historical performance by accessing our past performance report.

Key Takeaways

- Gain an insight into the universe of 54 Undervalued US Small Caps With Insider Buying by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Innovex International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:INVX

Innovex International

Designs, manufactures, sells, and rents mission critical engineered products to the oil and natural gas industry worldwide.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives